BDC Common Stocks Market Recap: Week Ended June 12, 2026

BDC COMMON STOCKS

Week 24

Wall Street ended the week higher as stocks rebounded from an early-week selloff, while investors weighed the latest inflation data, ongoing developments in Middle East diplomacy, and the strong debut of SpaceX. For the week, the blue-chip Dow (DJI) climbed up +0.66%. At the same time, the benchmark S&P 500 (SP00) moved up +0.65%, while the tech-heavy Nasdaq Composite (COMP:IND) added +0.70%. - Seeking Alpha-Wall Street Breakfast - June 13, 2026

Confused

We have to admit up front that the data we are about to share with you confuses us.

We've checked the numbers multiple times, but keep getting the same metrics from Seeking Alpha and other sources we regularly use.

For the week, the sector was up in price. The only BDC exchange-traded fund, sponsored by Van Eck and trading under the ticker BIZD, closed the week at $12.79, up from $12.48 a week earlier. That's a 1.8% increase.

The S&P BDC Index, calculated on a price-only basis, was up far less: 1.1%, but we're accustomed to different results from these two measuring sticks.

What confused us, though, is that Seeking Alpha shows far more BDCs going down in price this week than up: 33 to 12.

Furthermore, only 1 BDC increased by 3.0% or more in these 5 days, while 9 decreased by (3.0%) plus.

Also, the number of BDCs trading at or above their net asset value per share (NAVPS) decreased to 5 from 6 on an aggregate basis in this supposedly "positive" week.

(By the way, that's the lowest number of BDCs trading above book since March 2023).

So, objectively speaking, it's hard to say if Week 24 was a "good" week or not.

Worthy

Outside of these contradictory price signals, there were only 3 notable developments worth chewing on, 2 of which we wrote about.

Saratoga Investment (SAR) boldly announced another $ 0.25-per-month dividend for another quarter, despite earning much less in recurring income.

In an article, we tussled with the obvious question of how long this can go on and whether SAR is helping its cause by paying a dividend at such a generous level.

In a different vein, we also wrote about Ares Capital's (ARCC) groundbreaking commercial paper program - the first of its kind in the BDC sector.

Not only will this save ARCC and its shareholders financing costs, but it will also reduce its direct reliance on bank borrowings.

We expect several other of the larger BDCs to follow suit with CP programs of their own.

Canary?

Finally, not discussed during the week because we saw the filing late on Friday, Palmer Square (PSBD) announced its NAVPS for May 2026.

Because the BDC invests principally in the most liquid investments in the leveraged loan market, PSBD can provide this data every 30 days rather than every 90 days.

For BDC sector watchers, this provides an early insight into NAV trends that extends beyond PSBD alone.

Anyway, at the end of the IQ 2026, PSBD's NAVPS was $13.30, having dropped more than (10%) from the year-end 2025 number.

In April, the NAVPS improved to $13.59 and, now, in May, the metric is up to $13.63.

Over the last 2 months, that's a 2.5% increase and - need we say? - a great improvement on the first quarter of 2026's result.

Some of the improvement is undoubtedly due to the narrowing of discounts for liquid loans in the first two months of the second quarter.

Not So Fast

However, based on our research contained in this briefing note, the overall picture is very mixed.

In a nutshell - and possibly oversimplifying - higher quality loans have largely rebounded in value, but software debt values continue to be anemic.

How that might play out when the BDCs - each with a different mix of higher quality and software credits - value their portfolios in a quarter is hard to pin down.

WHERE WE STAND

More Certainty

If we're not sure how to characterize the week just ended, the situation regarding the BDC sector's price trends YTD in 2026 is clearer.

The market remains toxic for investors.

This past week, another 4 BDCs reached 52-week lows, and - as noted above - one more BDC ceased trading above book.

