An Introduction To The WhiteWolf Publicly Listed Private Equity ETF (ticker: LBO)

June 23, 2026

INTRODUCTION

For income-oriented investors, the playbook for capturing middle-market credit yields has traditionally been straightforward: buy common stocks of individual Business Development Companies (BDCs) or a broad passive index like the VanEck BDC Income ETF (BIZD). However, as the private credit and leveraged buyout landscapes grow more complex, navigating risk requires looking beyond standard wrappers. In this exclusive interview, we ask 5 revelatory questions of the management team behind the WHITEWOLF Publicly Listed Private Equity ETF (ticker: LBO), an actively managed vehicle that blends BDC exposure with listed private equity sponsors and asset managers.

________________________________________________________

1. Origin Story and Core Investment Mandate

BDC Reporter: "Could you walk us through the history and founding vision behind the WHITEWOLF Publicly Listed Private Equity ETF (LBO) since its launch in late 2023? Specifically, how do you define its core mandate, and what are the strategic goals you aim to achieve for investors that differ from a pure-play BDC index?"

A: "White Wolf Capital is a private investment firm founded in 2011. We are an SEC-registered investment advisor with approximately $600 million in assets under management. White Wolf Capital's investment strategies include Corporate Private Equity, Private Credit, and Private Fund Investing. We manage capital for both public and private institutions, including pension funds, family offices, RIAs, and high-net-worth individuals. With respect to LBO, we wanted to create a product that was an "easy button" for the wealth management channel, as well as for the DIY investor who wants a liquid, diversified way to invest in the private market ecosystem as a whole. LBO is an. actively managed income-oriented ETF that provides investors with exposure to certain components of the leveraged buyout ecosystem. This ETF invests in publicly listed private equity buyout firms & publicly-listed sponsors, Business Development Companies (BDCs), leverage providers, and related asset managers. Unlike a pure-play BDC ETF, LBO seeks long-term capital appreciation (which you don't typically see from a BDC ETF) while providing an opportunity for current income. In fact, BDC ETFs tend to exhibit flat-to-down price trends because they must distribute 90% of their earnings.

In fairness, you invest in BDCs for total return, including dividends. LBO mitigates this natural price decay by overlaying the PE manager stocks, which provide the potential for long-term capital appreciation. It is important to note that when we set out to design a product we thought was best for the wealth management channel, we researched various wrappers, including "semi-liquid" interval funds.

Ultimately, we decided to go with the more liquid ETF wrapper because our mandate was twofold: private-market exposure and liquidity. The retail investor or RIAs don't have to deal with redemption gates or limits - you want out, hit the sell button. This is particularly relevant because it sidesteps the redemption issue, which is arguably the main driver of many of the negative headlines you see about private credit. In our opinion, the most efficient way for the retail investor to gain exposure to private credit or private markets is to invest in BDCs rather than interval funds. The spread between interval fund yields and BDCs is simply not there to warrant a lock-up. i.e., you are not compensated for the illiquidity premium.

2. Asset Allocation: The Intersection of BDCs and Private Equity

BDC Reporter: "As you've already noted, LBO takes a unique approach by blending exposure across the leveraged buyout ecosystem—investing not just in traditional asset managers and buyout firms like Blackstone or Apollo, but heavily utilizing Business Development Companies (BDCs) like Ares Capital (ARCC) and Blackstone Secured Lending (BXSL). How do you balance the equity upside of listed private equity sponsors with the yield-heavy, debt-focused profile of BDCs, and what specific qualitative or quantitative criteria dictate your asset mix?"

A: LBO is differentiated in that it has components of both BDCs and Private Equity stocks. It is the first (and only) actively managed ETF that does this. Our strategic allocation between BDCs and non-BDCs depends on our outlook - we tilt more towards publicly traded PE names when we believe that the sector is undervalued and/or is poised for upward price movement. Under certain market conditions, when we want to adopt a more defensive posture, we tilt the strategic allocation toward greater exposure to BDCs.

