BDC Common Stocks Market Recap: Week Ended March 13, 2026

Gloom

BDC Common Stocks

Week 11

Wall Street closed the week lower as investors digested fresh inflation data, ongoing energy market volatility, and developments surrounding Federal Reserve Chair Jerome Powell. The S&P 500 lost 1.6%, the Nasdaq Composite dipped 1.3%, and the Dow fell 2.0% for the week.Seeking Alpha - Wall Street Breakfast - March 14, 2026

Misery

Another difficult week for anybody invested in the BDC common stock sector.

BIZD - the Van Eck exchange-traded fund, which serves as one of our guideposts to sector price performance, slumped by (2.7%).

Our other price guide - the S&P BDC Index - fell (3.1%) just in price terms.

Almost all individual BDCs were in the red this week - 42 out of 46.

Moreover, the downward pull on prices was very strong, with 25 BDCs falling (3.0%) or more.

6 BDCs fell (6%) or more, and of those, 5 fell by double-digit percentages.

The percentage price changes in the most extreme of these cases are so drastic that one can’t help but feel that investors are “capitulating”.

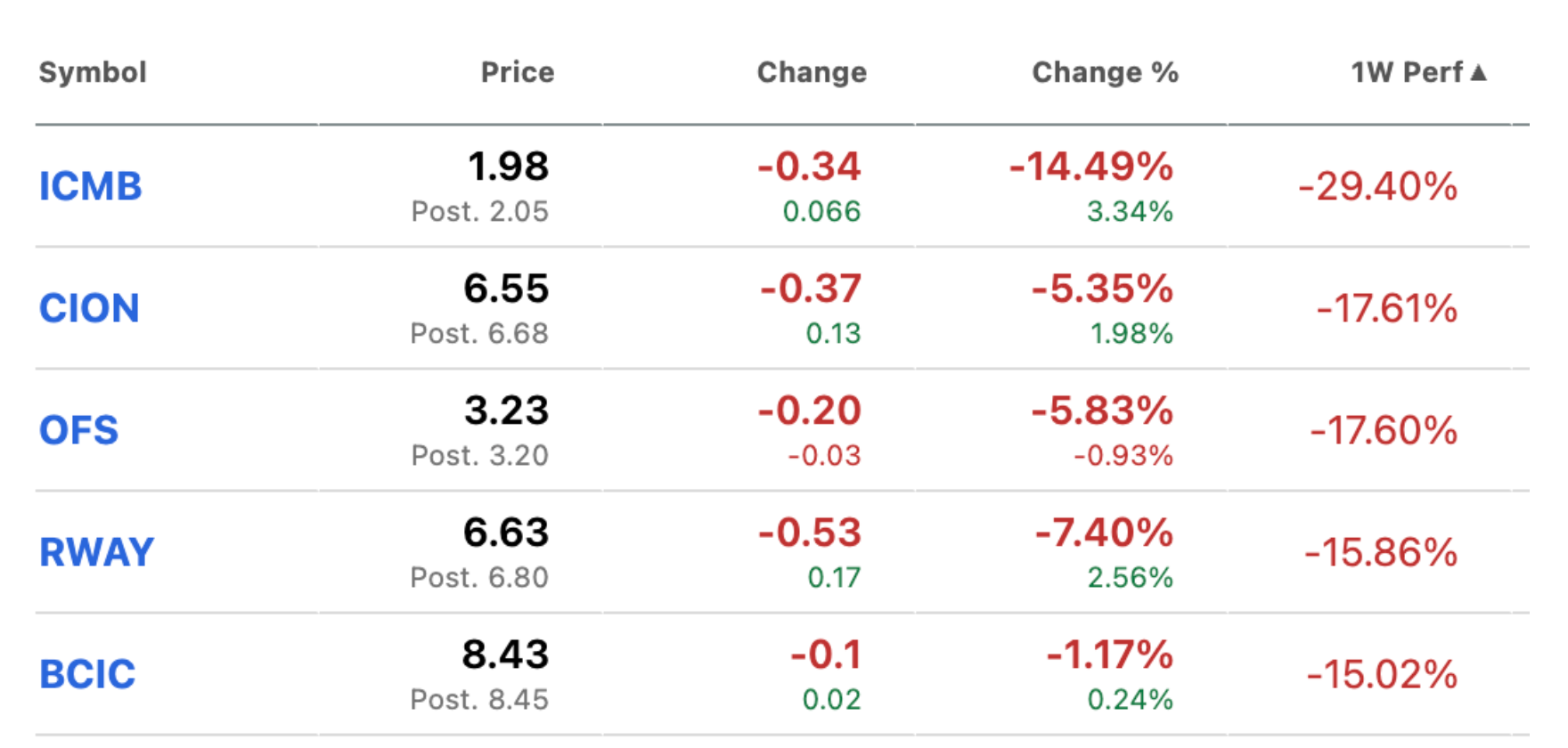

Here are the worst of the worst performers drawn from Seeking Alpha’s excellent records:

Makes Sense

The severe downdraft is not wholly unreasonable.