11 BDCs are trading within 5% of their 52 week lows and another 14 between (5%) and (10%) off the bottom.

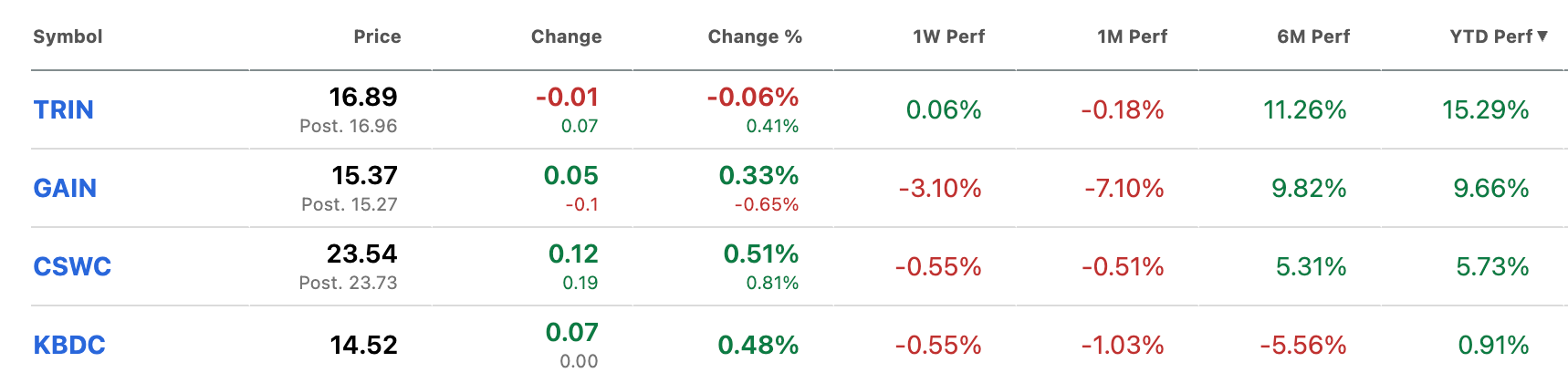

By contrast, only 2 BDCs are trading within 10% of their 52-week highs: Capital Southwest (CSWC) and Trinity Capital (TRIN).

Perennial investor favorites like Main Street Capital (MAIN), Ares Capital (ARCC), and even Gladstone Investment (GAIN) are trailing far behind the two price leaders, despite posting decent results in the IQ 2026.

On a year-to-date basis, only 4 BDCs are in the black, as illustrated below:

