Blue Owl Capital: IQ 2025 Credit Review

INTRODUCTION

We have edited Blue Owl Capital’s (OBDC) IQ 2025 earnings conference call transcript to focus only on issues relating to the BDC’s credit performance. Based on the research we’ve undertaken in the latest 10-Q and at the BDC Credit Reporter we’ve added – where appropriate additional data and commentary to fill out the picture.

AGENDA

OBDC has recently ballooned into a public bdc giant, with a market capitalization assets of $7.5bn. The BDC began in early 2016 with just over $200mn of portfolio investments and nine years later has managed to increase its portfolio to $17.7bn while increasing its net asset value per share over time. All the more reason for the bdc reporter to have a close look at the bdc’s credit performance.

Corporate Participants

Craig William Packer Blue Owl Capital Corporation – CEO & Director

Jonathan Lamm Blue Owl Capital Corporation – CFO & COO

Logan Joseph Nicholson Blue Owl Capital Corporation – President

Michael Mosticchio Blue Owl Capital Corporation – Head of Investor Relations

Conference Call Participants

Brian J. Mckenna Citizens JMP Securities, LLC, Research Division – Director & Equity Research Analyst

Casey Jay Alexander Compass Point Research & Trading, LLC, Research Division – Senior VP & Research Analyst

Finian Patrick O’Shea Wells Fargo Securities, LLC, Research Division – Vice President and Senior Equity Analyst

Maxwell Fritscher Truist Securities, Inc., Research Division – Research Analyst

Mickey Max Schleien Ladenburg Thalmann & Co. Inc., Research Division – MD of Equity Research & Supervisory Analyst

Robert James Dodd Raymond James & Associates, Inc., Research Division – Director & Research Analyst

Sean-Paul Adams

Presentation

Craig William Packer Blue Owl Capital Corporation – CEO & Director

MERGER/ FINAL NAV

As a reminder, we completed the merger between OBDC and OBDE on January 13. So our first quarter results now represent the combined company. As of quarter end, our net asset value per share was $15.14, down slightly from the prior quarter. That said, the fundamental performance of the portfolio remains strong, credit quality is solid, and our nonaccrual rate continues to be well below the industry average. While we’re now operating in a more normalized earnings environment, we remain confident in the credit quality of the portfolio.

TARIFFS

.. With uncertainty around tariff policy, ensuing equity sell-off in April and the possibility of an economic slowdown, we took the opportunity to reevaluate the health of our entire portfolio by re-underwriting our investments through the lens of potential scenarios for the months ahead. Following this review, we are confident that OBDC is well positioned to navigate these uncertain times. As was the case during the COVID pandemic in 2020 and the regional banking crisis in 2023, our portfolio is built for resilience during economic disruptions. Our team has been through seismic events before, and we are actively monitoring the portfolio in real time, maintaining constant dialogue with our portfolio companies, sponsors and partners to proactively address any issues that may arise.

BDC Reporter Adds: No BDC that has addressed the issue of tariffs as yet – and that’s most of them – has expressed anything more than the most modest of concern about the impact of the new measures. OBDC is no exception.

PORTFOLIO POSITIONING

While the economic outlook remains unclear, we believe we are entering this period from a position of strength. Performance across our portfolio companies remains healthy, which we believe is a result of our weighting towards defensive sectors. This stands in stark contrast to the public fixed income markets, which are more meaningfully skewed towards cyclical industries such as building products, retail, autos, energy and chemicals, sectors in which OBDC generally has not invested. …Approximately 94% of our portfolio companies are based in the United States and primarily serve domestic customers, limiting exposure to international trade disruptions. Our top sectors are primarily service-oriented such as healthcare, business services, financial services or software, which reduces reliance on manufactured goods or commodities and minimizes direct tariff impacts.

TARIFF EXPOSURE

We estimate that our exposure to companies with significant offshore manufacturing is limited to mid-single digits of the portfolio. Additionally, these businesses generally have diverse product sourcing capabilities and experienced management teams that have successfully navigated previous tariff or supply chain disruptions. This was by design. Since inception, we’ve built our portfolio to withstand turbulent economic environments and believe we will be a safe port in the storm. That said, we remain quite cautious about the impact of potential negative economic developments that our portfolio companies might face, including the possibility of broader recessionary pressures. This is why we’ve taken a proactive approach in response to the recent policy announcements by focusing on what we can control and quickly addressing any challenges that arise.

