BDC Common Stock Market Recap: Week Ended March 20,2020

Premium FreeBDC COMMON STOCKS

Incredible

In every conceivable way, the week ended March 20, 2020 was shocking, and will be long seared in the consciousness of BDC investors.

The sector- as measured by the UBS Exchange Traded Note with the ticker BDCS – dropped (28.4%) in the five days.

That followed an almost as remarkable (19.5%) the week before.

Down.Up.Down

The chart below shows the progress of the decline from February 20, 2020 – which we use as the starting point till last Friday.

Note the attempted bounceback on Thursday March 19 – which petered out – and the drop back on the last day of the week.

The chart also does a good job of showing the changes in the volume of BDCS which tells us a little about investor positioning.

You could argue – but we won’t – that the high volume on Friday – suggests that investors have reached their nadir.

What A Difference

BDCS closed at a price of $10.52, down (49.8%) from the close on February 20.

Still, that was not the sector’s lowest point, which came intra-day the day before – and only for the briefest of moments – at $8.61.

At that point, BDCS was down (57.9%) in just a month.

Equally Astounding

Necessarily, all the other metrics we use to take the temperature of the BDC sector were off the charts.

All BDCs decreased in price and all dropped by (3.0%) or more.

On the week, the Biggest Loser happened to be Portman Ridge Financial (PTMN), down (49.3%).

We can’t help feeling badly for BC Partners – the asset management group that bought out KCAP Financial and OHA Investment at just the wrong time and through no fault of their own.

The BDC’s exposure to KCAP’s CLO equity investments may have encouraged the fire sale this week.

Crowded Field

Still, PTMN had plenty of company with 41 BDCs of 45 dropping (20%) or more on the week.

Thanks to these massive losses even over a 1 year data every BDC is in the red – and deeply so.

Sidebar

Curiously, the least poorly performing BDC (if such a category exists) is Prospect Capital (PSEC): off (27.4%) compared to same time last year.

It’s one of those ironic little twists that the BDC with the highest compensation package and that does not bother with stock buybacks is performing the least badly !

Makes one wonder what is more important in keeping up BDC prices: fundamentals; “shareholder friendly” actions or good marketing ?

We really don’t have an answer but we noted the following during the week on Seeking Alpha, which might have affected both PSEC’s price and investor confidence:

We’re not fans of Prospect Capital as an investment. Heck, we’re short the BDC right now as part of our hedging strategy. But – to be fair – CEO John Barry has bought a monumental number of shares during this crisis: 17,721,293 by our calculation. He now owns 57,696,218.

As Expected

More obviously, the worst performer over a twelve month period is Medley Capital (MCC), down (86%), half of which occurred this week.

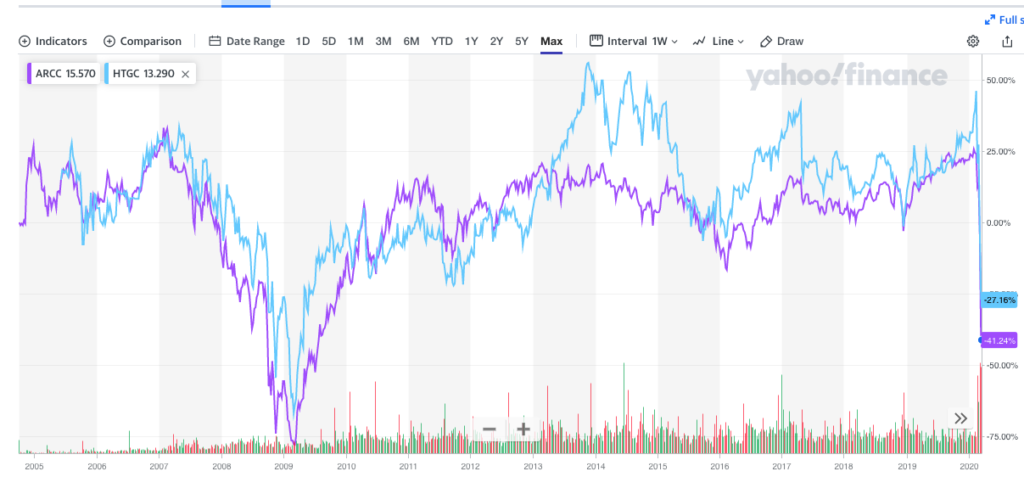

Back In Time

The BDCS measuring stick we use was only introduced in early 2011, and does not offer a useful perspective of where we stand.

For that, we’ve grabbed the long term charts of two BDC stalwarts – albeit in different segments of the leveraged loan market: Ares Capital (ARCC) and Hercules Capital (HTGC).

Their current price levels are in line with where we were in the fall of 2018 as investors began to worry about – everything.

Even then, we were still months away from the bottom of the market which occurred – depending on whom you ask – in a narrow window between late February – early March 2009.