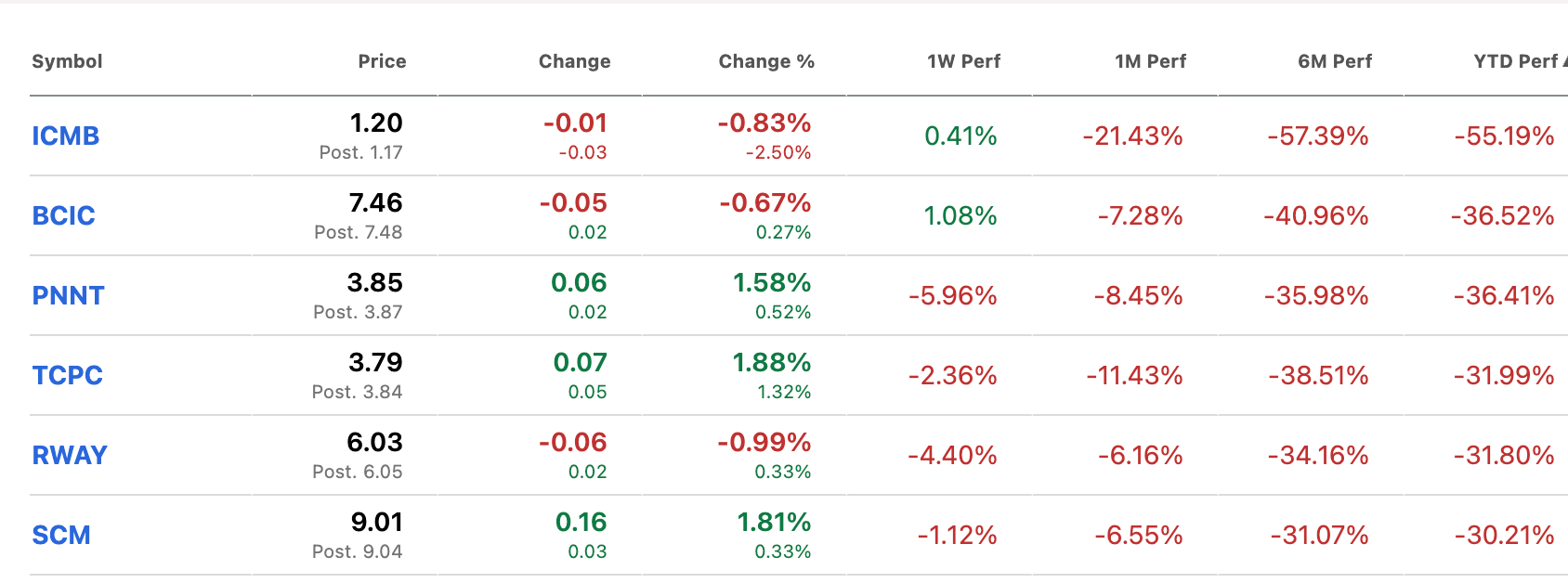

Contrast that with the percentage price drops at the 6 worst-performing BDCs:

Big Picture

Through 24 weeks, BIZD is down (10.4%) and an even worse (14%) over 6 months.

If we go back 1 year, BIZD is down (21.8%) and (27.0%) from the high point in February 2025.

This miserable performance extends to the individual BDCs as well. Only 3 are in positive price territory over the last 12 months.

Even if we roll back the clock 3 years to the very height of the BDC Golden Age, when interest rates were at their peak, only 8 BDCs have higher prices today.

All of this is to illustrate that the public BDC sector is a broad-based and long-lasting slump.

