BDC Common Stocks Market Recap: Week Ended January 23, 2026

BDC COMMON STOCKS

Week 4

Wall Street closed the trading week lower, though equities rebounded from intra-week lows following a volatile stretch marked by heightened geopolitical uncertainty.

For the week, the S&P (SP500) lost -0.4%, while the tech-heavy Nasdaq Composite (COMP:IND) dipped -0.1%, and the blue-chip Dow (DJI) fell -0.5%.

seeking alpha – wall street breakfast – january 24, 2026

Unusual

Week 4 had all the ingredients to be a highly volatile week for asset prices generally, but, as far as the BDC sector is concerned, it ended up something of a “nothing burger”.

That’s all the more surprising given that there was a stream of BDC news to go along with the on-again off-again grabbing of Greenland; threats of a devastating trade war with the EU, and – off in the distance – cracks appearing in the Japanese bond market.

For all that, BIZD – the only BDC exchange-traded fund – dropped only (0.9%) this week, as did the S&P BDC Index.

Admittedly, many more BDCs dropped in price than stayed put or increased:34 to 12.

However, the week was notable for the relatively small price changes in either direction.

No BDC increased more than 1.9% in price, and the biggest drop was only(2.6%), and that was for a BDC that took a hatchet to its regular distribution – Stellus Capital (SCM).

We haven’t had such a lack of volatility since the week ended July 25, 2025.

More On That Score

No BDC – for a second week in a row – reached either a new 52-week high or low.

However, we can report that the number of BDCs trading at or above net asset value per share (NAVPS) dropped by one, from 9 to 8.

Many Developments

If BDC prices were relatively quiet, there was plenty of news to digest in our corner of the Private Credit universe.

We covered virtually every new tidbit on our X feed in almost real time, but here are the highlights and lowlights – going in reverse chronological order:

Hercules Capital (HTGC) renewed a very large loan facility to one of its many borrowers, proving that both the BDC and its Media Relations Dept are keeping busy.

As always, we learned very little about the economic terms of the transaction, but that will be revealed – we expect – in future filings.

More importantly, MSC Income Fund (MSIF) followed in the footsteps of its external manager, Main Street Capital (MAIN), and several other BDCs and “previewed” several key IVQ 2025 performance metrics.

As discussed in a Premium article, the numbers seemed encouraging.

We were less encouraged by PennantPark Investment’s (PNNT) own quarterly heads-up, also the subject of an article during the week.

Two BDCs tapped the ever-accommodating institutional market for medium-term unsecured notes.

Goldman Sachs BDC (GSBD) raised $400mn on favorable terms but only for 3 years.

Bain Capital Specialty Finance (BCSF) gathered up $350mn, but for a longer period – 5 years – and at a higher yield.

Both BDCs are nearing the end of several years of owning unsecured debt at remarkably low yields acquired during the ZIRP era, while having to pay a much higher interest rate on new debt.

This will be a sector-wide phenomenon all year.

Internally managed Capital Southwest (CSWC) announced a new off-balance sheet joint venture with an unknown party.

Here’s what we had to say – which mostly consisted of a series of questions – on Seeking Alpha and on X:

The BDC Reporter adds: This is a very intriguing development at Capital Southwest CSWC , but one that begs more questions. We’ve been around for a quarter of a century – or more ! – following the BDC sector and never heard of a “first out” fund. And a leveraged one to boot! Is CSWC suggesting that the JV will grab the first out position in new loans and leave the second out to be held on its own balance sheet? What sort of yield give-up will the JV have to incur to have the right to be “first out,” and what will the overall ROE of the JV look like? Are the partners truly equal where the economics are concerned, or is CSWC gaining an advantage in generating the loans? Also, who is this mysterious JV partner? There are other ways to “win high‑quality lower middle market opportunities”, like clubbing together with friendly firms or launching a non-traded BDC like MAIN did with MSC Investment (MSIF). Why this JV instead? Also, is this a sign that something is shifting strategically at CSWC and management wants to move up to larger borrowers and leave their traditional hunting grounds behind? Or just broaden their market scope? As we said, we’ve got a lot of questions…Seeking Alpha- January 23, 2026

However, the Biggest Story of all snuck quietly in as an 8-K filing – no press release was involved – on Friday afternoon.