The majority of our portfolio companies are backed by private equity sponsors, who are skilled operators with significant equity investments in these businesses. This is particularly important during more volatile times as these sponsors have substantial financial resources, including ample dry powder to support their investments for extended periods of stress as we saw during COVID.

BDC Reporter Adds: OBDC – like most other BDCs – frames the threat of tariffs in very conventional terms: as to whether portfolio companies are unduly reliant on importing or exporting and where the company is domiciled. Also, management is arguing that they lend to non-cyclical businesses – those less likely to be as seriously impacted by a recession that might be triggered by what is happening. We’re not economists but we have the suspicion that the changes being made in the world order – and the subsequent impact on BDC leveraged borrowers – cannot be so readily categorized. As a result, we take very little comfort from these reassurances and those of its peers at this early stage of the great tectonic shift.

LOAN LEAD

Additionally, we are a lead or co-lead lender on roughly 90% of deals and administrative agent on approximately 65% of our investments across our platform, which gives us direct access to real-time information on borrower performance.

STRESS SIGNALS

To date, we have not seen any material signs of stress such as increased revolver borrowings, request for interest payment modifications or late interest payments. We also benefit from a strong balance sheet and significant liquidity, supported by diversified and flexible funding sources to allow us to be resilient and invest across all market environments.

BDC Reporter Adds: During the Covid crisis, analysts and investors were always asking about any pick-up in borrower amendment requests. These are seen as some of the earliest warnings that deterioration is occurring credit-wise. However, we would add that it’s way too early to take the absence of those requests through May 8 as a sign of the all clear. Much more valuable will be to learn what happens on this score in the second half of 2025.

Logan Joseph Nicholson Blue Owl Capital Corporation – President

UMM FOCUS

Notably, with an average deal size of approximately $2 billion this quarter, we continue to see the market migrate towards larger, more diversified credits. With the addition of first quarter originations, the median EBITDA of our portfolio borrowers grew slightly to $120 million and weighted average EBITDA increased to $215 million….

LOAN PRIORITY

Over the last year, OBDC’s first lien investments have grown from 73% to 77% of the portfolio. .

PORTFOLIO COMPANY PERFORMANCE

Portfolio company revenues and EBITDA once again increased in the mid- to high single digits year-over-year. We would highlight this is approximately double the U.S. GDP growth rate due to our durable noncyclical sector selection, which should provide our borrowers more cushion in a potential recession.

BDC Reporter Adds: Other BDCs have made similar claims about the growing sales and EBITDA of their borrowers, signaling by implication improving financial performance. That may or may not be true. We know that many borrowers have been busy making bolt-on acquisitions, often financed by the lenders. This data we are being quoted may include the impact of those acquisitions and not take into account the additional debt outstanding at the acquiror/BDC borrower and thus may not reflect organic growth.

DIVERSIFICATION

The portfolio also remains highly diversified with an average investment size of approximately 40 basis points, and our top 10 investments represent approximately 22% of the portfolio, down from 24% in the prior quarter.

LTV

Our average LTV is just over 40%, which provides significant support underneath our capital.

NON ACCRUALS

… The non accrual rate as of quarter end was 0.8% at fair value and 1.4% at cost compared to 0.4% and 1.9% in the prior quarter. The change reflects two additions, including National Dentex Labs and the removal of three positions that were fully exited. Stepping back, our non accrual rate remains at the lower end of our broader sector averages.

BDC Reporter Adds: The non-accrual not mentioned by name is EOS Finco SARL. For all the details about this French telecommunications company, check out the BDC Credit Reporter. OBDC exposure at cost is $23mn and the FMV $15mn.

The 3 positions “fully exited” from non-accrual are H-Food; Tall Tree Foods and CIBT Global. All resulted in realized losses which aggregated around ($155mn). The bulk of the loss was in H-Foods – around ($115mn). Read the whole story – which also involved Ares Capital (ARCC) –here.

The IQ 2025 realized net realized loss is greater than OBDC’s net losses aggregated over the last 3 years.