Most of these BDCs posted weak IVQ 2025 results, as you can see from checking out the BDC Performance Table, where we review each BDC's results.

CION Investment (CION) - for example - saw its Net Asset Value Per Share (NAVPS) fall (7.4%) in just 3 months.

Management would likely argue that much of the decline was due to equity stakes falling in value rather than because of credit problems, but no one is listening at this point.

Also, CION’s dividend was cut from $0.36 to $0.30 per share, albeit going forward, shareholders will receive their distributions monthly.

OFS Capital’s (OFS) NAVPS result was even worse. The metric was down (9.6%).

Runway Finance (RWAY), which is habitually a pretty good performer - slipped up in the IVQ 2025 and was punished.

The problem here was less about lower asset quality - NAVPS only fell by (1.0%), roughly within what one should expect for a BDC on average - but profitability.

Net Investment Income (NII): NII fell to $11.6 million in Q4 2025, a decrease from $15.7 million in Q3 2025.

NII Per Share: NII per share generated was $0.32 in the IVQ 2025, a ($0.11) per share decrease from the $0.43 per share generated in Q3 2025. That’s a (26%) reduction.

BCP Investment (BCIC) - the former Portman Ridge Finance - saw its NAVPS drop (5%), but there were other setbacks as well.

Not to re-invent the wheel, this is what we wrote in the Individual BDC Performance Table, where we summarize quarterly results:

During the fourth quarter of 2025, BCP Investment Corporation experienced a challenging period marked by broad declines across key financial metrics when compared to the prior quarter. BCIC saw its total portfolio value contract at both cost and fair value, accompanied by a noticeable drop in its weighted average yield. This contraction led to sequential declines in total investment income, net investment income, and core net investment income on both an absolute and per-share basis. The quarter was further impacted by significant net realized and unrealized losses, driving a (5%) reduction in net asset value per share. Credit quality also deteriorated, evidenced by an increase in the number of non-accrual borrowers, a rise in non-accruals as a percentage of the portfolio's cost and fair value, and an uptick in assets internally rated as underperforming. All this drew the lowest quarterly rating: a 5.

Poor old Investcorp Credit Management (ICMB) - the worst performer in percentage terms - has not even had the opportunity to present its IVQ 2025 results, but investors fled anyway.

Almost There

When we hear from ICMB IVQ 2025, the earnings season will be over, and the BDC Reporter will have a mountain of data to summarize for our readers.

We won’t be spoiling anything by stating the obvious: this turned out to be a very mediocre quarter overall, where BDC’s book values were concerned, despite a great deal of stock repurchases going on.

We can safely say the last quarter was the worst one of the year by many metrics.

However, let’s not be too grim.

9 BDCs managed to increase their NAVPS in the period, and another 5 were down in a range between 0% and (0.5%).

There’s a wide dispersion in BDC performance, and that’s showing in price performance as well.

6 BDCs are still trading at a premium to book, while others are trading at discounts of up to (65%).

WHERE WE ARE

Record Breaking

We’ve been tracking the BDC sector for over twenty years, and, conceding that our memory may be faulty, we can’t remember such a dreadful beginning to a new year since 2007.

That’s a troubling parallel because that was the beginning of the GFC, and BDC prices did not stop tumbling - with brief pauses to breathe along the way - till March 2009.

By no means are we suggesting - as so many others already are - that the markets are about to repeat those darkest of days.

Every crisis is different and plays out on its own timescale and intensity.

However, what happened in 2007-2009 is useful as a reminder that stocks generally - and BDCs are no exception - can go very, very low before investors pull themselves together.

Market leader then and now - Ares Capital (ARCC) - began 2007 with a stock price of $18.84, only to bottom out 26 months later at $3.12.

Yet ARCC continued to pay a quarterly dividend throughout.

At the bottom, the annualized yield was 54%.

This week, ARCC reached a new 52-week low of $17.59. Its annual yield is 10.9%.

Correcting

Anyway, at this point, BIZD is down (12.0%) on the year, and (29.7%) below its 52-week high and slightly more than that compared to the full-year high in February 2025.

44 of the 46 BDCs we track are down in price YTD.

14 BDCs are down by (20%) or more.

The few BDCs trading at reasonable prices are almost all those that fell sharply previously due to poor performance (such as Prospect Capital) and are seen as too cheap to ignore.

One And Only

The only BDC that can boast both good financial performance and a decent stock price is Gladstone Investment (GAIN).

The BDC is a world away from AI fears; it pays a consistent dividend, and investors may be hoping for some equity gains to sweeten the pot in 2026.

GAIN is up 0.4% in 2026.

WHERE WE ARE HEADED

Bad Mood

As we’ve noted, recent BDC financial performance has been weak, and dividends are being cut left and right.

However, the recent drastic downward price moves are much more about what the forward-thinking markets anticipate might be coming shortly.

Some of that is undeniable. In the IQ 2026, all the BDCs will be impacted to varying degrees by the full impact of those multiple rate cuts the Fed made late in 2025.

