Investcorp Credit Management BDC: Hires A Financial Advisor

Too Late?

NEWS

NEW YORK—April 20, 2026 — Investcorp Credit Management BDC, Inc. (NASDAQ: ICMB) (“ICMB” or the “Company”) today announced that it has engaged Houlihan Lokey, a leading independent investment bank, as its financial advisor to assist the Special Committee of Independent Directors in its ongoing review of strategic alternatives. As previously announced, the Special Committee is evaluating a broad range of strategic, financial and business configuration options for the Company. ICMB has not set a timetable for the conclusion of its review and has not made any decisions at this time. There can be no assurance that the review will result in the completion of any specific transaction or outcome. The Company does not intend to comment further with respect to this review unless or until its Board of Directors has approved a definitive course of action, the review process has concluded, or it is determined that other disclosure is appropriate.

AGENDA

We are going to review the BDC’s most recent financials to determine what earnings and asset value might look like going forward – a critical factor in any “strategic alternative”. Also, we’ll speculate about the different alternatives available to ICMB’s Board.

ANALYSIS

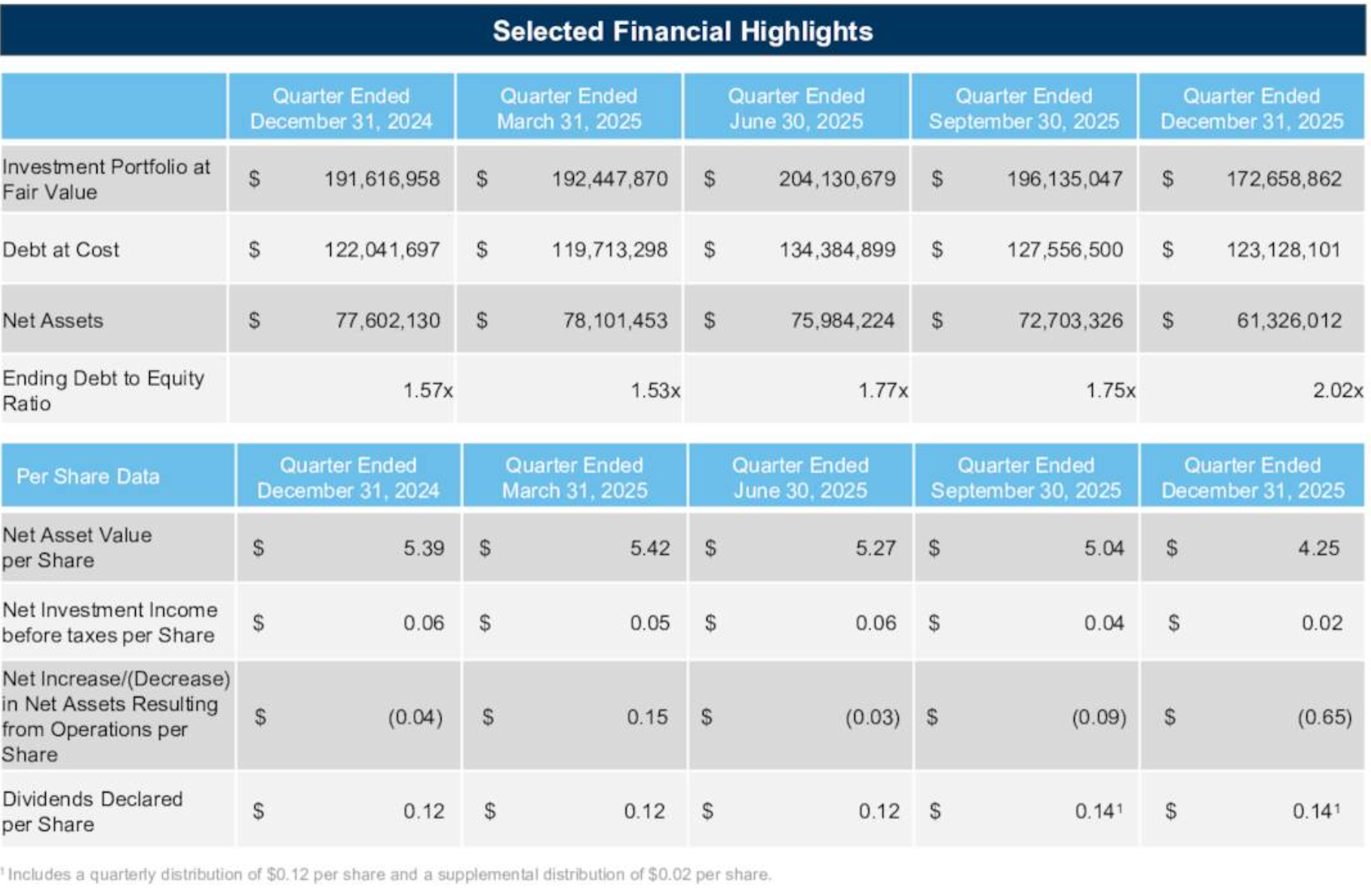

ICMB’s portfolio value, net asset value, earnings, and dividends have all been shrinking quarter-over-quarter over the past year.

On The Brink

Most problematically of all for a regulated BDC, leverage levels are exceeding the maximum allowed. \ According to what was said on ICMB’s conference call, the critical asset coverage ratio of debt was 150% at year-end 2025, right at the regulatory limit. Admittedly, since then, asset coverage has improved slightly to 155% as a further $14mn of debt has been paid down. Some of that pay-down must have come from investment repayments, further shrinking the portfolio.