3. The Active Management Advantage vs. Passive Indexes

BDC Reporter: "For income-focused investors, passive vehicles like the VanEck BDCIncome ETF (BIZD) are standard benchmarks. LBO, however, is actively managed and has a broad mandate across small, mid, and large-cap listed private equity companies. How does your active management approach protect capital or capture alpha during periods of market stress, and what should readers understand about how your daily trading and security selection process actually operates 'under the hood'?"

A: Given that LBO is managed by a firm that operates primarily in the private equity space, its management team can leverage that boots-on-the-ground knowledge (as well as its more than 15 years of experience) to select the fund’s portfolio. We always go back quarterly to ensure that all underlying holdings align with our thesis. LBO's holdings are under constant review, with each 10-K and 10-Q scrutinized as they become available. We listen to earnings calls and analyze investor presentations. In general, we tilt towards more liquid names and higher-quality BDCs. We are tracking operating metrics over time, including portfolio performance, dividend quality, cash vs. PIK interest composition, and other factors.

4. Navigating Current Market Conditions and Historical Returns

BDC Reporter: "Given the shifting interest rate environment and evolving credit quality trends we've observed over the past year, how has the fund’s strategy held up regarding historical total returns and dividend distributions? Which segments of your portfolio—the direct lenders/BDCs versus the private equity sponsors- have done the heavy lifting in this current economic environment?"