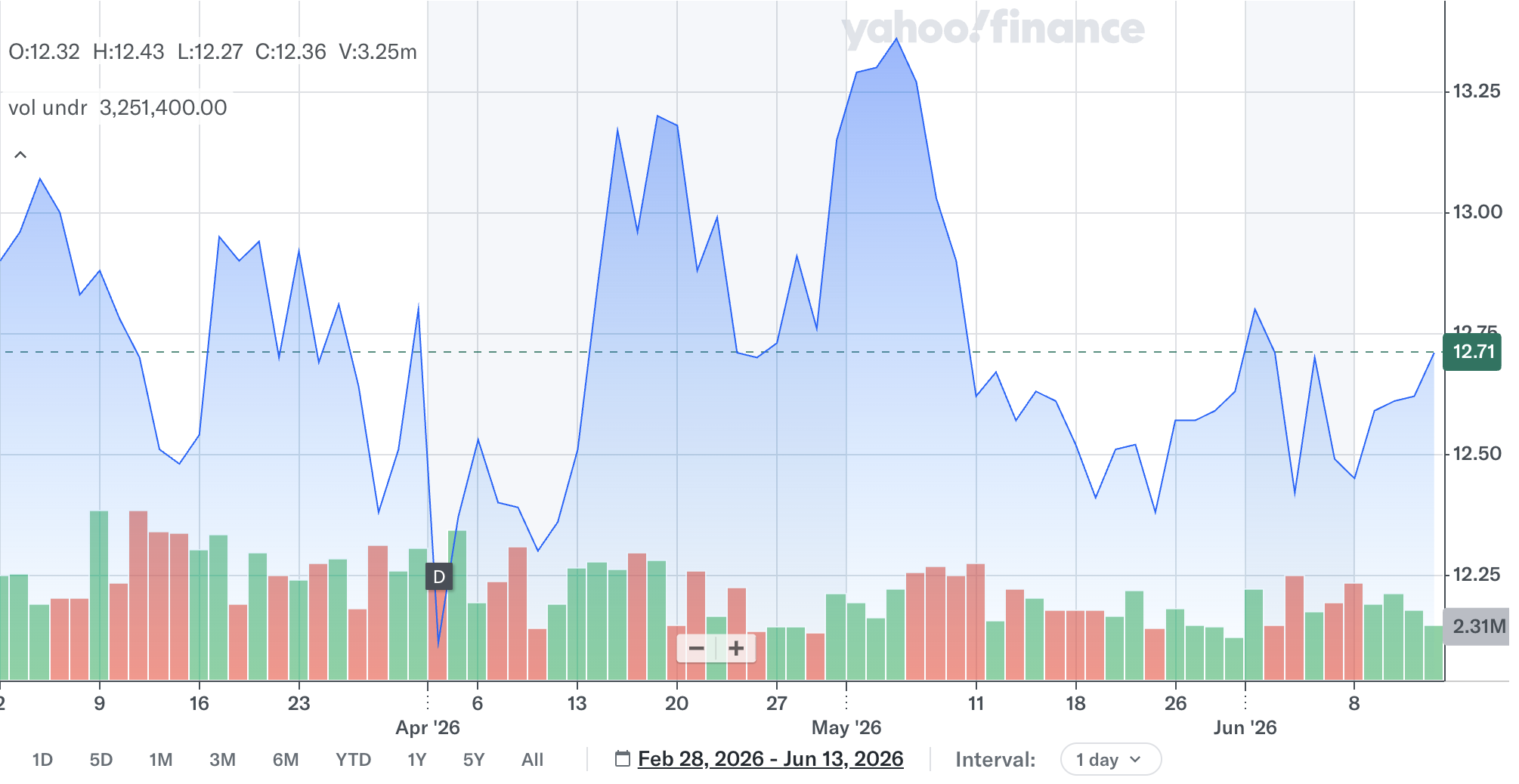

This week's potentially positive BIZD result notwithstanding, there is no upward trend to point to.

As this chart illustrates, the BDC ETF has been trading essentially flat since early March, with any uptick quickly followed by a downswing.

Glimmer

However, we should point out that for BDC investors able to stay long in all this price turmoil, the bottom-line performance is not so awful, thanks to BDC distributions received even as their prices tanked.

The S&P BDC Index on a total return calculation is down "only" (8.3%) in 2026 and is actually up 18% over a three-year period.

Of the 39 BDCs around since mid-2023, 25 are in the black when price change and dividends are factored in.

WHERE WE ARE HEADED

Unaltered

In the first two sections of these Recaps, we stick to reporting the facts as we've collected them.

When we come to the way forward, we have no choice but to reach for our crystal ball whose fortune telling capabilities are admittedly flawed.

With that reminder, we can say that the BDC Reporter remains pessimistic about the way ahead for BIZD and for most individual BDC prices.

There continues to be no catalyst we can see on the horizon that might ignite investor enthusiasm and lift prices for a sustained period.

Top Of The List

The biggest question remains what might happen to interest rates.

Appropriately enough, we have the first Warsh-helmed Fed meeting coming up this week.

We'd be very surprised if the new Chairman allowed an interest rate increase, even in the face of rampant inflation.

One gets the impression that the Chairman has promises to keep and is most likely to stand pat to retain some support in the White House while also avoiding the immediate destruction of his credibility with his more "hawkish" colleagues and the market.

Sometimes, making everyone a little unhappy is better than provoking strong feelings on one side or the other.

No change in the Fed Funds rate should keep BDC income flat, but the sector faces other challenges.

Expensive

As we've been reporting, medium-term rates in the unsecured debt market remain high, just as many, many BDCs are issuing new unsecured notes.

That expensive debt is mostly refinancing extremely inexpensive borrowings from the ZIRP era.

In many cases, this will erode BDC earnings for many quarters to come as the arbitrage involved between BDC lending and borrowing narrows.

If Only It Were So Easy

Some market observers hope that wider spreads on new loans, driven by current credit uncertainty around software loans, will be a boost for BDCs.

