BDC Common Stocks Market Recap: Week Ended March 6, 2026

BDC Common Stocks

Week 10

For the week, the S&P (SP500) lost -2.0%, while the tech-heavy Nasdaq Composite (COMP:IND) dipped -1.2%, and the blue-chip Dow (DJI) fell -3.0%.

seeking alpha - wall street breakfast - March 7, 2026

Not On The Agenda

Surprisingly, in a week that saw all the major indices in the red and a new war in the Middle East leaving thousands dead, the BDC sector moved up in price by 1.2%.

This was all the more unexpected because BDCs - both public and private - have been caught up in the most negative environment we can remember since the GFC.

There has been an unrelenting campaign in the media warning against the risks inherent in “Private Credit”, which has gone so far as to suggest we are on the edge of a new Great Financial Crisis (GFC).

The nay-sayers have had a massive impact on BDC prices. Until this week’s reprieve, BIZD - the Van Eck exchange-traded fund, which is the sector’s bellwether, has fallen (12.3%) in price over six weeks.

“Dead cat” or otherwise, BIZD finally moved up, along with 26 of the 46 individual BDCs we track.

9 BDCs moved up 3.0% or more in price, led by WhiteHorse Finance (WHF), which perked up by 18%.

Investors may be reacting to the BDC’s quarterly increase in its net asset value per share (NAVPS) or the slight increase in WHF’s recurring earnings and a 1-cent per share supplemental dividend announced over its recently reduced quarterly payout of $0.25.

For the record, our own assessment of performance was less rosy. The quarter-over-quarter EPS increase was mostly due to one-time or intermittent items, which may not show up next quarter.

The unrealized gain on the portfolio in the quarter was only $1.2mn, and the year-end unrealized gain was ($20mn) when the benefit of writing back realized losses booked is taken into account.

Those realized losses - by the way - amounted to ($35mn) in 2025, twice the level of the year before and far in excess of what WHF earned in Net Investment Income.

Maybe more importantly, WHF, on its conference call, candidly admitted that several troubled portfolio companies are faring worse in 2026, which may result in further write-downs.

In any case, investors looking to “buy at the bottom” rushed in this week. Time will tell if WHF has turned itself around, or not.

Flip Side

Getting back to the week that just was, we shouldn’t make too much of the change in tone.

After all, many BDCs continue to bleed price-wise, with as many down by (3.0%) or more as were up.

The most spectacular backfire occurred at Horizon Technology Finance (HRZN) and Monroe Capital (MRCC), down (30%) and (27%) respectively, in 5 trading days!

As our readers will know, these two very different BDCs - one in venture lending and the other operating in the middle market - are to be wed - so to speak - in a few weeks in a merger.

Or are they? After both BDCs posted terrible IVQ 2025 results, which included a big dividend cut at HRZN, a leading shareholder of MRCC called for the nuptials to be called off:

SADDLE BROOK, N.J., March 06, 2026 (GLOBE NEWSWIRE) -- Bulldog Investors, LLP (“Bulldog”), one of the largest shareholders of Monroe Capital Corporation (MRCC), holding 954,816 shares, announced today that it is urging Monroe’s Board of Directors to reconsider the proposed merger of Monroe into Horizon Technology Finance Corporation (HRZN)...

Phillip Goldstein, a managing partner of Bulldog, stated: “What appeared to be an attractive transaction for Monroe shareholders last August has unraveled just a few days before the special meeting to vote on the merger. Given that Monroe’s most recent NAV is $7.68 or 70% above its current market price, we think that, absent improved terms, the merger with Horizon is not in the best interest of Monroe’s stockholders. Consequently, we urge the Board to consider restructuring the merger. Alternatively, the Board should consider other measures to maximize shareholder value, including letting Monroe gradually wind down and making cash distributions to shareholders.”

This challenge to a process already well underway occurred late on Friday, so we’ll have to see how this plays out next week.

Also down drastically in price this week and reaching new record lows were PhenixFin (PFX) and the former Portman Ridge Finance, now called BCP Investment Corp (BCIC).

PFX fell (15%) and BCIC (12%).

We can’t put our finger on the reason for the former’s price drop, but the latter’s (16%) dividend cut and (5.0%) drop in NAVPS are the likely culprits.