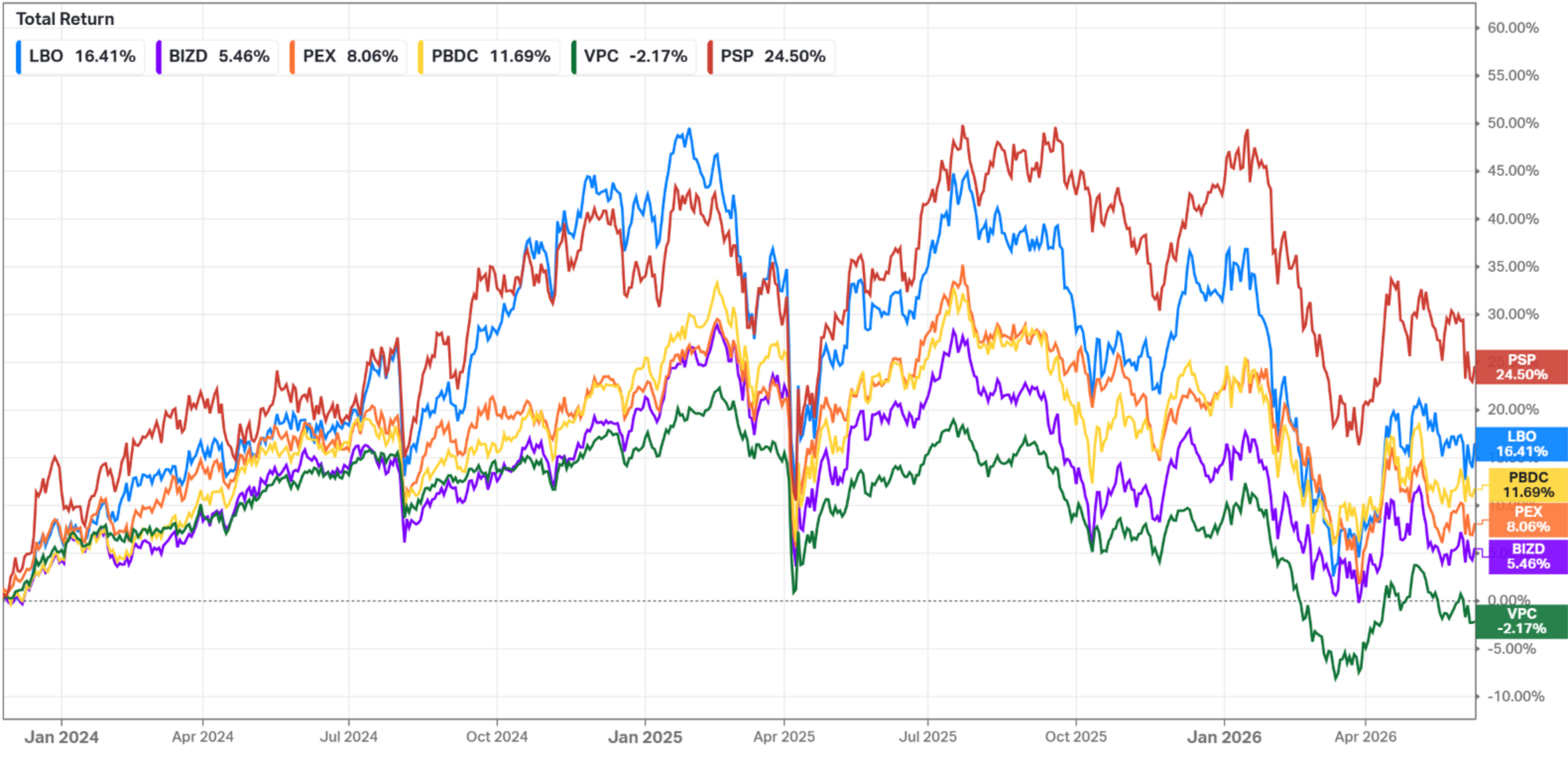

A: As your readers know better than anyone else, the whole private market is down. However, we are proud to say that LBO has performed meaningfully better than some other private market ETFs (when measured using total return since LBO’s inception through today).

With regard to your question about which segment of the portfolio did the heavy lifting, I would say the publicly traded private equity sponsors did. That is because the publicly traded private equity managers provided a lift in the form of price appreciation, whereas some of the other passive BDC ETFs saw their dividend income not enough to offset price drawdowns.

5. Macro Outlook: The Future of Public PE and Middle-Market Credit

BDC Reporter: "Looking ahead, what is your outlook for the public-private equity and BDC sectors? As middle-market lending faces increased competition and shifting macroeconomic indicators, where do you see the most compelling risk-adjusted opportunities for LBO, and what primary risks are you actively managing against?"

A: Our outlook for the public-private equity and BDC sectors in 2026 remains cautiously constructive, but we believe that investors have to be highly selective. This aligns with our view that we remain in the early innings of broader adoption of alternatives, with meaningful opportunities for patient, active capital across both public and private channels. Private markets have matured significantly since the post-GFC acceleration, with institutional allocations to alternatives rising substantially, and a clear shift is underway toward broader adoption by high-net-worth and individual investors moving beyond traditional 60/40 portfolios. Publicly listed players—private equity sponsors, asset managers, and Business Development Companies (BDCs)—stand to benefit from normalizing deal and exit activity, though alpha will increasingly come from operational value creation, specialization, manager selection, and thematic exposure rather than from broad market tailwinds such as declining rates or expanding multiples.

Core middle- and lower-middle-market segments generally appear more resilient, often featuring stronger creditor protections, conservative structures, and relatively higher risk-adjusted yields, with competition less intense than in the BSL segment. Asset quality has remained generally stable, but managers must navigate potential credit stress in cyclical or highly leveraged names amid a maturing private credit landscape.

For the LBO ETF, we believe that the most compelling risk-adjusted opportunities lie in inactive, fundamental-driven selection across the publicly listed leveraged buyout ecosystem—specifically, high-quality BDCs and leading buyout sponsors/asset managers with strong middle-market or infrastructure exposure. Our approach prioritizes high-quality originators with scale and expertise, thematic resilience (e.g., infrastructure and AI-enabled businesses), diversification across ~40 holdings, and active rebalancing based on fundamental analysis of filings, manager capabilities, and credit metrics.

BDC Reporter Adds:

We thought our readers would appreciate this chart, which compares the total return performance of LBO with several other related publicly traded investments. These include the Invesco Global Listed Private Equity ETF (PSP); the Putnam BDC Income ETF (PBDC), and - of course - the Van Eck BDC Income BDC (BIZD), amongst others.