Under Pressure

A key challenge ICMB faces in the short run is that further devaluations of its net assets, driven by credit challenges, will require additional debt paydowns to remain within BDC rules. Unfortunately, it’s very likely that the BDC will continue to experience unrealized depreciation in its portfolio. In 2025, these losses totaled ($8.9mn), several times the BDC’s earnings for the period. With 9% of the portfolio at cost non-performing – up from 8.0% previously – the odds are high that the portfolio will be shrinking in the near future.

Back Of The Envelope

That’s likely to leave the Board of the BDC with even less than the $173mn in portfolio assets on the books at year-end at FMV. Moreover, a large proportion of the assets will be highly problematic to sell. Let’s deduct the ($12mn) of non-accruals and the $33mn of equity investments. For our purposes, let’s also assume $15mn of investments have been repaid or sold since year-end at close to full value. On a pro forma basis, that suggests ICMB has only $105mn of decent-quality loans available to sell.

Even that number is likely overstated because there are several companies that might be paying interest but are underperforming. Specifically, we are thinking of recently restructured American Nuts and Crafty Apes, with a total FMV of about $6mn in debt. That brings the FMV of credible portfolio loans that could be sold just under $100mn. Against this shrinking pool of decent assets, ICMB had $110mn in borrowings outstanding at the end of February, following the repayment of the $14mn flagged above.

Loss Making

A portfolio of this size can’t hope to be profitable. As of IVQ 2025, ICMB was earning only $0.3mn in Net Investment Income. Since then, the external manager has come to the BDC’s rescue and arranged a refinancing of its only unsecured debt of $65.0mn. That’s a positive for the BDC and the shareholders, avoiding a potential bankruptcy. However, the prior debt was being charged at 4.875%. The new debt, guaranteed by Investcorp, is based on SOFR and has an all-in yield of about 9.25%. On an annual basis, that will cost ICMB about ($2.8mn) more in interest expense than before. Then there’s the one-time fee charged ICMB for the new debt of $0.650mn.

Best Option?

We imagine that the Board of Directors would ideally like to identify a buyer for the entire portfolio. On paper, at year’s end, the net asset value was $61mn. Currently, in the wake of the news about hiring Houlihan Lokey, the market values that NAV at $27mn, or $1.89 a share, as we write this. Based on the above, even the market’s latest estimate of the BDC’s book value seems optimistic. Chances seem high that shareholders will receive nothing, and we wonder if some of the unsecured debt might end up getting a haircut.

Known Unknown

Much will depend on what value any buyer places on the $48mn in equity investments, which are already valued at only $33mn. There are 13 different companies involved. Of those investments, only 3 are materially outperforming their cost: Bioplan USA, Discovery Behavioral Health (a preferred stock position), and the aforementioned Crafty Apes equity. These 3 positions have an aggregate value of $18mn. However, both Bioplan and Crafty Apes have seen their equity values drop somewhat in the most recent quarter. Only Discovery has increased, from an FMV of $6mn to the current $7mn.

Timing

The problem – as always – with valuing these equity stakes – is that the holders have little or no control over the timing of any exit. ICMB’s 10K shows that in 2023 and 2024, no proceeds were received from “sales and repayments” of equity stakes, and $6.5mn in 2025. How much would a would-be buyer be willing to pay for $33mn of equity with an unknown liquidity timetable? That is the question the investment bank will be attempting to answer, along with the value of the debt positions.

Unlikely

On paper, another option ICMB might have is not to sell the portfolio but to let the investments run off over time. Proceeds would initially be used to pay off the secured Revolver, followed by the unsecured notes, and ultimately, the net proceeds would go to shareholders. In this case, though, this seems unlikely. With the existing portfolio generating only 7.7% yield, ICMB would likely be a money loser, even if the manager waived some or all of its fees. The cost of borrowing under the Rebolver is running at 8.0%, and – as we’ve seen – the new unsecured notes are even more expensive. In all likelihood, by the time the lenders were repaid from investment proceeds, there would be nothing left for the shareholders.

VIEWS

These rather dark prognostications are just estimates based on what we can find in the public record.

Maybe we are being too pessimistic, and one or more buyers may see more value than we can ascertain.

We’ll find out once Houlihan has polled potential purchasers.

As we’ve seen, the portfolio’s economics suggest that some sort of resolution is required to avoid making an already difficult question worse.

What is clear – in our opinion – is that Investcorp has done no one any favors by waiting this long to pull the alarm bell and ask for outside help.

One can only wonder why the 3 independent directors now entrusted with protecting shareholder interests took so long to get involved.

We do note – without comment – that the independent directors owned between them 45,000 shares in ICMB – one third of 1% of the shares outstanding.

Bigger Picture

If ICMB – and its remaining equity – sinks below the waves – as seems likely – it will be another black eye for the BDC sector and not at a good time for the sector.

Even more worrying will be if several other underperforming BDCs follow a similar path.

We don’t want to be alarmist, but anyone keeping an eye on our BDC NAV Change Table will know that there are 8 BDCs whose NAVPs have dropped by (30%) or more in the last 5 years.

ICMB is amongst them, down (46%) -, but there are others who have fared even worse…

Some of those ailing public BDCs are much, much larger than ICMB, and should they stumble, the impact on shareholders, the market, and the sector’s reputation could be far worse.

That’s one more reason to keep an eye on how the managers of these walking wounded address their challenges during the coming BDC earnings season- and in future quarters.

Will they contend that there is nothing wrong or take remedial actions to ensure that their investors won’t wake up one morning to hear that the Board has hired an outside adviser to fix what they did not?