BDC Common Stocks Market Recap: Week Ended January 16, 2026

Good Start

BDC COMMON STOCKS

Week 3

Wall Street closed the trading week modestly lower, with the S&P 500 (SP500) remaining within striking distance of the historic 7,000 level. Investor attention also focused on key inflation data, the kickoff of earnings season, and the ongoing rally in silver

Core CPI edged slightly below expectations, suggesting modest moderation in consumer inflation, while PPI met forecasts, sending a mixed signal on underlying price pressures.

For the week, the S&P (SP500) lost -0.4%, while the tech-heavy Nasdaq Composite (COMP:IND) dipped -0.7%, and the blue-chip Dow (DJI) fell -0.3%.

Seeking alpha – wallstree breakfast – january 17, 2026

Better

For the second full week of 2026, the BDC sector performed materially better than the major indices, which were all in the red.

Our favorite guidepost for BDC sector performance – the change in the price of the Van Eck exchange-traded fund with the ticker BIZD – was up 1.3%.

The alternative measuring tape is the price change in the S&P BDC Index, which moved up 1.10%.

In The Weeds

If we examine the price performance of the 46 BDCs we track, which have $170 billion of portfolio assets, we find that 32 were up in price – or unchanged – week over week, while 14 were down.

Coincidentally, these are the same metrics as a week ago.

8 BDCs increased in price by 3.0% or more, twice as many as last week, and the best performance in over a month by this standard.

No BDC fell in price – according to Seeking Alpha’s excellent data – by more than (1.8%).

That was CION Investment (CION), which ten days ago was one of what might be a long list of BDCs cutting their regular dividend.

Still, no BDC fell to a new 52-week low – the first time in 5 weeks that has happened.

That’s all to the good, but the number of BDCs priced at or above their net asset value per share (NAVPS) remained the same as the week before – 9

News

There were numerous BDC-related headlines this week, mostly featuring positive news that may have contributed to the buoyant prices.

Main Street Capital (MAIN) managed to report both yet another successful exit from a portfolio company and a preview of its key performance metrics for the IVQ 2025.

The latter were so strong that we felt compelled to write an article quantifying how favorable the numbers are compared to the prior quarter, analyst expectations, and other BDCs.

MAIN is having its moment at the beginning of a year when most BDCs’ results are expected to be dragged down by the heavy anchor of ever-lower interest rates.

Three cuts in the last few months of 2025 are likely to have an impact on earnings all the way into the IIQ 2026.

Unexpected

With that said – and an aside – we’ve been collecting all the analyst earnings expectations for the IVQ 2025 and comparing them to the actual results for the IIIQ 2025. Much to our surprise – and possibly to yours – we find that in aggregate dividends are expected – by the analyst community at least – to edge a little higher in the last quarter: 0.3%. That’s following several quarters of (3%) or greater declines brought on by previous interest rate decreases. Maybe there is a seasonal impact, as the fourth quarter is traditionally the busiest period of the year for lending. Also, the full impact of 0.75% in rate cuts may not yet be showing up. Or the analysts could be overly optimistic… This is setting up the fourth quarter of 2025 to be an intriguing one.

Back to the news.

We also received a preview of IVQ 2025 earnings from Capital Southwest (CSWC). The metrics were not quite as glorious as at MAIN, but the recurring earnings – at least – seem to be higher than what the consensus was.

At the very least, CSWC is holding its own in the final stage of 2025.

Elsewhere, Stellus Capital (SCM) announced monthly distributions for the IQ 2026 that were unchanged from prior periods and annualize to $1.60 a share.

As we reminded readers on our X page, where we briefly comment on all BDC news stories before choosing the ones deserving of more coverage on the BDC Reporter, SCM is projected to earn only $1.15 a share in 2026.

Clearly, management has not bent the knee where the payout to shareholders is concerned. The guessing game continues for another quarter.

Of the several BDCs that have announced 2026 dividends, most have kept their payouts unchanged (CSWC, OXSQ, PSEC, SCM) or increased them (MAIN).

The BDCs that have taken out their scissors are GLAD and the aforementioned CION.

Of course, several BDCs “adjusted” their regular distributions during the course of 2025, usually due to the impact of poor credit performance on their ability to continue paying.

These include OCSL, TCPC, and WHF.

We’ll be keeping a running list of which BDCs stand pat or increase their payouts in 2026, and which are unable to do so, and we'll share it with our readers quarterly to see how this trend is playing out.

WHERE WE ARE

Early Days

After two trading weeks and one day, BIZD is up 2.5% on a price basis, per BIZD, and up 2.5% on a total return basis, per the S&P BDC Index.

By contrast – and for what it’s worth – so early in the year, the S&P 500 is up only 1.4%, both on a price-only and total return terms.

