Blue Owl Capital: Issues $400mn In New Unsecured Notes

Underwhelming

NEWS

ANALYSIS

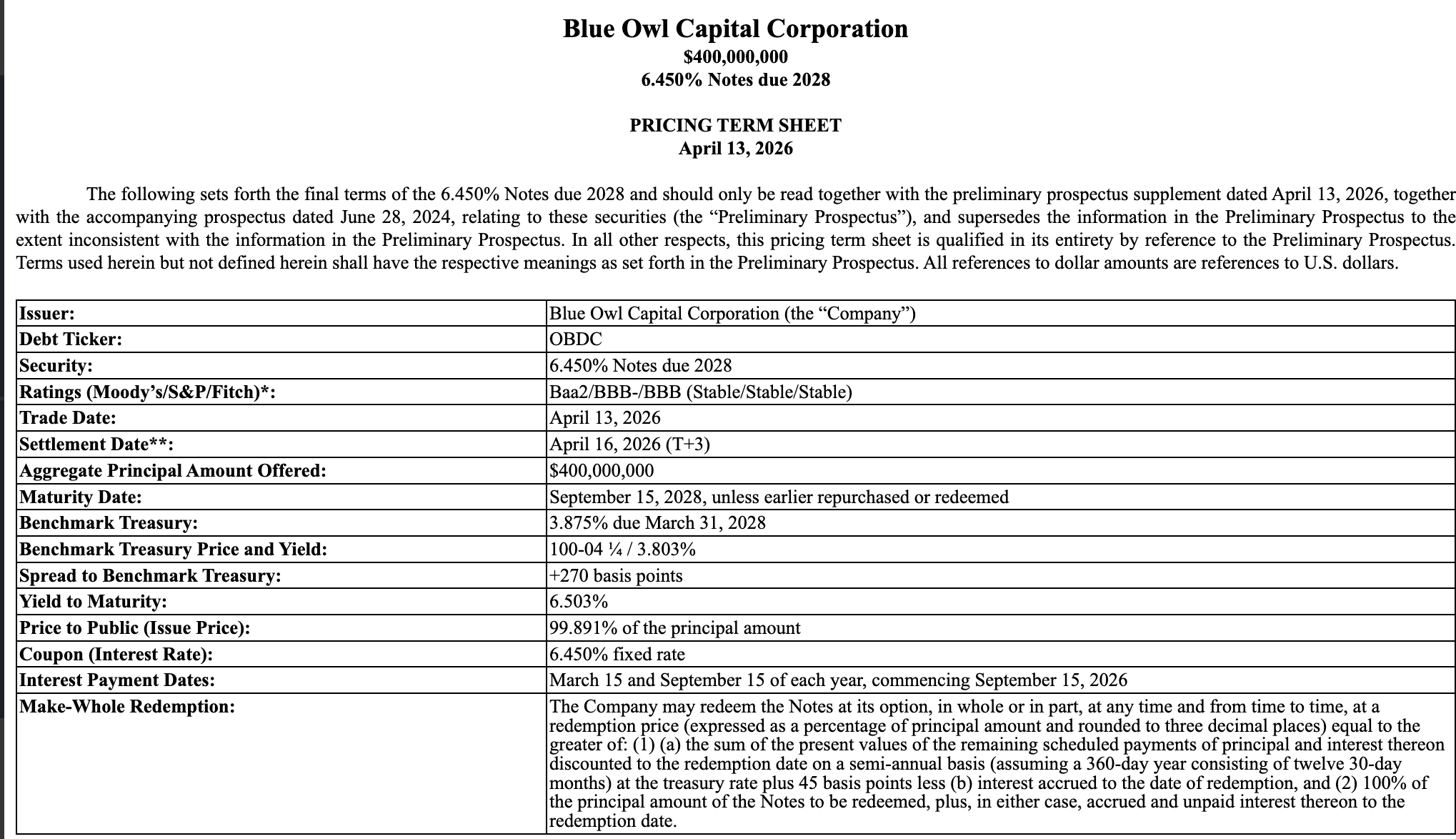

We were curious to see how Blue Owl (OBDC) might structure and price its latest unsecured note. See the Term Sheet above.