BlackRock TCP (TCPC) published a IVQ 2025 preview of some of its performance metrics, and they were – in a word – disastrous.

We won’t get into a big discussion here because we are already halfway through an article for the BDC Reporter and will also be tackling the subject at the BDC Credit Reporter.

We’ll just quote from our post on X:

This Is Bad. We can tell you right now what the biggest BDC story of next week will be: the market reaction to BlackRock TCP’s $TCPC preliminary IVQ 2025 results. We’re working on a Premium article with all the trimmings, but one metric should speak volumes: its net asset value per share dropped (19%) in 3 months. Worst performance by any BDC in 2025…Bloomberg has already written an article, bless them. https://bit.ly/4sWtSiz. BDC Publications On X January 24, 2025

Not Budging

Anyway, all the above did little to move BDC prices.

Maybe investors are just waiting for the IVQ 2025 results, which are just around the corner, and for which we have been publishing previews all week.

WHERE WE ARE

Sign Posts

After 4 weeks, BIZD is up 1.6% – notwithstanding this week’s price reversal – and ahead of the S&P 500, which has increased by only 1.0%.

At this earliest stage, 26 individual public BDCs are up or flat, and 20 are in the red.

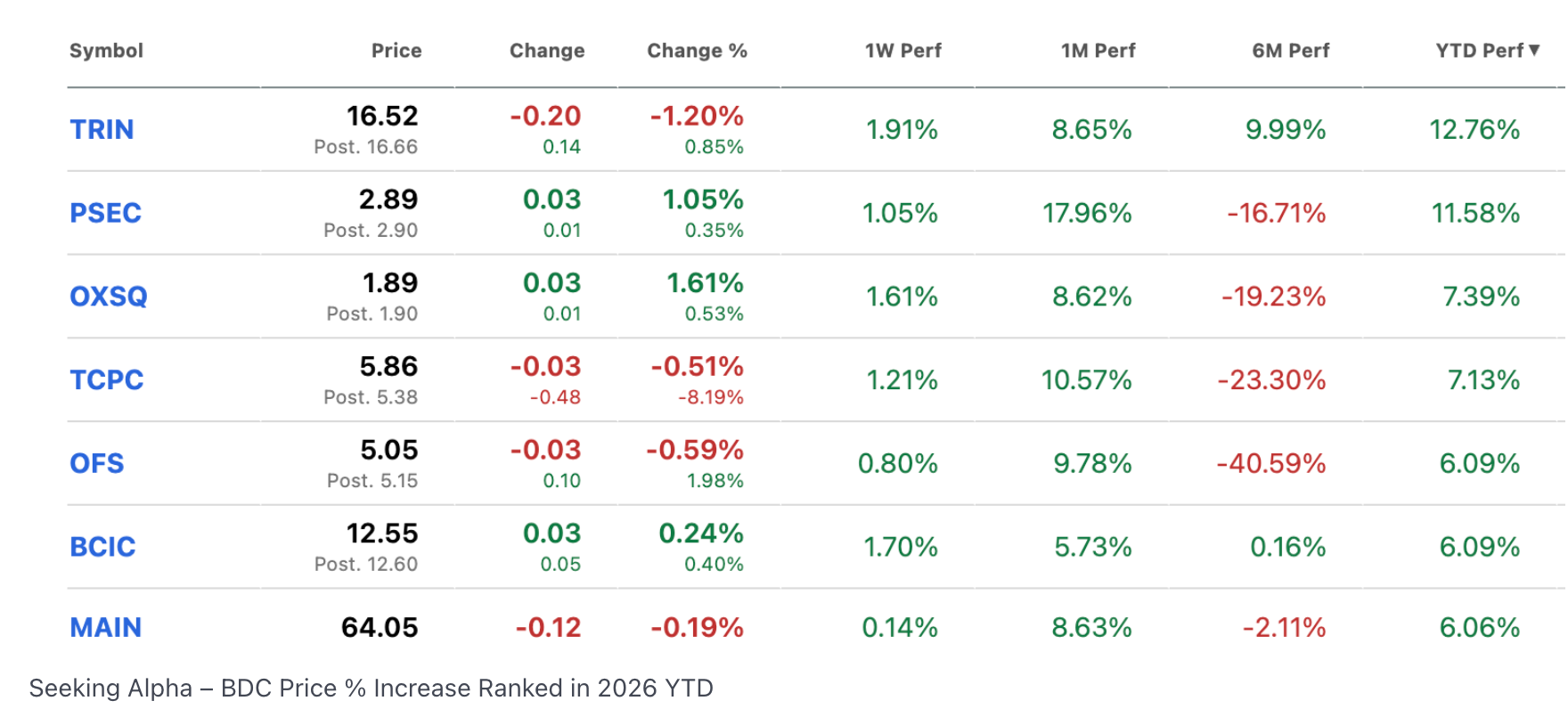

This chart shows that a handful of names have shot out of the gates in 2026 price-wise:

As is often the case, this list reflects investors reacting favorably to recent good news (MAIN) and speculators buying up price underperformers.

All we’ll say is that several BDCs on this list are being rated very poorly by the BDC Credit Reporter from a credit perspective.

Maybe the market knows something we don’t about these credit trouble spots or considers all the bad news baked into the price.

There’s a lot to gain from a BDC yielding 22.2% (as per OXSQ), but there’s still plenty of risk.

Speaking of risk, there’s only one BDC down more than (5.0%) in 2026 YTD.

That’s Blue Owl Technology Finance (OTF) – a unique player in the venture debt category.

