BDC Common Stocks Market Recap: Week Ended June 24, 2022

BDC COMMON STOCKS

Week 25

Deep Breath

After three weeks of unrelenting price drops, the BDC sector bounced some of the way back.

BDCZ – the UBS sponsored exchange traded note that owns most BDC stocks and which we use as a sector price guide – increased by 3.11% in just 4 trading days.

The S&P BDC index – calculated on a total return basis – did even better, jumping 3.31%.

Where BDCZ is concerned, this week’s jump forward offset 29% of the prior three weeks losses.

Not Unanimous

Most all the 43 individual BDCs that make up our coverage universe joined in this relief rally: 32.

Still, 11 BDCs continued to drop in price…

Ups And Downs

As you’d expect price volatility – as measured by the number of BDC stocks moving 3% or more in either direction over the 4 day week – was high.

There were 18 BDCs that moved up 3.0% or more, and 3 that moved down by (3.0%) plus.

In what was otherwise a good week for BDC stocks, 3 players still reached new 52 week lows.

These were Cion Investment (CION); Runway Growth Finance (RWAY) and Monroe Capital (MRCC).

What Is Happening Here ?

Earlier in the year, the BDC sector out-performed the major indices all the way through April 20.

In recent weeks, though, the BDC sector has increasingly reverted to mimicking what happens to the S&P 500.

This chart below tells the story:

The current difference between the two indices is now the narrowest since early in the year.

Not Yet A Bear

Overall, BDCZ is down in price (14.0%) YTD, while the total return S&P BDC Index is in “correction” territory as well: off (11.2%).

As you’d expect after the last 9 weeks of carnage, it’s been very hard for any individual BDC to hold its price.

Not A Pretty Sight

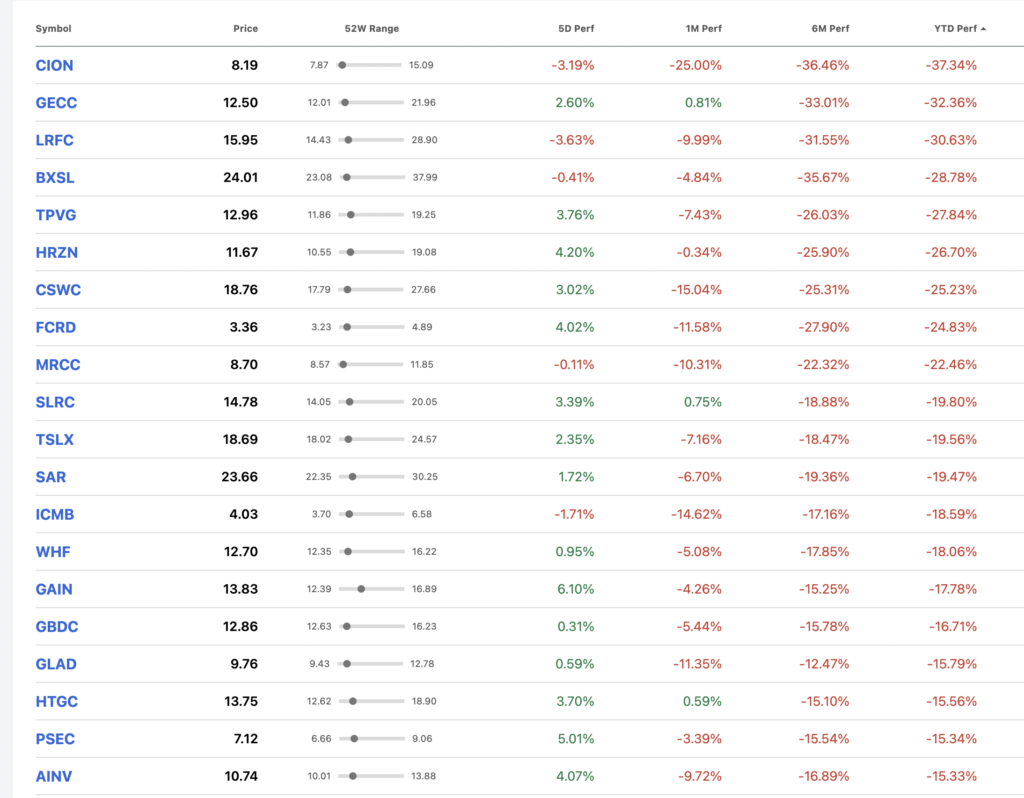

Year-to-date, 42 of the 43 BDCs are in the red, with only Fidus Investment (FDUS) able to boast of a very slight price gain – 0.9%.

Some of the price drops in 2022- this week’s bounce back notwithstanding – continue to be monumental.

As this chart from Seeking Alpha shows, 20 stocks have fallen by 15% or more in these first 25 weeks:

Popular Categories

Or, putting the price loss data in another context: 9 individual BDC stocks are in “bear market” territory having dropped (20%) or more, and 25 are between (10%) and (20%) down – “correction” territory.

