BDC Common Stocks Market Recap: Week Ended January 9, 2026

Behind Already

BDC COMMON STOCKS

Week 2

Wall Street closed out the first full trading week of the new year at record levels on Friday, with the benchmark S&P 500 index (SP500) ending about 34 points shy of the historic 7,000 mark. A revival in the tech trade, coupled with mixed labor market economic data, boosted sentiment and offset geopolitical escalation between the U.S. and Venezuela.

For the week, the S&P (SP500) added +1.6%, while the tech-heavy Nasdaq Composite (COMP:IND) advanced +1.9%. The blue-chip Dow (DJI) climbed +2.3%.

Seeking alpha – wall street breakfast – january 10, 2026

Good Enough

BDC sector prices in the first full week of the year – but Week 2 by our way of counting – could not keep up with the major indices.

The only BDC exchange-traded fund – Van Eck’s BIZD – moved up 0.5%. The S&P BDC Index on a price-only basis performed only a little better: 0.55%.

Intra-week, BIZD – and BDC prices generally – were moving up and down with abandon.

We were so rattled that we took to our X page to comment on Wednesday, January 7:

BDC Prices Slumping: Going by the price action of the BDC sector’s only ETF – Van Eck’s $BIZD – In the last two trading days, prices – after a mini new year surge – have headed south. $BIZD has dropped by (4.0%) since peaking at $14.54 intra-day on Monday, January 5, closing a few minutes ago at $13.97. That’s below the 2025 year-end of $14.18. This is reminiscent of July 2025, when BDC prices fell across the board. 3 months later, BIZD was down (20%) into Bear territory. We’re already a fifth of the way to a repeat in 2 days…Why is this happening? Maybe it’s positioning ahead of earnings season, or investors believe Trump and Miran are going to cut short-term rates a lot more than the Fed has been indicating.

However, on Thursday, we were back with these words:

The Wonderful Wacky World Of Public BDC Prices: Just hours after we noted that the BDC ETF $BIZD had been seriously slumping for 2 days, and almost every individual BDC was in the red, prices have surged upwards. $BIZD is up 3.0% 4 hours into the trading day, even as Trump Administration fellow traveller and Federal Reserve gadfly Stephen Miran calls for a 150 bps rate reduction. Confusing, to say the least.

Thankfully, Friday was relatively quiet, and so were we.

Mostly

Looking at the prices of individual BDCs after a week, there was plenty of forward motion.

32 of the 46 BDCs we track were up or flat price-wise

4 BDCs increased by 3.0% or more in price right out of the gate.

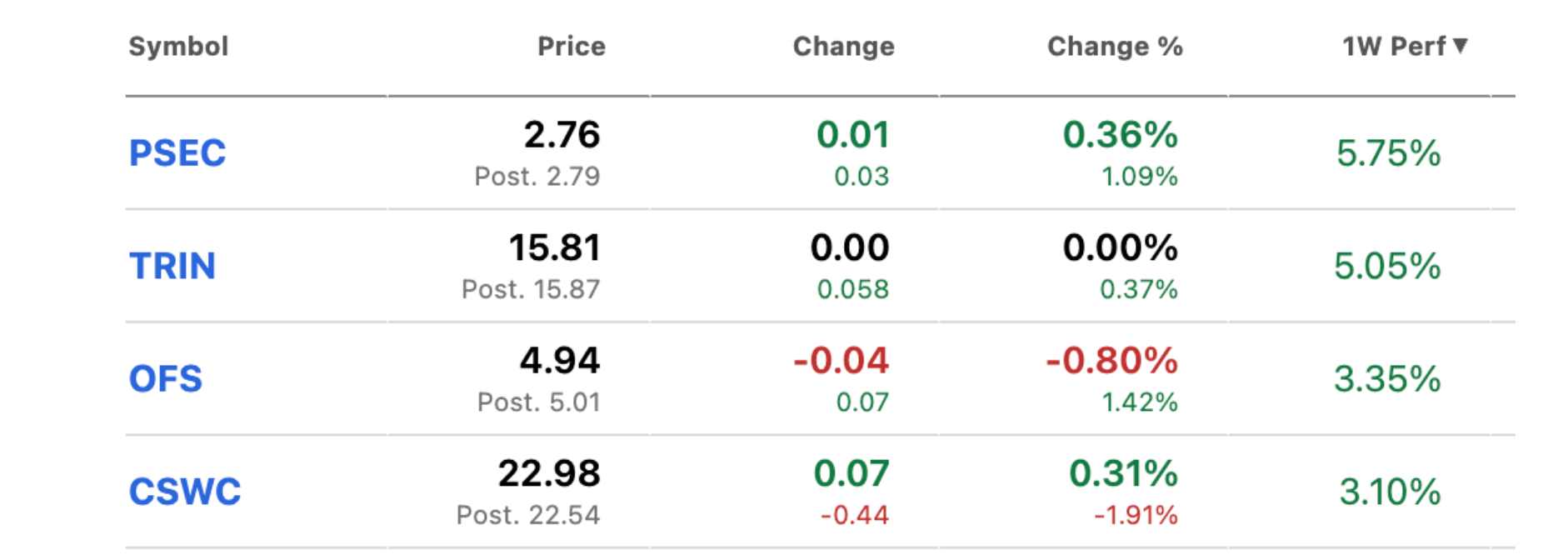

A Bit Of Both

As the table shows, there are two perennial underperformers on this list – PSEC and OFS – whose stock price trades at a deep discount to book, and two investor favorites – TRIN and CSWC – whose price is well above book.