BDC conference calls in April were full of reports of new loans being booked on more lender-friendly terms.

However, we believe the "flight to quality" discussed in the briefing note above will prevent spreads from widening significantly.

Everyone is being more cautious - so they tell us - and will be bidding up for the "better" deals and avoiding adding exposure to the generous terms software borrowers will need to pay.

Market Update

Despite all the talk about redemptions of non-traded BDC capital, there's still a lot of capital swirling around in Private Credit. Here's what our research shows:

Key Dynamics in April–June 2026

The "Syndicated vs. Private" Tug-of-War: The biggest narrative of Q2 2026 is the pricing pressure on private credit. Because the BSL market has rebounded with tighter, more competitive spreads, upper-middle-market corporate borrowers are actively looking to "refinance out" of expensive private credit deals into cheaper syndicated bank facilities. To defend their portfolios, direct lenders in Q2 are being forced to slash pricing (often cutting yields or accepting lower original issue discounts).

Middle Market Resilience: In the core middle market—companies with EBITDA between $25 million and $75 million—private credit remains the absolute dominant technology for capital deployment (Ivashina, 2026). Net new deal flow here is steady but highly selective, as managers keep an eye on underlying portfolio companies facing prolonged high cash interest burdens.

Even if spreads on new loans widen from their anemic prior levels, that process will have to continue for several quarters to have a material impact on BDC profitability.

After all, BDC portfolios take, on average, 4 years to turn over.

Job 1

Finally, there's the credit question.

Our own research continues to suggest that overall BDC credit performance remains well within "normal" historical ranges for losses, defaults, and non-accruals.

Private Credit's "cracks" are not much more pronounced than they were 3, 6, or 9 months ago.

However, there continues to be a wide dispersion in credit performance amongst individual BDCs, so it's impossible to paint with a broad brush.

As they say, "your results will vary", depending on which BDCs one holds.

Don't Look Up

With that said, the sword of Damocles that hangs over all Private Credit is what the future holds for all those software loans on the books.

Here is some broad market data which shows that the key refinancing years are 2028-2029 - a lifetime away

Out of a total of roughly $657 billion in outstanding software/tech-related BSL and private credit-adjacent debt, approximately 46% is scheduled to mature within the next four years.

| Year | Expected Software Loan Maturities | Market Context & Narrative |

| 2026 | Minimal (< $10-15 billion) | A handful of minor facilities; a complete non-event for the broader credit market. |

| 2027 | ~$30 - $40 billion | The wall begins to build. Early 2021/2022 vintage LBOs reaching their 5-year marks. |

| 2028 | ~$130 - $150 billion | The Peak Crunch. Apollo and Goldman Sachs data show that 2028 holds the massive $40B+ single-year wall for pure-play BSL software issuers. |

| 2029 | ~$230 - $250 billion | The tail end of the massive 2021–2022 software buyout boom hits final maturity. |

| 2030+ | Remaining Balance | Recent 2024–2026 vintages, which are heavily scaled back in size and volume. |

Exceptional

We've been following the BDC market for over 25 years and cannot point to any prior period with a credit question mark against such a large portion of the loans held.

The closest equivalent was in 2014, when oil prices fell from $100 per barrel to $40-$50. Some BDCs had been active, adding all sorts of energy deals in the years running up to the price crash, and were caught flat-footed.

However, energy accounted for only 4%-7% of BDC investments overall and was less broadly-based than the current exposure to software.

The BDC sector came through that challenge without too many scrapes and bruises, but some individual BDCs did suffer losses they have never fully recovered from.

Worrying

We remain agnostic as to whether the software exposure is a disaster in the making or a non-event, but that's neither here nor there.

The market, in the form of lenders and the investors in those lenders, still seems wary, though.

We don't see that bugbear going away in 2026, and it is likely to weigh on BDC prices.

One day, the sun will come out, where the factors influencing BDC profitability are concerned, as they did very suddenly in 2009, 2011, 2020, and 2022.