BDC Common Stocks Market Recap: Week Ended February 14, 2025

BDC COMMON STOCKS

Week 7

For the week, the S&P 500 (SP500) gained +1.5%, while the tech-heavy Nasdaq Composite (COMP:IND) surged +2.6%. The blue-chip Dow (DJI) added +0.5%.

february 15, 2025 – Seeking alpha – wall street breakfast

Happy Days

The major indices were up across the board this week, as you can see above, with the NASDAQ “surging” to use the preferred nomenclature of the market.

Increasing inflation, global tariffs and higher interest rates? Bring ’em on, the markets seem to be saying.

Anyway, the BDC sector was not left out of this period of good feelings.

In fact, BDCs are running ahead of the major markets in many cases, as the rally that began the day after the Presidential election rolls onward and upward.

Here are some the metrics that make our point, without need for further comment:

Metrics

BIZD, the only BDC exchange traded fund and our main way to measure sector price changes, was up 2.0%, and reached a new 52 week high.

The S&P BDC Index increased 2.1% on a price basis and a total return basis.

43 BDCs out of the 46 in our coverage universe were up in price.

Of the BDCs in the black, 11 increased in price by 3.0% or more.

Only 1 fell more than (3%).

Exception

This Biggest Loser was Carlyle Secured Lending (CGBD), off (3.9%).

The BDC’s stock price was down (3.9%) on the week, way more than anyone else.

That was enough to also tip the BDC into the red for 2025 YTD.

The likely reason: an Underperform rating on Monday from BofA, switched from Buy previously.

“Earnings growth and overall profitability will likely disappoint investors following the completion of its merger with an affiliated private BDC (CSL3).”

Also – the analyst adds – the stock has become over-valued.

We did double-check IVQ 2024 earnings expectations for CGBD, which are for $0.44 of Net Investment Income Per Share (NIIPS), down (7%) from the IIIQ 2024 result.

Over at BDC Best Ideas we track the analysts earnings consensus for every BDC and note that the current outlook is for NIIPS to drop (12.2%) in 2025.

That’s above the (9.7%) average for all the BDCs we track over there, so maybe the BoFA analyst is on to something.

On the other hand – as someone who’s forever checking actual recurring earnings against “expectations” and also watching the analysts constantly moving their own goalposts – we wouldn’t say NIIPS projections are written in stone.

There are dozens of variables that go into the ultimate NIIPS number every quarter so even getting the actual number right probably has more to do with luck than a finely tuned financial model