In a way, this reflects the two main categories of investors in BDCs: one group looking for undervalued names that might be on the rebound trail and could generate a quick capital gain, and the other looking for stocks to have and hold for steady, predictable returns.

Coincidentally or otherwise, TRIN and CSWC are part of a select group of BDCs that we project will maintain their 2025 payout level into 2026.

BTW, no BDC dropped more than (3.0%) in price. FS-KKR Capital (FSK) was the worst price performer, (2.4%) down in price.

Pick Up

In another sign of a decent start to 2026, the number of BDCs trading at or above their Net Asset Value Per Share (NAVPS) increased to 9 from 7.

Yet Again

As far as we can tell, only one BDC dropped to a new 52-week low: Goldman Sachs BDC (GSBD).

The WSJ had some not-so-nice things to say about GSBD in a full-fledged article on December 25, 2025. If you’re a WSJ subscriber, click here for the link.

Maybe the bad press has something to do with the continuing decline in GSBD’s price.

However, as is often the case, when the financial press notices a problem, it’s much too late.

GSBD’s NAVPS began to deteriorate in the IIIQ 2021 (see the BDC NAV Change Table), and its stock price reacted in the spring of 2022. See below:

Currently, GSBD’s price-to-expected-2026-earnings ratio is 7.0x, well below the BDC average – as we calculate it – of 9.2x.

How long until GSBD begins to attract the “value buyers” circling PSEC and OFS?

WHERE WE ARE

Keeping It Short

Of course, after 5 trading days, there’s not much to add that has not already been covered above.

2026 is just getting underway, and the BDC IVQ 2025 earnings season is still a few weeks away.

From The Headlines

However, we did hear from Saratoga Investment (SAR) this week, whose fourth quarter ends in November.

We did write two articles about SAR – one was a response to a frequently asked question: Will the BDC be able to maintain its current dividend despite consistently earning less than its payout? Inquiring minds – and all its shareholders – would like to know.

In a second article, we offered up some questions that we would have liked the analysts to ask on the SAR conference call, but didn’t.

However, we didn’t write any straightforward review of the BDC’s latest financial results and credit performance, both of which we assess for the BDC Reporter and the BDC Credit Reporter, and hand out ratings for.

Here’s a summary of both:

Financial Performance: Despite lower interest rates, a decreasing portfolio yield, and an increased number of shares, SAR managed to boost its recurring income per share compared to the prior period. This reflected both a once-again growing portfolio, gains from repayments, and decreasing debt service expenses. Plus, the BDC booked some decent realized gains. If it weren’t for the higher dividend level, NAVPS would have increased but ended up an immaterial ($0.02) per share lower. All in all, SAR performed above our expectations, garnering a rating of 1 on our 5-point scale.

Credit Performance: Both the number and value of underperforming and non-performing companies remained very, very low. According to SAR itself, only 0.2% of the 87.2% of its assets that they rate are performing poorly. There is only one company – out of 46 – involved: Pepper Palace – the only non-accrual on the books. There were no new Watch List or non-performers added in the period, and improvements were noted in the ones that were present in the prior quarter. There remains softness in the performance of SAR’s own CLO , which is being wound up, and its senior loan joint venture – but the impact is not material. All in all, the BDC Credit Reporter continues to rate SAR’s long-term credit performance a 1 out of 5 – exceeding our expectations.

For the full review, see the BDC Credit Reporter. A subscription is only $50 a month.

Other News

There were several other BDC news stories during the week that deserved mention but the market took in stride.

Ares Capital (ARCC) issued new 5-year unsecured notes with a yield of 5.25%, a tight 200 basis points over the risk-free rate.

Still, the BDC has to contend for a little longer with multiple blocks of debt added during the ZIRP era that must be refinanced at higher costs.

It’s a sector-wide problem, but most of the super-cheap debt will be gone by the end of 2026.

Different Approaches

Several BDCs announced distributions for 2026. PennantPark Investment (PNNT) and PennantPark Floating (PFLT) are sticking with the same monthly dividend as before, but CION Investment (CION) cut its “regular” monthly dividend from $0.12 to $0.10 per share.

We expect many more CIONs than Pennant Parks this year, as the pressure of lower rates/spreads causes elevated dividends added in the BDC Golden Years to be reduced.