WATCH LIST

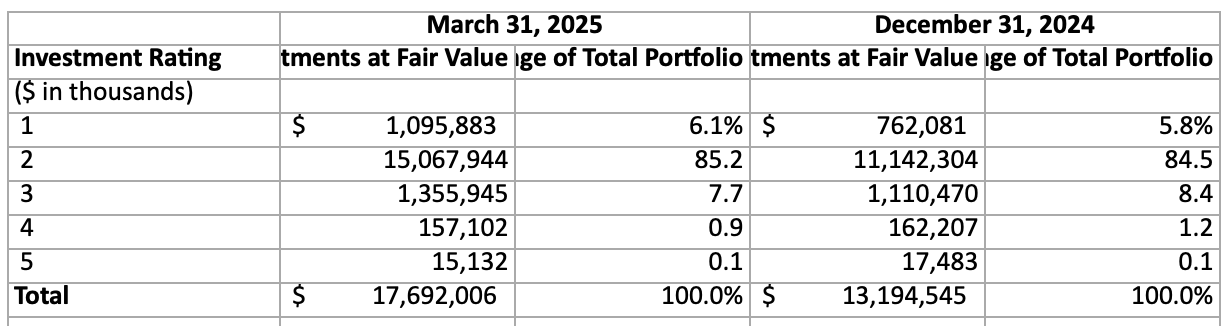

Next, our internal rating system, which ranges from 1 to 5 as an indicator of portfolio health remains steady and the subset of names on our watch list was also stable quarter-over-quarter.

BDC Reporter Adds: Not mentioned on the CC, but featured in the 10-Q is the BDC’s investment rating of its portfolio. Given that the size of the portfolio has changed sin ce the end of 2024 because of the merger, the percentage of assets in the bottom 3 ratings – all different shades of under-performing – may be the most interesting metric. Combined ratings 3-5 have dropped from 9.7% to 8.7% of the portfolio. The worst of the worst – category 5 – is much unchanged, even after the realized losses as is category 4.

Over at the BDC Credit Reporter we tackle quantifying weaker assets a little differently. We have identified only 5 “Important Underperformers” – companies likely to result in material realized losses down the road. These include both the new non-accruals and the recently written about Peraton Corp. BDC Credit Reporter estimate OBDC could book further losses on these companies amounting to ($148mn). That amounts to just under ($0.30) per share, or a decline in NAVPS – everything being equal – of only (2.0%).

Debt Service Coverage

Interest coverage remained steady at 1.8x based on current spot rates, up from trough levels as lower rates have benefited our borrowers, which should provide them a bit more flexibility during this period of uncertainty.

BDC Reporter Adds: It’s important to remember that just over a year ago when interest rates were flying high some analysts and investors were deeply wooried that many BDC borrowers would have insufficient cash flow to meet debt service requirements. Widespread defaults even of companies performing. to expectations was held out as a possibility. Upper Middle Market companies, like those financed by OBDC were the most vulnerable to this perceived risk given that they typically carry the highest level of debt. As we know, none of that has happened and that risk – always a bit of a mirage – is receding even as market observers find new risks to worry about.

PAY-IN-KIND

PIK income declined to 10.7% of total investment income from 13.2% last quarter, driven by several investments that converted to all cash pay as well as the merger with OBDE, which had lower levels of PIK exposure. As we’ve highlighted in the past, the vast majority of this PIK was underwritten at inception rather than as a result of credit issues, and these investments continue to perform as expected.

BDC Reporter Adds: We’ve taken a look at OBDC’s PIK and found little to worry about. Only a small fraction of borrowers are paying anything in kind and – as management says – most PIK arrangements were made at inception rather than granted as a desperate attempt to keep a borrower afloat. (There are a couple of occasions where that was the case but the impact on earnings was not material).

Jonathan Lamm Blue Owl Capital Corporation – CFO & COO

SIZE

Following completion of the merger with OBDE, we ended the quarter with total portfolio investments of nearly $18 billion, total net assets of nearly $8 billion and total outstanding debt of approximately $10 billion.

BDC Reporter Adds: According to OBDC’s investor presentation, its the “second largest publicly traded business development company (BDC) by market capitalization”. The BDC’s peers from a credit standpoint are Ares Capital (ARCC); Blackstone Secured Lending (BXSL); FS-KKR Capital (FSK) and -arguably – Palmer Square BDC (PSBD).