Back To The Party

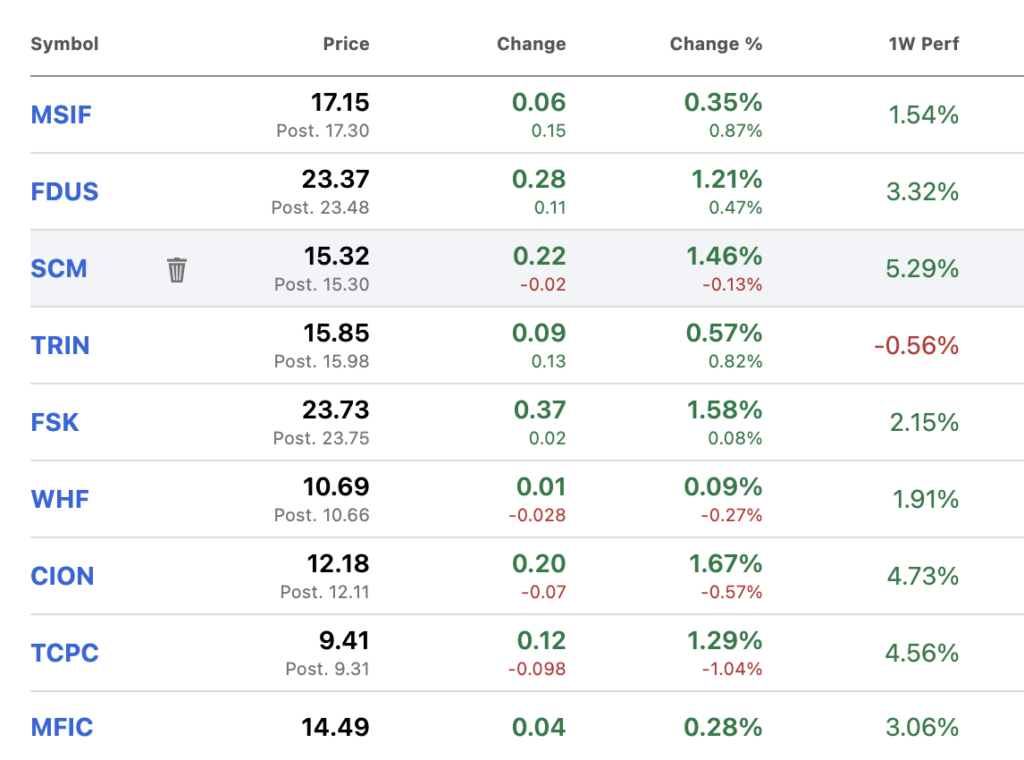

Here is a list of the BDCs up 3.0% or more.

This is a heterogenous group, led by the latest public BDC – MSC Investment (MSIF), regarded by many as Main Street Capital’s (MAIN) younger sibling because an affiliate of the popular BDC serves as the external manager and its portfolios are very similar.

On the list above are BDCs that have fared very well where fundamentals are concerned (remember those? ) and others that have not. There are BDCs that serve the venture debt market; and all the segments of the traditional LBO borrower.

We did note, though, that all the BDCs above have NOT yet reported IVQ 2024 earnings.

Thiis suggests investors are piling in the expectation of seeing decent results when these BDCs open their earnings kimonos shortly.

That seems to include BDCs that have been disappointing their shareholders of late where credit is concerned such as BlackRock TCP (TCPC); CION Investment (CION) and WhiteHorse Finance (WHF).

We don’t want to use our hoary old cliche but we have to: the rising tide is lifting all boats.

What A Bull Market Looks Like

Only 1 BDC is trading within 5% of its 52 week low price and 9 are 5%-10% out.

By contrast, 22 BDCs are within 5% of their 52 week heights and another 7 close by 5%-10% off that prak.

An unusually high 10 BDCs reached new 52 week records this week and none dropped to a new 52 week low.

A favorite metric of investors: the number of BDCs trading at or above book increased to 20, from 18 the week before.

Fathoming

We all know that the markets never explain themselves, both on the way up and the way down.

However, we surmise with an unusual degree of confidence, that the BDC sector’s strength has little to do with a belief in tariffs, or hoping that the war in Ukraine is going to go away, or any of those things.

As usual, the key factor is likely the apparent strong possibility that the Fed Funds rate – and thus SOFR on which all floating rate loans are built – will remain higher for longer. Possibly much longer.

We heard this week from Chairman Powell who sounded very comfortable keeping rates where they are and the futures suggest we will be getting only one interest rate cut in 2025.

The number – not so long ago – was four.

There’s always a few economists bucking the consensus and this week we had Torsten Slok at Apollo Global Management predicting – which may be too strong a word – an INCREASE in the Fed Funds rate in mid-year.

We say “never say never” even if most of the other dismal scientists don’t agree.

We mention this outlier – which could become consensus in a few months – as the uncertainty may keep BDC prices fizzing while investors try to ascertain the path of future rates.

Who wants to leave the party when the Fed might still be handing out more cake?

Where We Are In 2025

So much for the latest moves in the BDC market.

Pulling back a little bit to gain a 7 week view of the year so far, we find BIZD up 5.8%, well above the S&P 500’s price change of 4.0%.

On a total return basis, using the S&P BDC Index as our measuring stock, we are up 5.6%, which outstrips the S&P 500′s own “total return” of 4.1%.

For this period, 42 of the 46 BDCs are up in price, reflecting that whole tide analogy.

Little Guys Rule

Interestingly – if only to us – the Biggest Winners outside of MSIF which leads the pack – are smaller BDCs like Oxford Square Capital (OXSQ); Stellus Capital (SCM) and White Horse Finance (WHF).

Yes, the Big Boys of the BDC sector likes Ares Capital (ARCC); Blackstone Secured Lending (BXSL) and Blue Owl Capital (OBDC) have held up alright and are squarely in the black but lag many percentage points behind the minnows.