WHERE WE STAND

Sad To Say

This week’s perk up notwithstanding, the public BDC sector remains in very poor shape in 2026.

BIZD is down (9.5%) in price terms in 10 weeks of 2026 and (9.2%) on a total return basis.

At this point, 38 of the BDCs are in the red price-wise, some by massive margins.

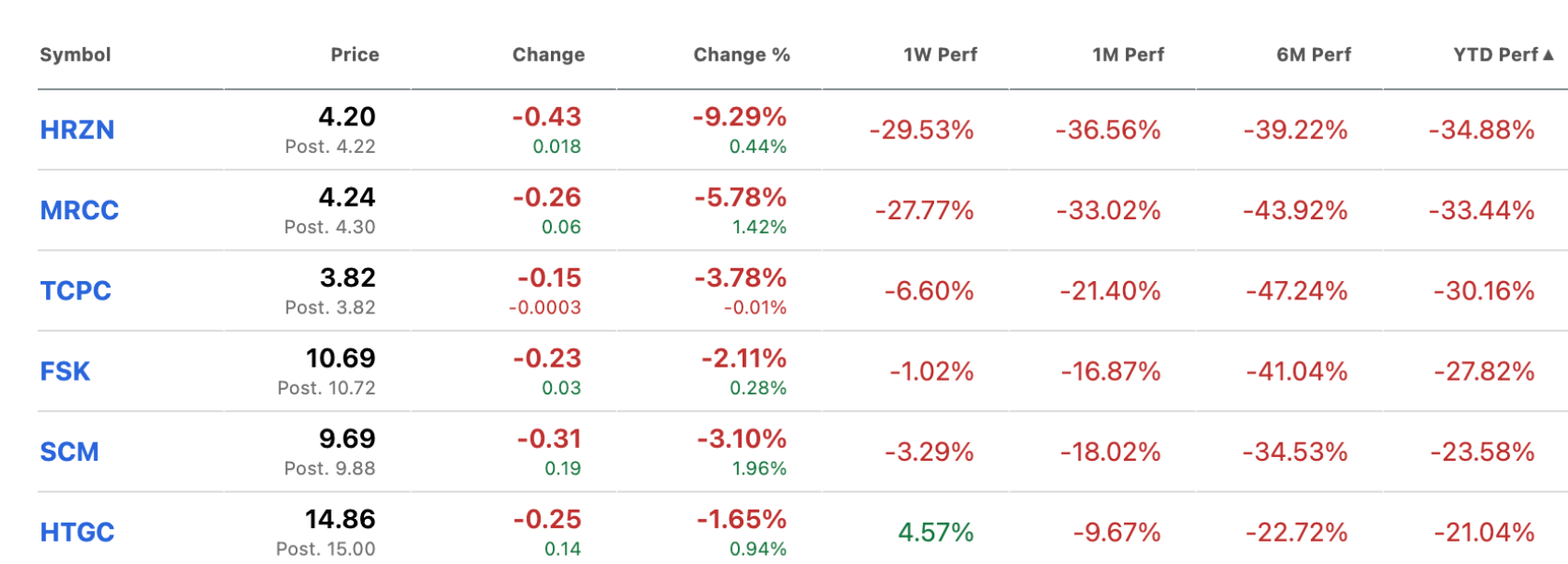

As this chart shows, 6 are off by more than (20%):

We can understand how HRZN, MRCC, TCPC, and FSK have made the list.

If you look at the BDC Performance Table, all of those BDCs have received a Performance Rating of 4 or 5 - the two lowest rungs on our scale, where their IVQ 2025 results are concerned.

Collectively, these 4 BDCs have accumulated (30%) of lower NAVPS in the quarter, albeit that TCPC accounted for (19%).

Poor old Stellus Capital (SCM) has not even reported its results yet, while Hercules Capital (HTGC) had a very robust IVQ 2025 and received a Performance Rating of 1 from the BDC Reporter.

However, the venture-debt giant is being brought low - rightly or wrongly - by market concerns over AI, the overarching theme of the last few weeks.

Otherwise, only 6 BDCs are trading over book, up from 5 the week before.

In price terms, only 1 BDC can boast a stock price within 10% of its 52-week high, and 37 are trading somewhere from 0% to 10% from their 52 week low.

These are difficult times to be a BDC investor, made worse by the fact that 2025 was a loss year as well.