NAVPS CHANGE

Our first quarter NAV per share was $15.14, down $0.12 from the last quarter. The decline was primarily driven by changes in credit spreads and write-downs on a small number of high-focus investments.

BDC Reporter Adds: As is often the case with BDCs, management is not offering much in the way of details here. The 10-Q, though, does mention some of these “high focus investments”:

These are not immaterial write-downs. In toto, they amount to nearly ($50mn), or a quarter of what OBDC earned in Net Investment Income in the quarter.

LEVERAGE

We finished the quarter with net leverage of 1.26x, up from 1.19x and just outside of our target range of 0.9x to 1.25x, which is partly attributable to the onetime leveraging event of the merger with OBDE.We also had visibility into a couple of large repayments that slipped into April. And as a result, we expect net leverage in Q2 will be within our target range.

Questions and Answers

Operator

Robert James Dodd Raymond James & Associates, Inc., Research Division – Director & Research Analyst

You’ve answered the spread in M&A one really clearly and in case you got the liability one. So the Board one, going back to kind of your opening remarks here. I mean, at this point in your underwriting case when you’re looking at new deals, what are you ranking maybe qualitatively, not quantitatively, necessarily, as the probability of a near-term recession. I mean you always put one into kind of your underwriting case and for a lot of your businesses, they’re not that economically sensitive because of the services side. But how has that kind of near-term view like the second half of ’25, has that view changed on the probability of a meaningful or moderate economic slowdown?

Craig William Packer Blue Owl Capital Corporation – CEO & Director

Sure. So look, I’ll try to answer your question, but I’m going to just try to give a broader lens to it. We’re — the economy can be gangbusters, and we’re running downside cases. We’re — every deal, every investment we’ve made in our history has a recession case in it. Every deal in our history has a liquidation case in it. So we’re extremely downside focused, and it’s a hallmark of our underwriting process. In addition to that, as you know, we’re buying businesses, we’re investing in businesses, excuse me, that are not that cyclical. That is also a hallmark of our investment process, software, insurance brokerage, healthcare, food and beverage, mostly U.S. businesses, mostly stable, mostly annuity-like revenue streams. That’s what we like to invest in.

I’ll also repeat what we said in our prepared remarks, we’re not seeing any economic weakness in our portfolio companies. Now we are not a forward indicator of the U.S. economy because we’re selecting into the most stable parts of the U.S. economy. So we wouldn’t see it, but we’re not. If what you’re asking me is, are we especially concerned about an economic slowdown in our underwriting process. I think the answer is yes. We are.

I mean we follow economic developments as closely as I think most investors would. And there have been seismic changes to U.S. trade regulations that many feel are going to potentially impact the economy later this year. And so of course, we’re taking a serious look at that and factoring that into our base case rather than our downside case. So I think that’s just sort of responsible lending in this kind of environment, and we are a downside in orientation. So we’re taking that into account, and that’s probably our expectation.

It’s not going to change the kinds of investments we’re making because we would have already selected out of the type of investments that would be most impacted by that type of a downturn. But it’s certainly on the margin makes you that much more cautious about how much leverage you put on a business that even though it’s not cyclical, like every business is impacted if there’s a recession and even very stable ones. So we are certainly factoring that in, and it’s — we insist that introduces a level of caution as we look to deploy additional capital.

Robert James Dodd Raymond James & Associates, Inc., Research Division – Director & Research Analyst

Got it. Got it. Now one more, if I can. I mean on — the businesses have been combined. The asset base is bigger. You’ve got a little bit more room arguably now under your nonqualified bucket or any of these other diversified lending strategies that you follow between Wingspire, et cetera. I mean, any incremental — and I think I asked you about this last quarter, but any incremental thoughts on like now that they’re combined bigger balance sheet, how much of that non-pure traditional first lien, I’m not saying it’s high risk or anything, right? But those differentiated strategies you want within this vehicle.

Craig William Packer Blue Owl Capital Corporation – CEO & Director

So as you’re alluding to, at OBDC, previously, we had fairly meaningful investments in a number of essentially portfolios of assets in an asset-based lending business. We have a syndicated loan joint venture, our aircraft and railcar equipment finance, give or take, those are measured in the low double digits of the asset pool. OBDE had much less. And so we would certainly look to true up the combined portfolio and essentially get a portion of incremental exposure by just getting the combined asset base to where OBDC was previously. These have been really good investments.