The market has already braced itself, as reflected in the huge BDC price drop last summer.

CION’s dividend may have been reduced by (17%), but its stock price was down only (1%) this week.

For the record, CION’s current PE ratio is 7.3x and its yield 12.4%.

Just In Time

Elsewhere, OFS found the liquidity needed to redeem the final $16mn of its unsecured note, which comes due next month.

We don’t know where the proceeds came from – there was no new Baby Bond or other unsecured note issued – but we did hear this week that the BDC’s revolver with Banc of California (why a c and not a k ?) was extended for 2 years.

According to the BDC’s latest 10-Q, Banc of California has committed $25.0mn, with nothing drawn as of September 30, 2025.

This extension is important because the BDC’s other revolver with BNP Paribas was not extended and is being wound down, with all loans held in the facility as collateral being used to repay outstandings when they come due.

OFS – this week’s jump in its stock price notwithstanding – is not out of the liquidity woods as yet.

For more on OFS, check out the multiple articles available in the BDC Reporter’s archives.

Investor Relations Department Kept Busy

Finally, both Main Street Capital (MAIN) and its “mini-me,” MSC Income Fund (MSIF) disclosed both a realized equity gain from a jointly owned portfolio company and the latest status of their “Private Loan Portfolio ” activity.

These partial disclosures of news can be misleading – for all we know, both BDCs have also booked big realized losses as well that have not found their way into a press release.

Still, if we take what we read at face value, both MAIN and MSIF will have positive news to report when we get the actual IVQ 2025 results in a few weeks.

WHERE WE ARE GOING

Sweet To Sour

Looking at the macro environment going into the new year, we were in a positive frame of mind about the outlook for BDC stock prices in 2026.

With short-term interest rates seemingly very close to the neutral rate and the Fed projecting only one rate cut in 2026, some stability seemed to be headed our way after two years.

SOFR, the key ingredient to both BDC loans and borrowings, has dropped from 5.3% to 3.7%.

If we were “done” at a SOFR rate of 3.5% or so, BDC earnings would have a chance to stabilize.

That, in turn, could cause investors to return to the fold after last year’s major exit.

Wrong?

However, this week we heard – once again – that Fed Reserve Governor Stephen Miran is looking for 150 basis points of rate cuts in 2026, and that theme was taken up – also once again – by U.S. Secretary Bessent, albeit without a specific reduction mentioned.

The President – jokingly? – warned he might fire Bessent if the Fed didn’t cut rates this year.

We know that the markets are not expecting a rate cut in January, and something far less than Miran/Bessent/Trump in all of 2026.

Far From Impossible

Yet, who can say with assurance that this Administration – whose self-confidence is at an all-time high – will not get its way?

And soon. For rate cuts to have the desired political effect on voters’ state of mind at the time of the midterms in November, they must happen ASAP.

This week, we saw the President willing to take his battles to the business establishment on a variety of issues (credit cards, weapons manufacturers, etc) and causing Fannie/Freddie to buy up mortgage-backed securities to lower our mortgage costs.

We have no opinion on whether lower rates are a Good Thing or a Bad Thing in the U.S.

Our only concern here is what the impact might be on BDC prices if the Administration gets its way and rates are sharply reduced over a short period.

Based on what we’ve heard from the BDCs themselves, their planning is informed by market expectations for the rate curve. The same also seems to be true for BDC investors.

If we get a much more substantial downward shift, chances are high – but never 100% – that BDC prices will take another leg down to re-set to the expected new level – i.e., SOFR between 2.25% – 2.75%.

We Too Are Fair And Balanced

BDCs will benefit from much lower rates.

Pressure on debt service numbers at leveraged borrowers will ease, reducing default and bankruptcy risks. Also, the private equity market should pick up steam after years in the doldrums, generating plenty of business for leveraged lenders. Portfolio companies – boosted by having more money to spend – could be in even better shape than they are currently. All the recent angst about “cracks” appearing in lending could be replaced with a much more sanguine approach from markets.

Most Likely

However, investors – if prior performance is any guide – are likely to sell first and only circle back later should interest-rate expectations change drastically.

After all, the likely result will be lower BDC earnings and lower distributions than cu rrently countenanced.

Staying Calm And Carrying On

In the long run – under any scenario – we believe BDCs provide superior value compared with other income-producing investments tied to interest rates and that will eventually be reflected in their stock price.

Worrisome

In the short to medium term, though, the huge uncertainty coming out of Washington is sending chills down our spine.

Every year has its dramas, and where rates go – or don’t go – seems to be lining up to be the key macro variant of the year – much more impactful than credit, spreads, investment activity, or any of the other factors that go into BDC profitability.

We will be here every weekend to discuss the latest developments, so please tune in.

You’ll also find us commenting regularly on the BDC Publications X site during the week, so please “follow” us there as well.