Apparently, so was Bloomberg, which wrote an article on the subject on April 13, 2026, which was picked up and summarized by Seeking Alpha.

The most interesting insight from Bloomberg was the following:

The OBDC bond sale priced at a roughly 2.7 percentage point spread to similar-maturity Treasuries, according to the filing. US BDC spreads have widened in recent weeks, climbing to about 2.25 percentage points above their benchmark, from 1.7 in January, according to data compiled by Bloomberg. That compares with an average yield gap of about 0.8 percentage point for US high-grade bonds.

We have not seen Bloomberg’s data, so we cannot confirm their contention that BDCs are paying more of late than earlier in the year.

Anyway, new issues are episodic, extend over different maturities, and involve BDCs of varying sizes, which makes drawing conclusions about spreads “widening” problematic.

Our Thoughts

The BDC Reporter has a couple of insights of its own.

First, we were surprised by the unusual length of the notes.

They traded as of April 13, 2026, and are maturing on September 15, 2028.

That’s a 29-month period.

Typically, these unsecured notes are issued for 5 years and, more recently, for 3 years.

This is a strange tenure and makes the comparison with the risk-free rate, which is the two-year Treasury coming due March 31, 2028, imperfect.

Squeezed

As we’ve noted in earlier articles, the spread between what a BDC can earn on new loans and its borrowing cost is narrowing.

In this case, OBDC reported in the IVQ 2025 that new loans were being booked at a 4.8% spread over SOFR.

The latter is currently running at 3.6%, so the all-in yield is 8.4%.

OBDC – as we’ve seen – will be paying 6.5% on this new note.

(By the way, that’s substantially more than the $500mn in notes recently paid off, which had a yield of 4.25%.)

Then there’s the 1.50% Management Fee (but only 1.00% when leverage exceeds 1:1) and the 17.5% Incentive Fee.

Using the most conservative numbers and assuming all acquired assets are yield-bearing, a shareholder should net only about 0.3% on investments funded by this latest debt.

If OBDC had borrowed for 5 years, the return would likely have been negative.

These sorts of numbers make one question whether using leverage under current conditions makes sense from a shareholder’s standpoint, especially as those thin returns are likely, statistically speaking, to be further eroded by credit losses over time.

Of course, the external manager benefits from maintaining this leverage, but does the OBDC investor?

Not Done Yet

OBDC, like many BDCs, is facing the need to gradually replace very inexpensive, unsecured debt issued during the ZIRP era with much more expensive unsecured notes.

In addition to this latest issue, there are 4 more notes on the books that will need to be repaid between now and 2028, with an aggregate cost of $2.7bn.

Unfortunately for OBDC and its shareholders, that means the arbitrage between what the BDC earns and what it pays to borrow is likely to narrow.

Here are the numbers as of the end of 2025:

In the fourth quarter of 2025, the weighted average total yield of OBDC’s portfolio was 9.5% at both fair value and amortized cost. When looking specifically at accruing debt and income-producing securities, the weighted average yield was 10.0% at fair value and 10.1% at amortized cost. Regarding the cost of borrowing, OBDC reported that its weighted average total cost of debt was 6.0% as of December 31, 2025. Additionally, the company’s average interest rate on its borrowings was 5.6% for the year ended December 31, 2025

VIEWS

The most important issue is not whether OBDC paid a few more basis points than they might have otherwise, were it not for the recent bad publicity at the parent.

Much more important – and more likely to weigh on earnings in the next couple of years than any credit losses on software loans – is this drawn-out process of replacing dirt-cheap BDC ZIRP-era borrowings with debt at market rates.

For OBDC at least – and every BDC is different – this process will serve as a significant brake on profitability.

Unfortunately, the macro conditions are not currently favorable, with loan spreads thin and the cost of borrowing unsecured relatively high.