Maybe investors are not yet fully convinced there has been a sea change in BDC economics with the changing rate environment, or quick witted traders have already marked up prices to what they consider a reasonable price.

Reset

For example, ARCC’s stock price – going by the Friday close and comparing with Election Day – has increased 11% already and was 14% up at one point.

As we’ve discussed in the BDC News Feed, there was nothing very special about the BDC’s IVQ 2024 results that would justify its recent ascent.

Net Asset Value Per Share (NAVPS) increased, but only because management sold a boatload of new shares at a premium to book; earnings were a little softer than expectations and the dividend remained unchanged, just as expected.

Where We’re Headed

Of course, of most importance is where we go from here after a blistering start to 2025.

As an old hand in these markets, we tend to be skeptical of these periods of unrelenting rallying where every day our favorite BDCs – as well as all the others – keep marching up in price.

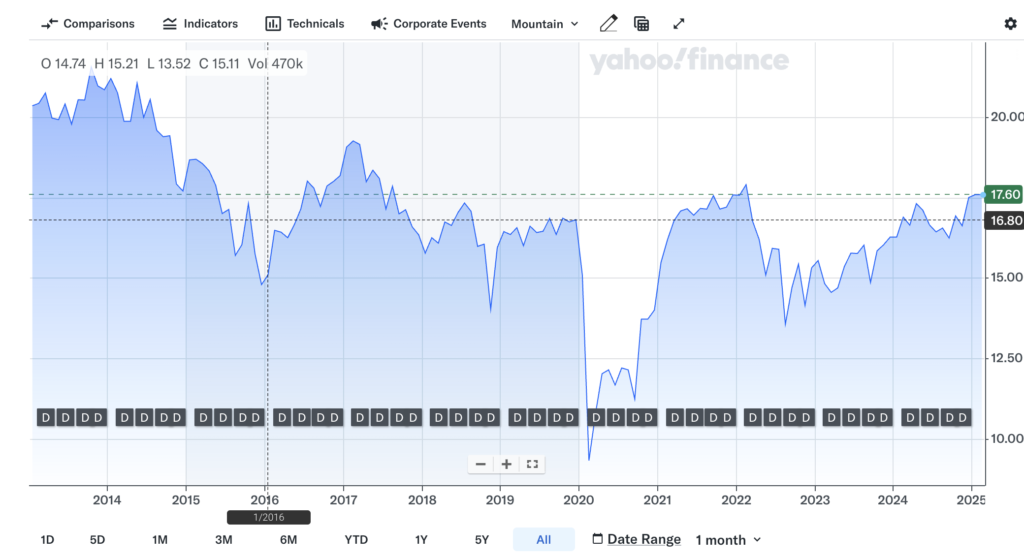

If you’ll forgive us one more chart – BIZD’s performance since coming to market 12 years ago – periods of price euphoria have often been followed by vertiginous falls.

There are four showing up here and its been 30 months since the last pullback.

Not Causation

We’re not saying that high prices cause the price downturns.

In all 4 cases exogenous events like Covid or (unreasonable) concerns about the broader economy are the villains caused the price drops.

However, those declines are all the more jarring coming from multi-year highs.

Nobody Knows Anything

If nothing else, experience teaches us that yesterday’s stock price tells us nothing about tomorrow’s and anything can happen.

BDC investors may see prices continue to rise on the promise of an unexpected improvement in BDC earnings, or they might bumble along from here after 15 weeks of rallying or could fall off a cliff, as they’ve done before.

Sentiment – which is the tendency of investors at all times to look ahead and believe they can ascertain what’s coming down the road – will be key.

Many commentators – us included – have been surprised about how bullish investors have been, both before and after the election so – as always – there’s no telling what comes next.

Quiet Confidence

We do take comfort from our work here at the BDC Reporter – and at our sister publication, the BDC Credit Reporter – which indicates that BDC credit conditions (as recently discussed )are stable; balance sheets are not too leveraged and are well leavened with unsecured debt; liabilities and there is plenty of liquidity available.

Those factors seem to help little in the short term price-wise when the sector is first hit by any turbulence but they are critical to recovery down the road.

We’d say that for a number of reasons we won’t get into here, the BDC sector has rarely been in better shape where fundamentals are concerned, which helps us sleep a little better at night.