By that standard, both BDCs – and we’re talking roughly here – still have (50%-70%) drops in their price to go before reaching their All-Time Lows.

Zoom

What’s different this time – amongst so many items – is the speed of the decline compared to the Great Recession.

Hope dies fast under the current conditions.

Back at the beginning of the Great Recession, HTGC dropped just (2.2%) in the first month of the downturn, but would ultimately fall a total of over (75%) from highest to lowest closing prices.

You Must Remember This

The charts of the Great Recession are mostly instructive in one key way – as a reminder that investors – if sufficiently spooked – can almost completely desert the BDC sector at these critical times.

This time round – one could argue – many hard nosed investors have remained optimistic – if that’s not too startling a word.

This probably comes down to FOMO: Fear Of Missing Out – and peering over at what happened to HTGC and ARCC’s stock price after all hope was lost last time round.

Rocket Ship

The former eventually peaked in 2013 (mostly on hopes of the BDC’s cashing in on Facebook !) 4.7x higher in price.

Investors in ARCC only had to wait till the spring of 2011 – just two years after the nadir – to make a 5.3x return.

FOMO, though, can be a siren’s song as BDC investors found out 5 times in the past month as prices started to move up, only to drop back again.

Depending on how you slice the numbers ARCC’s investors during its Great Recession slide got unduly optimistic NINE times before “calling the turn” correctly.

(We know. We were there and living the adage “Fool Me Once Shame On You. Fool Me Twice Shame on Me”).

Less Known Acronym

That other lesson of the Great Recession – which doesn’t get taught as much – is that a little patience can be an investor’s strategy too.

In the Great Recession, the rebounds typically lasted only a few days or weeks.

The longest period of false optimism was towards the end and lasted 6 weeks.

If you’d waited 6 weeks to invest in ARCC after its Great Recession low, you’d still have tripled your money two years later at that height, and made even more if you’d waited till the recent high.

Every investor has their own methodology and the BDC Reporter would never advise anyone on how to “play” the market, but we offer up this PIG approach (“Patience Is Good”) as one possible option for the tool-kit.

Week Ahead

Unfortunately, we don’t see any end in sight to the fog of uncertainty that has covered the economy, the markets and the BDC sector.

We wrote an article in a hurry on March 18, 2020 entitled “Where We Stand And Where We’re Headed”.

The key point then – and which we stand by in the quiet of the weekend – is that BDC investors have to throw out all their prior expectations about BDC performance and outlook.

The writing is on the wall that we are going to face conditions akin to those between 2008-2011 than those of recent years.

As the song goes ” some will win, and some will lose” but all BDCs at first will sing the blues.

No Exceptions

That’s because the universal impact of Covid-19 on the U.S. and global economy means almost every company in almost every industry is affected, and to degrees never before faced.

All BDCs will face a grim reduction in the value of their portfolio assets – and an immediate deduction to their capital – when March 31, 2020 results are published.

Nobody will be immune from an unprecedented drop in NAV.

That will be – in you’ll excuse the analogy – akin to the immediate aftermath of an unexpected tornado.

Everyone is affected and everyone is in shock.

However, the real impact will vary widely – as happens after a tornado – on a BDC-by-BDC basis.

Nobody will be spared but some will recover faster than others and might be able to resume normal operations.

Very Preliminary And Very Broad

Our look down the leverage levels of the 45 BDCs we track – and taking into account what we knew previously about credit quality; liquidity; earnings coverage of the dividend etc – does not provide much solace in the short term.

Because of the huge and across the board in asset values expect a quarter to half of BDCs to breach the minimum asset coverage of debt required of BDCs of 150%.

(That’s the 2:1 debt to equity that we – and others bandy around all the time but differently expressed).

Cutting

We also expect many BDCs to follow the example of Great Elm Corporation (GECC) and begin to pay distributions in cash and additional stock on a 20/80 ratio.

Just when many investors might have been most counting on their distributions these will be cut – both in form and substance in the quarters ahead.

GECC – and all others that follow in their wake – are doing the “right thing” to protect liquidity at a time when cash is king and debt makes paupers.

Discount

At the moment, and we see this on the literally hundreds of loans to BDC portfolio companies we’ve priced out, virtually every asset has dropped by (15%) to (30%) in value.

That includes every industry and every company you can think of, and all this has happened in days.

Yo-Yo ?

The good news: valuations could readily bounce back if the environment improves.

They represent more of a natural de-risking by nervous debt holders dealing with the same sort of worries as those in every other market.

However, once we get the Covid-19 all clear (which may be a longer time coming than markets were expecting as of Friday and could occur in stages), BDCs will be far from safe.

Then, the BDCs and their borrowers will be able to work-out (pun intended) who will be able to return to “normal” and who will need new capital; restructuring; amendments etc.