That will likely shave several cents per share from most BDCs' earnings next quarter.

Also coming down the pike are the March 31, 2026, revaluations of BDC portfolios.

While secondary loan prices are holding up surprisingly well for most categories, all those Software borrowers the market is worried about may get re-valued downward.

Loan valuations are a black art, and methodologies vary between BDCs, but we’ll likely see another slump in NAVPS - especially amongst the high and mighty players that receive most of the attention.

Also, the first quarter of any year tends to be the slowest in terms of new business activity, and the recent turmoil may further lower new investment.

However, those concerns are modest compared to what some investors are contemplating for the medium term.

20% of BDC loans go to software companies, and many market participants continue to believe that many borrowers will face shrinking sales or even liquidation down the road due to AI competition.

Of course, that won’t happen overnight, so the markets will be anxiously watching companies' performance and whether loans coming up to maturity will be successfully refinanced.

However, with most Software loans not due to be repaid till 2028, we’ve got a long wait ahead, and every wayward move by an individual Software borrower - and there are over 1,000 of them - will be scrutinized for what they are telling us about the sector as a whole.

This could be excruciatingly painful and long-winded.

Not helping are moves like that made by JP Morgan this week, reducing advance rates to certain Private Credit borrowers on the software loans they post as collateral for their secured bank financings.

The “Software Is Doomed” fever could eventually break, but determining when, if at all, is impossible to tell.

The BDC Reporter and the BDC Credit Reporter will be keeping a close eye on the subject, but we’re digging in for the long haul.

Heaven Forbid

Then there’s always the possibility that all those naysayers turn out to be right. (We don’t think so, but what do we know?).

In the worst-case scenario that groups like UBS have posited, many of the larger BDCs - i.e., most of the market in dollar terms - could be hit with huge losses.

We’ll define “huge” as reductions in their NAVPS from this threat alone of (15-20%), and earnings could drop by a third or more.

As we’ve said, we don’t expect that to happen. Still, you can see how investors on the sidelines, or considering heading there, might tell themselves that a 12%-20% current yield from a BDC might not be sufficiently attractive to take on that sort of value-busting risk.

One More

Then there’s the broader uncertainty that the war with Iran has triggered.

Market participants, as they are prone to do even when times are good and the sun is shining, are bringing up the R word: Recession.

Also of concern is Recession’s cousin - Stagflation. In that case, we get both a weaker economy and higher prices.

The latter is bad news for most borrowers, and not all companies can overcome its challenges.

It’s not even clear what the Fed might do to tackle this new threat that has been triggered by the war and high oil and other commodity prices.

Typically, higher inflation brings on an increase in interest rates - a positive for BDC lenders up to a point.

However, the Fed might be more worried about a weakening economy and head in the other direction.

Then we might have the much lower interest-rate environment the Trump Administration has been rooting for, but for the wrong reason.

Clearly, nobody is fully in control of the macro environment at the moment or can say what the next few weeks will bring, even if the war ends.

All we can say is that both lower rates and economic contraction are Kryptonite for lenders and for BDC prices.

The painful price drops that began in Week 4 of this year and have brought BIZD down by about (15%) are not factoring in those contingencies.

Different View

In fact, we’ll get a little controversial here and suggest the damage to BDC stock prices in recent weeks has been relatively orderly and rational.

We’ve looked at our data across several BDCs and calculated how much their earnings have decreased since the heady days of high interest rates and wide spreads in 2023 to their current tepid level.

At the same time, we’ve calculated by what percentage their stock prices have dropped from their frothiest highs - typically in 2022 or 2023 - to today.

In many cases, percentage declines are very similar, suggesting that investors are mostly reacting to being paid less rather than panicking about what may be lurking around the corner.

Unfortunately, that also means that if conditions worsen, investors could sharpen their pencils even more.

We don't believe we've seen a full-blown panic as yet, and we - hopefully - will not.

Bull Case

In all this gloom, there is a more optimistic perspective.

Prices have come down a good deal, and there are - even after adjusting for lower distribution levels - some very high yields available out there in BDC-land.

Should the war be concluded shortly and the worries about the economy subside, as they have waxed and waned many times before since the GFC, investors might be tempted to jump back in.

Others might be drawn in if the Fed, with Chairman Powell vindicated by the courts, decides to hold the line on inflation by maintaining or increasing interest rates in 2026 and into 2027.

Stability might encourage more M&A, which would boost BDC lending.

Finally, all the troubles facing the Private Credit sector might widen spreads on new loans across the board as non-traded BDCs spend most of their time drawing down their own portfolios to meet redemptions.

Bottom Line

As always, this could go any number of ways.

We must say, though, that the markets have never been as gloomy as this since the you-know-what, and sentiment has a lot to do with BDC investing.

On the other hand, we’ve seen markets change their mind very suddenly and starkly and - often - when all seems bleakest and irresolvable.

It’s unlikely that we’ll see a return to the BDC price levels of Week 4, but there could be a bounce should the general mood improve.