36 BDCs are priced above their level at the end of 2025.

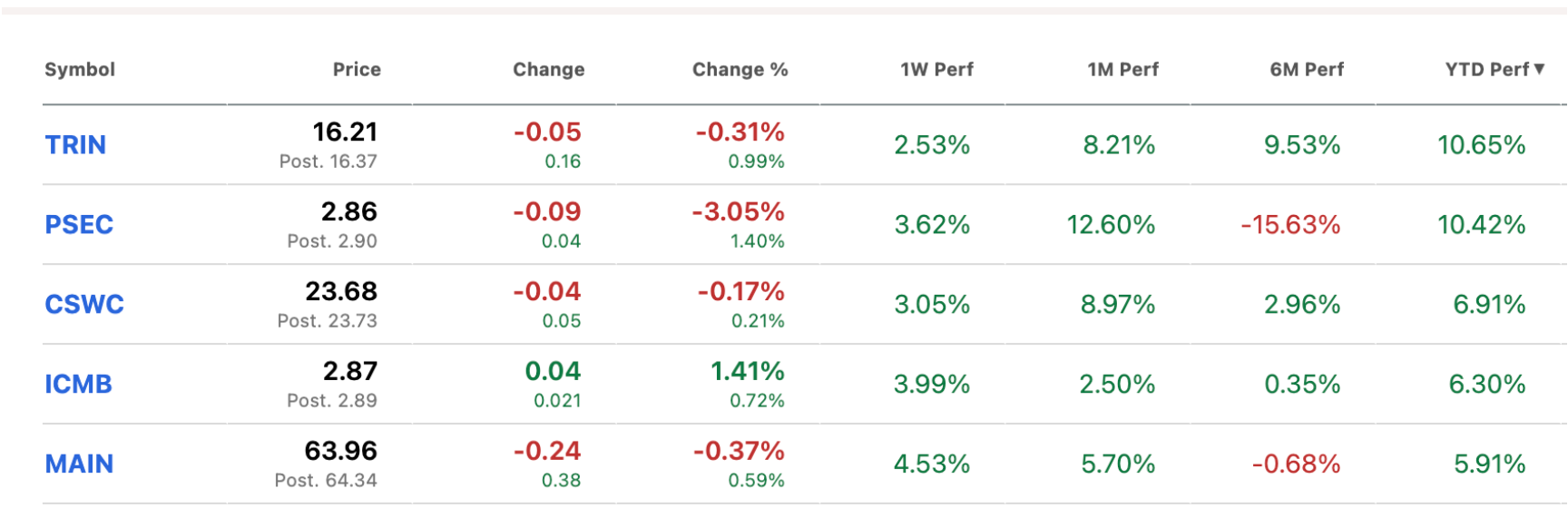

Best

Here are the 5 top performers in price in 2026:

The BDCs involved are both “quality”, popular BDCs like TRIN, CSWC, and MAIN – all trading at a premium to book – and potential “turnaround” candidates.

Long Time Going

As this chart shows, PSEC – in red – has been in a price decline since 2021, and ICMB – in yellow – since 2023.

There’s a yawning gap between their price performance and that of BIZD. – in blue.

Nonetheless, hope springs eternal.

WHERE WE ARE HEADED

Every week, the same challenge

This most important section of our weekly articles is – as usual – the hardest to write about.

We won’t repeat the concerns expressed last week – and at various times through 2025 – that interest rates might head much lower than the market – and the Fed’s “dot plot” – currently expect.

Need we say that all those analyst projections of future earnings will need to be amended if the Fed Funds rate – and by association SOFR – drops as low as 2.5% from 3.75% currently?

We suspect we would get a big price downdraft even though – as we spelled out last week – there could be indirect benefits from forcibly – and rapidly – reducing rates.

For all that, we’ll just have to wait and see.

Holding On

In the short term, though, there is a strong consensus that the Fed will not strike a fourth dividend cut this month, whatever they might choose to do later in the year.

This might bring a degree of quiet to the BDC sector, which has picked itself up from the carpet of October 2025 but has only climbed 8% since then.

Even with this robust start to 2026, BIZD is still (4%) below a peak price of $15.10 set in early December last year.

Only 2 BDCs are trading within 5% of their 52-week high, another 2 are 5%-10% off, and 17 are less than 10% above their 52-week lows.

Lighten Up

Although we’ve seen neither cracks opening up nor more cockroaches appearing in BDC credit, the mood – if that’s something one can really sense – remains a little grim.

A BDC bull might say that’s not entirely reasonable, given that everyone and his dog seems to believe that the economy is going to be stronger in 2026 than in 2025; most BDCs are reporting growing EBITDAs at their portfolio companies and – as we’ve reported – realized losses have been very modest in BDC P&Ls through the reported 2025 data.

Moreover, the broader leveraged loan/Private credit environment continues to grow and is benefiting from a pickup in LBO activity, thanks to those same lower interest rates and PE groups anxious to provide LPs with tangible returns.

BDC balance sheets – with a few exceptions – have never been stronger, and liquidity is abundant.

That should allow BDCs to either grow by increasing their leverage or strategically shrink by buying back their shares at a very profitable cost.

There may be great – and continuing – uncertainty about the future direction of interest rates – but these are hardly the worst of times for BDCs in most other ways.

Why Not?

So here’s one optimistic scenario: Rates end up not moving much further down in 2026, and BDCs continue to pay out distribution yields in the low teens – far higher than what comparable yields are in the leveraged loan, high yield, and CLO markets.

If we get just an 8%-10% price bump in 2026 over the year-end 2025 level, we could see a BDC total return north of 20.0%.

It could happen, and this sort of whiplash in total returns has occurred multiple times before in BDC history.