BDC Common Stocks Market Recap: Week Ended March 20, 2026

BDC COMMON STOCKS

Week 12

Wall Street ended the week substantially lower as concerns about the conflict in the Middle East lingered and oil prices stayed higher at around $100 per barrel. Meanwhile, the Federal Reserve announced its decision to keep interest rates unchanged, as widely expected.

In economic news, the February Producer Price Index came in hotter at +0.7% month-over-month, compared to the expected +0.3%, and Core PPI, excluding foods and energy, was +0.5% month-over-month vs. +0.3% consensus.

For the week, the S&P (SP500) lost -1.9%, while the tech-heavy Nasdaq Composite (COMP:IND) dipped -2.1%, and the blue-chip Dow (DJI) fell -2.1%.

seeking alpha- wall street breakfast - march 21, 2026

Go Your Own Way

Every market is reacting to the conflict in the Middle East in its own way.

In the case of the public BDC sector - as measured by its only exchange-traded fund with the ticker BIZD - investors are peeking out of their foxholes after experiencing a (12%) downturn in price which began January 15, 2026, and reached a nadir on March 13.

Hope has been rekindled with BIZD increasing for the second time in the past 3 weeks: up 1.8%.

That’s the strongest weekly percentage price increase since early December of last year.

Early in the week, the bounce back was even more pronounced, but the general gloominess about oil prices, etc., impacted sentiment in the latter half of the week.

BIZD reached $13.09 intra-week but closed on Friday at $12.70.

Choosy

In any case, investor optimism seemed to be selective.

As you might expect, there were no new 52-week highs to write about, but there were 11 new 52-week lows: nearly a quarter of our coverage universe.

Most of the BDCs involved had underperformed in the BDC Performance Table.

Apparently, investors are not in a forgiving mood, with most of the BDCs involved continuing to reach new lows in recent months.

At a time when the largest asset managers are under scrutiny, we note that both FS-KKR Capital (FSK), managed by KKR, and Oaktree Specialty Lending (OCSL), managed by Oaktree, were at new lows this week.

Not far behind are many other famous capital raisers, such as BlackRock (TCPC), New Mountain (NMFC), Ares Management (ARCC), and Blackstone (BXSL).

Amusing

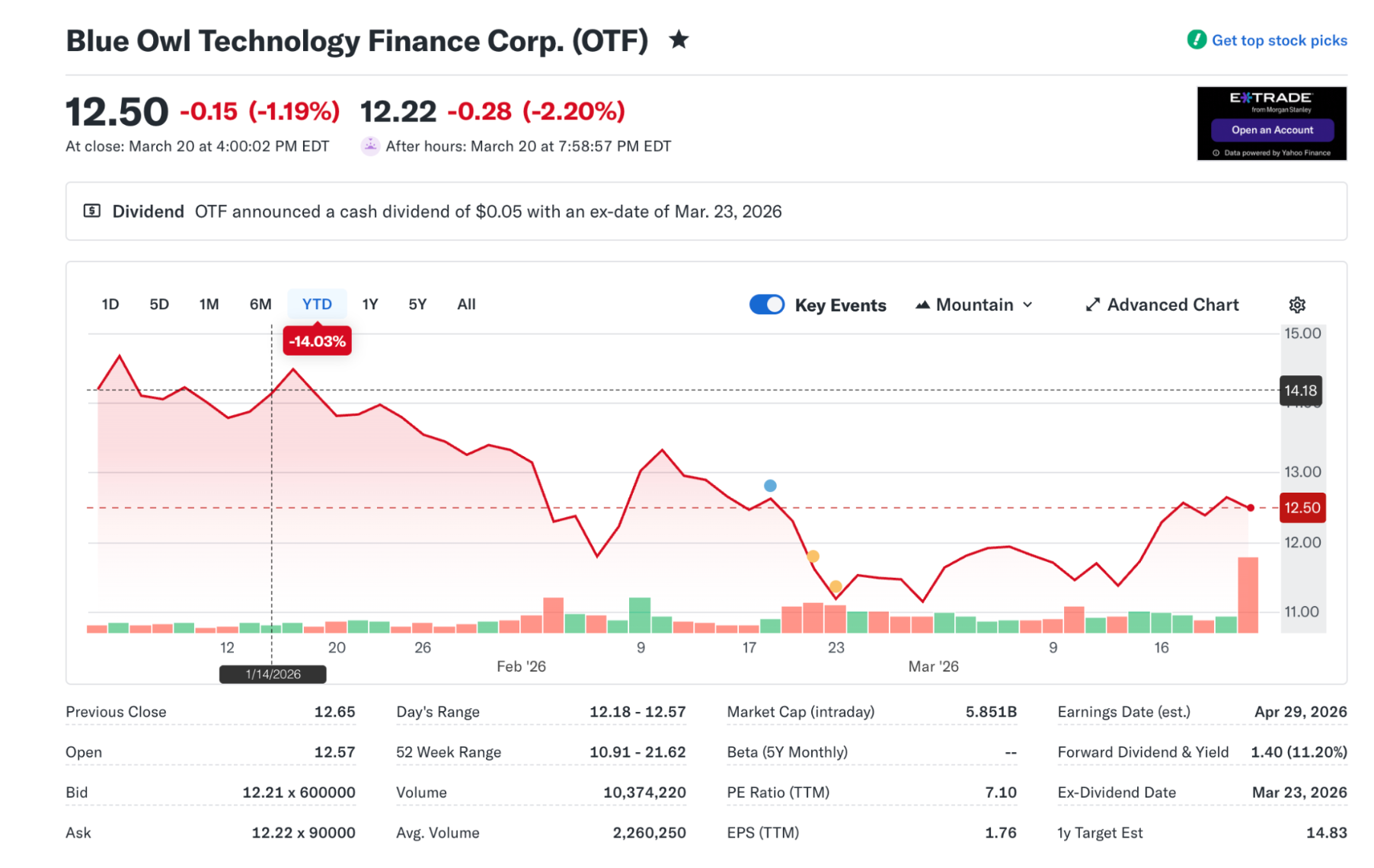

In one of those delicious ironies of investing, Blue Owl Technology Finance (OTF) - much shunned a few weeks ago for having the biggest percentage of software loans of any BDC - has moved sharply off its own 52-week low.