There are some BDCs that have underperformed where fundamentals are concerned (GECC), or are not paying a dividend (LRFC), but most of these BDCs up to their waists in red ink are well regarded players, many of whom have been increasing their dividends.

Which is to suggest that BDC price drops to date has been as much as about profit taking as anything else as everybody maneuvers ahead of the seemingly inevitable recession.

Toxic Stew

Of course, the problem is that the future is particularly opaque at the moment which makes pricing stocks of all kinds – including BDCs – particularly problematic.

There’s the “soft”, “soft-ish” and “hard landing” debate, then there’s the question on when this all occurs and what will be the intensity of any economic drawdown. Even more problematic – but not discussed as much – is which industries will fare better and worse when the rains come. Are technology and healthcare – very large components of the economy and of leveraged lending – going to be hit hard ? In the recent past, investors and lenders have considered them almost immune to downturns.

Then there’s the wide range of possibilities about where short and long term interest rates (“you can’t have one without the other”) might go in the years ahead. We can’t imagine – however we might like to – that the level of rates will return to the levels of year end 2021 any time soon. Whatever the picture ends up being at the end of 2022 and 2023 will make a huge difference to BDC investment income, but also to how funding is constructed going forward.

If long term rates continue to rise – making the cost of new unsecured notes and convertibles prohibitive – we might see a change in how BDCs fund themselves and a greater reliance on secured facilities tied to floating rate SOFR. On the other hand, if short term rates do get pumped up as high as 5% – as some economists are predicting – while long term rates stabilize close to current levels, the opposite might happen. Those are just two of thousands of possible permutations.

You Can Handle The Truth

The fact is that “nobody knows anything” about Hollywood as well as the future state of the economy, interest rates and what’s going to happen to the BDC sector, and anybody who claims otherwise is misguided.

We are in a period of maximum uncertainty, which means that volatility is likely to persist.

Just in the last 9 weeks, BDCZ has moved up or down by greater than 3.0% 6 times…

Ho Hum

In great contrast to the volatility we see where the price of BDC stocks (and bonds for that matter) are concerned is the prosaicness of the recent news stream.

In June so far, 4 BDCs have announced monthly or quarterly distributions: 3 were unchanged and 1 was increased. None were a great surprise.

One BDC repaid two publicly traded Baby Bonds (Logan Ridge Finance or LRFC) while another – Horizon Technology Finance (HRZN) tapped the public debt market again. Likewise Prospect Capital (PSEC) continued a long tradition of issuing very small amounts of unsecured debt to retail investors at very low rates. The most recent 5 year inter-notes were priced at 4.5%.

Even the institutional market for unsecured debt seems to have re-opened after a few months on hiatus, with New Mountain Finance’s $75mn unsecured note issuance, covered on these pages last week.

Hercules Capital (HTGC) – as well – has been fine tuning its liability management, both increasing the size of its secured revolvers and raising $50mn in unsecured notes. Interestingly – and probably with a recession in mind – the maturity of the new debt is only 3 years long and bears interest at 6.00%. (HTGC also raised $150mn in secured notes which are expected to run off over 3.1 years, even though their nominal maturity is 2031).

During this difficult period, Great Elm Capital (GECC) has impressively managed to successfully complete a Rights Offering and non-traded Franklin BSP Lending (not included in our coverage) even raised $325mn in new equity.

Whatever storm is headed this way, it’s not yet reached the BDC sector which – at least on the surface – appears to be in a business as usual mode, although new transaction volumes – according to news services – appear to have dropped compared to 2021’s pace while new loan spreads – according to Direct Lending Deals – have increased by about 50 basis points.

Dazed And Confused

All of this uncertainty in the future mixed in with complacency of the moment has wreaked havoc with analysts BDC earnings models.

We’ve been looking over the revisions made to projections for the second and third quarter of 2022 and for the next two years over the past 90 days and found the numbers are bouncing all over the place – both up and down.

The analysts – like everyone else – are not sure what to expect.

Our Suggestion

The best course – and the one we are taking – is to take matters one day at a time and not presume too much.

This period where everything is a question mark will pass, but patience will be needed.

At the moment, though determining whether you were right or wrong to be long BDCs or not, or any particular name, is impossible to say.

Sadly for those who want immediate answers, we might have to wait till 2024 for clarity.

Already a Member? Log InRegister for the BDC Reporter

The BDC Reporter has been writing about the changing Business Development Company landscape for a decade. We’ve become the leading publication on the BDC industry, with several thousand readers every month. We offer a broad range of free articles like this one, brought to you by an industry veteran and professional investor with 30 years of leveraged finance experience. All you have to do is register, so we can learn a little more about you and your interests. Registration will take only a few seconds.