Even when we widen the lens, we can see that outside of Covid, BIZD is at the lowest point in its history:

WHERE WE ARE HEADED

Chilly

It’s far, far too early to say the BDC price tide has turned, this week’s increase in BIZD notwithstanding.

We may be close to the end of earnings season, but most of the pressure on the sector revolves around what might, or might not, be coming up in the quarters ahead.

As always, the market is looking for some clarity on the direction of interest rates and inflation, both of which are inextricably linked.

We’ve found ourselves convincing ourselves one moment that rates will not drop any further because the Iran War should boost an inflation rate that was already too high.

Then we had the weak employment numbers, which suddenly suggested the economy might be weakening and cause the Fed to bow to the Administration’s demands for lower rates.

Then there’s the continuing malaise about the potential reshaping of the entire U.S. economy by AI, which could cause a massive increase in failures of Private Credit/BDC-financed companies.

A UBS team that does not even specialize in BDCs used data from our segment to argue that default rates could reach as high as 15%in a “tail‑risk stress case.”..

However, UBS has not shown anyone but their clients how they came to their numbers, but that has not stopped their “worst case scenario” from getting a lot of airplay in the media.

For the record, the language UBS uses in its publicly available documents is much milder than is typically being quoted. Here’s an extract:

- “AI disintermediation risk has emerged as an important market narrative in recent weeks. US software and IT services have been hard hit, with the S&P 500 software index down close to 30% from its fall 2025 high, as rapid advances in agentic AI inject new uncertainty over the terminal value of traditional software models.”

- “Sectors perceived as most exposed to AI disruption, such as software, services, and insurance brokers, have seen significant spread widening.”

- “We think AI disintermediation risks in credit are real. But the more pressing question is how and where this translates into pressure on cash flows, leverage, and refinancing risk.”

- “We think credit markets are likely to remain resilient, with these AI-related risks unlikely to spill over into sustained stress.”

OUR VIEW

All over the markets, a sort of panic has developed about the outlook for Private Credit. Here is a small collection of what we hear daily - and which we respond to on X:

“Unfortunately, we did see this in ’05, ’06 and ’07, almost the same thing — the rising tide was lifting all boats, everyone was making a lot of money… My own view is that people are getting a little comfortable that this is real — that these high asset prices and high volumes mean we won’t have any kind of problem whatsoever… I see a couple of people doing some dumb things.”

— Jamie Dimon, JPMorgan CEO, investor day remarks, February 23, 2026 (via Business Insider and related coverage)

“The private credit stress has started with Blue Owl and New Mountain, and this is likely the early phase of an unfolding financial crisis.”

— Seeking Alpha, “It’s An Early Phase Financial Crisis: The Private Credit Bust,” February 27, 2026

“Private credit is easy to enter but hard to exit. Retail investors seeking fast cash could trigger a financial crisis… A spiral of illiquidity, forced selling, markdowns and deleveraging could emerge – amplified by opacity and rapidly fading trust.”

— Fabio Natalucci, as quoted in MarketWatch/Morningstar commentary, February 25, 2026

Now, commentators and market participants are looking for confirmatory evidence anywhere they can, whether it’s the write-off of a BlackRock TCP (TCPC) loan whose challenges date back to 2022, or private BDC investors wanting to take out more than the 5% of net assets that they agreed to out of their non-traded BDCs.

The big asset managers are seeing their stock prices destroyed and are spending most of their time on PR damage control.

Some of this anxiety has begun to impact the actual prices at which leveraged loans and high yield bonds trade, and there are anecdotal reports that new advances are being made at wider spreads.

We’re not at crisis levels as yet, as market professionals are not readily swayed, but infections can spread…

Worse

Actually, much more frightening than the AI risk in the short term is that the U.S. economy gets tripped up by some or all of the headwinds the Trump Administration faces.

Should an economic downturn occur - seemingly out of a clear blue sky - the impact on the already tetchy markets, and then later on, Private Credit borrowers could be substantial.

We may not see a 15% default rate, but a doubling or tripling of defaults from the current amount expected, coupled with the impact of the much lower interest rates that might follow, could be deeply impactful for BDC prices.

As we’ve seen, the markets don’t wait around for confirmation.

If confidence truly begins to evaporate, expect much more “sell, sell, sell” across the board.

This is no time to take one’s eye off the ticker.