Investors are always keen to jump on a perceived opportunity.

After all, the BDC Reporter did rate OTF's most recent financial performance a 1 on our 5-point scale, meaning “performing better than expectations”.

Maybe more importantly, the BDC Credit Reporter, which has its own rating protocol, continues to assign OCSL its highest rating on credit outlook as well.

Admittedly, the BDC Credit Reporter is not conceding en masse.

If one is worried about that eventuality, OTF might be a BDC to avoid, along with several other large-cap names.

For those less intimidated, OTF offers a yield of just over 11% per annum, as shown in this Yahoo Finance screenshot.

Similar

By the way, we can’t help noticing that most of the BDCs whose dividend payouts seem stable for the foreseeable future are paying a dividend yield of about 11%.

Will that be a juicy enough return to draw investors back in, given the macro backdrop?

WHERE WE ARE

Still Not Good

This week’s mild price rebound notwithstanding, the public BDC sector remains in poor shape after 12 weeks, including 3 weeks of war and roughly 7 weeks of unrelentingly poor press about the future of Private Credit.

BIZD is down (10.4%) on the year in price terms, and even the S&P BDC Index - calculated on a total return basis - is (11.5%) down.

If we look further back to when BIZD peaked in February 2025, the fall from grace - whichever way you cut it - has been extreme:

“Since February 17, 2025 was Presidents' Day (market closed), the nearest trading day peak was February 19, 2025, when BIZD closed at $17.82. From that peak through March 20, 2026, BIZD's total return has been approximately -19.4%”.Perplexity Calculation

Price-wise, only 5 BDCs have avoided a price decline in 2026, and only 6 are trading at a premium to book.

Piling on, our data shows only 2 BDCs trading within 10% of their 52-week highs and none within 5%.

At the other end of this measure, 6 BDCs are trading within 5%-10% of their 52-week lows, and a massive 31 are within 5%...

As they say, we appear to be “bouncing along the bottom”.

WHERE WE ARE HEADED

Darkest Before Dawn Analogy?

BDC prices - and BDC investors - have been beaten up for over a year now.

Investors know that nothing goes on forever.

In fact, BDCs have been through long sour patches like this one before, only to recover and reach new heights.

We don’t have a BIZD chart to show you because the ETF’s trading history is relatively short.

For an illustration of our point, check out what happened to Ares Capital’s (ARCC) stock between November 2013 and February 2016.

ARCC dropped (26%) in that almost 3-year period in seven sharp jags as every rebound was met with more selling.

Cause And Effect

We were around for that episode, which involved - ironically enough, given the current macro narrative - the drastic fall in oil prices from $100+ a barrel.

Many BDCs - including ARCC - had committed substantial funds to the energy sector, drawn in by the promise of “fracking”.

Once again, the now much reviled Private Equity and Private Credit machines had jumped on an opportunity to deploy capital in a big way.

As sometimes happened, that was mostly a mistake, and for years after the oil price drop, BDCs were kept busy restructuring, merging, and selling their loans to energy producers and service providers.

We’re not saying that BDC prices are going up from here or that they’re going down.

Determining those timelines is impossible, as those ARCC investors in 2013-2016 discovered 7 times.

We Promise

What we are saying is that at some point, BDC prices will rise for a sustained period.

More importantly, the energy downturn episode is also a reminder that the BDC managers may make mistakes, but they adapt and come roaring back.

Since February 2016, ARCC has both increased its dividend payout and seen its stock price increase 73%.

Another History Lesson

There are several reasons for the resilience of the BDC model: the highly diversified nature of portfolios, the relatively low leverage deployed, and the credit skills of the managers in the face of unexpected conditions.

Regarding that last point, which many critics would not concede, we have a more recent example to point to: how the BDCs contended with the across-the-board downturn that occurred at the beginning of COVID.

Then, as now, there were many skeptics contending that the end was near for the entire sector.

Instead, the BDCs ducked and weaved in a variety of ways - temporarily suspending distributions; calling for PE sponsors to provide capital support; PIK-ing (the horror!) some loans or advancing new monies; granting waivers, etc.

Thanks to all that - and the biggest instance of corporate welfare in American history - COVID losses were modest, and the sector quickly recovered and went on to thrive through 2022.

However, that’s with the benefit of hindsight.

Wild Days

BDC investors panicked in a way that makes the current situation seem almost orderly, with BIZD dropping (60%) in the course of a month.

There were no temporary upward jags. Everybody - so it seemed - was a seller.

Not The Same

The current dilemma is different. The BDC sector faces another challenge to the perceived creditworthiness of one of its favorite sectors (Software borrowers), and - hiding in plain sight - the prospect of a recession before long, should the war in the Middle East and other actions by the Trump Administration tip us into an economic contraction.

Unlike the situation with COVID, there’s no clear end date for these potential risks, which may end up keeping BDC investors guessing for many months - or years - to come.

On the other hand - and we’ve seen this before as well - investors might just get tired of worrying and move back into BDC stocks that are paying some of the highest dividend yields we’ve seen in years.

Still Standing After All This Time

For our part, our only certainty is that both Private Credit and the public BDC sector will survive whatever the future holds.