Knowing how that will play out BDC-by-BDC at this stage is impossible because we are still at a very early stage and governmental support – if any – is unclear.

Other Challenges

Nor will BDCs only have to contend – once we get back to work – with a multitude of credit issues but also with a much lower LIBOR, which will diminish earnings significantly.

Then there will be very little in the way of new loans booked for some time; as higher spreads; borrower/lender uncertainty freeze up investment activity.

That’s going to hurt BDC income derived from pre-payments and new loan activity, but that may be partly offset by borrowers paying for loan waivers and restructurings as occurred in 2008.

Borrowing costs will drop for BDCs, but not in all cases as many players – not unreasonably – rushed to borrow unsecured in recent months, fixing in rates.

Phew

Whatever their other troubles BDCs financed exclusively or heavily by cov-lite unsecured debt that’s not coming due in 2020 are delighted by their liability management choices right now.

BDCs that rely heavily on Revolvers, and the kindness of bankers , are wondering how the providers of their liquidity are going to behave in this new environment.

Investors might want to dig through 10-Ks to be reminded which BDCs arranged secured financing that is not marked to market but to real credit losses.

Those BDCs – assuming they remain in compliance with BDC industry asset coverage rules – may fare better in their relationship with their bankers than others.

Shrinkage

Overall, we expect – even after adjusting for valuation changes – to see BDC assets drop substantially in the quarters ahead, just after nearly two years of unrelenting growth thanks to the SBCAA.

Some BDCs will be allowing portfolios to shrink to meet asset coverage rules; there will be write-offs to contend with and hard decisions to be made about whether to pay down debt.

If BDCs do end up stabilizing their balance sheets, some may choose to use loan run-off to shrink and use the proceeds to avoid any upcoming debt deadlines, either on Revolvers or Baby Bonds.

Unlikely

Several BDCs – prior to the crisis and – in the case of TPG Specialty (TSLX) – after, boasted of their intention to take advantage of market dislocations to grow AUM at above average spreads.

However, the BDC Reporter’s believes that will be hard in this extreme environment and just keeping one’s head above water might be the best result one can expect.

Next Year

Any advantage to be taken will likely to have to wait till 2021, assuming Covid-19 can be relegated to bad flu status by then.

Newest List

The BDC Reporter – for our own benefit and that of our readers – is beginning to analyze each BDC’s likely outlook in turn, as we did where Apollo Investment (AINV) was concerned.

Candidly, though, this is like undertaking damage assessment in the middle of a natural disaster, rather than in its aftermath., to go back to our earlier analogy.

For a while longer we’ll content ourselves with drafting up a new Table which will provide our projections as to what will happen to individual BDCs NAV; leverage; dividend paying power and credit outlook.

We won’t be publishing that Table quite yet until the situation clarifies, to avoid providing either false hope or dismay to readers unwise enough to take our on-the-fly assessments as gospel.

When we do publish this BDC Pro-Forma Table, expect to see constant revisions to our views as the environment gets into focus and we hear from the BDCs themselves.

Mostly Crickets

To date, there have been very few reassuring words from the BDC community.

As we mentioned TSLX published a press release as did Main Street Capital (MAIN).

Great Elm (GECC) – as a late filer – made some references to the difficult conditions.

Generally speaking, though, most BDCs are busy calling both their borrowers and their own lenders and watching the situation unfold – in many cases from home in their pajamas like the rest of America.

We’ll be forwarding and analyzing any public statements from the BDCs as they come out.

And they will.

Not On Our Side

In conclusion, the most important asset right now for BDCs is time.

Time to determine what support they and American business might receive from Washington and from Wall Street.

We proposed a couple ideas in this regard in our article ostensibly about AINV.

We even ingenuously forwarded our thoughts to Senator Warren, who has been quizzing Treasury Secretary Mnuchin about his own plans for the coming leveraged loan crisis.

You’ll be surprised to hear we’ve not received a phone call from either.

One More

Chances are, though, is that the private sector – both the BDCs and their borrowers – are mostly going to dig themselves out of this by themselves.

How about a 3 month “forbearance” by both the lenders to the BDCs and the BDCs themselves to their borrowers ?

That does not preclude anyone from eventually exercising their legal rights; and income continues to accrue but a critical breathing space is created to give time for the medical community to do its work.

The day of reckoning for Greece has been kicked down the road for years.

Surely, American business deserves 3 months ?

Wake up Wall Street !

Already a Member? Log InRegister for the BDC Reporter

The BDC Reporter has been writing about the changing Business Development Company landscape for a decade. We’ve become the leading publication on the BDC industry, with several thousand readers every month. We offer a broad range of free articles like this one, brought to you by an industry veteran and professional investor with 30 years of leveraged finance experience. All you have to do is register, so we can learn a little more about you and your interests. Registration will take only a few seconds.