OTF has not been able to catch the fancy of investors since going public in June of last year, and despite paying a steady dividend and attracting a high credit rating from the BDC Credit Reporter.

The BDC has lost one-third of its enterprise value from its highest price as a public company to the current level, which is very similar to Blue Owl’s other public BDC, which is often in the news, Blue Owl Capital – ticker OBDC.

WHERE WE ARE HEADED

Watching And Waiting

As we mentioned above, investors may be waiting for IVQ 2025 results to gain clarity on where the BDC sector is headed.

If so, they may soon be disappointed.

That’s because the BDC “sector” is really very disparate, and fundamental performance, even more than at any other time recently, is likely to vary widely name-by-name.

Even in market segments like the Upper Middle Market (UMM), Core Middle Market (CMM), Lower Middle Market (LMM), and venture debt, there are both winners and losers when it comes to bottom-line results.

TCPC may have chronic credit problems, but that does not mean Ares Capital (ARCC) or Blackstone Secured Lending (BXSL) – two similar BDCs also owned by brand-name asset managers – are in the same boat.

As of the IIIQ 2025 – to use but one example – TCPC’s non-accrual percentage at cost was 7.0% while ARCC and BXSL’s were 1.8% and 0.1% respectively.

Just because TCPC’s non-accrual percentage has jumped to 9.6% in the IVQ 2025 does not mean its peers will be similarly impacted.

By our count, one-third of the public BDC universe has been performing poorly for some time (including TCPC), one-third has been outperforming, and one-third are just hanging in there – neither sweet nor sour.

We’d be surprised if those proportions change very much once the IVQ 2025 earnings season is done and dusted.

The many “previews” we have received from BDCs in recent weeks confirm our suspicions, but they're only a sample.

We will find out shortly, and when earnings season is over, we’ll sum up whether any material changes have occurred.

As we roll through the results, the BDC Reporter and the BDC Credfit Reporter will share their respective performance ratings with our readers.

Let’s see who surprises us.