Again, there — the underlying pools of assets within each of these investments are diversified pools — diversified pools of loans. Typically, we have a life insurance settlements business, a drug royalty business. The diversified underlying pools that have delivered depending upon the structure of low to middle — low to mid-teens ROE. So they’re accretive to OBDC. We think they’re risk appropriate. And over time, we’d like to continue to grow our exposure to the existing ones.

And if we could find one or two additional strategies to invest in, we would do that as well. Again, today, it’s a combined low double digits. We’re going to be patient as we grow this. But over the next couple of years, if we could take that number up to 15% versus 12%, I think that would be very valuable for shareholders. And we’re working with experienced teams that have good deal flow, chunky opportunities and we’ll look to support them and find good investments through that venue.

BDC Reporter Adds: On recent occasions when we’ve had the opportunity to wax on about the outlook for Private Credit one of our top themes has been that new category of assets are being added to what was previously an industry devoted to financing leveraged buy-outs. Private Credit is not going to double or triple in size on the back of LBOs alone in the years ahead, but is going to add all sorts of other assets to finance. OBDC, probably given its size and the growth aspirations of its external asset manger, has embraced many of these new asset categories. As the discussion above makes clear the BDC will continue to add more investments and look for new categories. The BDC Reporter, though, is dubious about this expansion of Private Credit. There is typically very little information available to investors about the assets being financed and the risks therein. This is already making investing in OBDC more of a “black box” than has been the case previously.

Maxwell Fritscher Truist Securities, Inc., Research Division – Research Analyst

You had mentioned the decrease in PIK from borrowers transitioning to cash pay. Do you have any visibility in the near, maybe medium term for other borrowers to do the same?

Logan Joseph Nicholson Blue Owl Capital Corporation – President

Sure. Exactly right. So in the first quarter, we had five names that went from partial PIK to fully cash pay. And so we do have visibility to others likely going off their PIK options. Again, some of these windows are at the borrower’s option. And so sometimes it’s voluntary and sometimes it’s time-based. But we do have visibility, and we expect our PIK to be consistent. We, at this point, have had a number of quarters in a row back through the full year 2024, where we’ve been range bound on PIK, and we’ve had now a couple of quarters of decline.So we would expect our PIK to be consistent based on our visibility so far. And also last year, we had the benefit of a number of refinancings. So opportunistic refinancings of junior capital into delevered capital structures into first liens or simply takeouts with cash flow. And to the extent that the markets are open and active in terms of refinancings, we will continue to see that.

CONCLUSION

Hanging In There

Through the IQ 2025, OBDC’s credit performance remains pretty good by the many metrics market participants use to measure performance.

Moreover – based on what we are told – more than nine-tenth of the investment assets owned are performing as expected and the BDC is increasing its proportion of “safer” first lien assets.

Management confidence is high, even when the subject of tariffs is taken into consideration.

Like ARCC and BXSL, OBDC can point to very modest non-accrual levels at cost and FMV and which are even better than their historical averages.

And Yet…

With that said, the BDC Reporter believes the data does suggest a weakening at the margins in credit performance.

Entered Into Evidence

Exhibit A are the substantial realized and unrealized losses booked in recent quarters, and especially in the IQ 2025.

Material amounts of income has been permanently lost because of those setbacks.

Furthermore, write-downs in the most recent quarter and the addition of 2 new non-accruals are reminders that this trend is likely to continue in the quarters ahead.

Also, an increasingly large number of assets are in categories that outside observers cannot properly evaluate and whose performance over the long term is not yet known.

Credit vigilance is always called for where BDCs are concerned but it’s even more vital where OBDC – whose portfolio growth has been very rapid (AUM has doubled in 5 years) – is concerned.

So far so good for OBDC but the journey of a thousand miles has only just begun for this gigantic BDC.

Already a Member? Log In

Register for the BDC Reporter

The BDC Reporter has been writing about the changing Business Development Company landscape for a decade. We’ve become the leading publication on the BDC industry, with several thousand readers every month. We offer a broad range of free articles like this one, brought to you by an industry veteran and professional investor with 30 years of leveraged finance experience. All you have to do is register, so we can learn a little more about you and your interests. Registration will take only a few seconds.