Barings BDC

Organization

We are a Maryland corporation incorporated on October 10, 2006. We currently operate as a closed-end, non-diversified investment company and have elected to be treated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). Our wholly-owned subsidiary, Triangle Mezzanine Fund LLLP (“Triangle SBIC”) has also elected to be treated as a BDC under the 1940 Act. We have elected for federal income tax purposes to be treated as a regulated investment company (“RIC”) under the Internal Revenue Code of 1986, as amended (the “Code”), for tax purposes. Our headquarters are in Charlotte, North Carolina, and our Internet address is www.baringsbdc.com.

The Asset Sale and Externalization Transactions

On April 3, 2018, we entered into an asset purchase agreement (the “Asset Purchase Agreement”), with BSP Asset Acquisition I, LLC (the “Asset Buyer”), an affiliate of Benefit Street Partners L.L.C. (“BSP”), pursuant to which we agreed to sell our December 31, 2017 investment portfolio to the Asset Buyer for gross proceeds of $981.2 million in cash, subject to certain adjustments to take into account portfolio activity and other matters occurring since December 31, 2017 (such transaction referred to herein as the “Asset Sale Transaction”). Also on April 3, 2018, we entered into a stock purchase and transaction agreement (the “Externalization Agreement”), with Barings LLC (“Barings”) through which Barings agreed to become our investment adviser in exchange for (1) a payment by Barings of $85.0 million, or approximately $1.78 per share, directly to our stockholders, (2) an investment by Barings of $100.0 million in newly issued shares of our common stock at net asset value and (3) a commitment from Barings to purchase up to $50.0 million of shares of our common stock in the open market at prices up to and including our then-current net asset value per share for a two-year period, after which Barings agreed to use any remaining funds from the $50.0 million to purchase additional newly-issued shares of our common stock at the greater of our then-current net asset value per share or market price (collectively, the “Externalization Transaction”). The Asset Sale Transaction and the Externalization Transaction are collectively referred to as the “Transactions.” The Transactions were approved by our stockholders at our July 24, 2018 special meeting of stockholders (the “2018 Special Meeting”).

The Asset Sale Transaction closed on July 31, 2018. The gross cash proceeds received from the Asset Buyer and certain affiliates of the Asset Buyer in connection with the Asset Sale Transaction were approximately $793.3 million, after adjustments to take into account portfolio activity and other matters occurring since December 31, 2017, as described in greater detail in the Asset Purchase Agreement. Adjustments to the purchase price included, among other things, approximately $208.8 million of principal payments and prepayments, sales proceeds and distributions related to our investment portfolio that were received and retained by us between December 31, 2017 and the closing of the Asset Sale Transaction, offset by approximately $29.5 million of loans and equity investments originated by us between December 31, 2017 and the closing of the Asset Sale Transaction.

The Externalization Transaction closed on August 2, 2018 (the “Externalization Closing”). Effective as of the Externalization Closing, we changed our name from Triangle Capital Corporation to Barings BDC, Inc. and on August 3, 2018, began trading on the New York Stock Exchange (“NYSE”) under the symbol “BBDC.”

In connection with the closing of the Externalization Transaction, we entered into an investment advisory agreement (the “Advisory Agreement”) and an administration agreement (the “Administration Agreement”) with Barings, pursuant to which Barings serves as our investment adviser and administrator and manages our investment portfolio which initially consisted primarily of the cash proceeds received in connection with the Asset Sale Transaction. In addition, on August 2, 2018, we issued 8,529,917 shares of our common stock to Barings at a price of $11.723443 per share, or an aggregate of $100.0 million in cash. Furthermore, on August 7, 2018, we launched a $50.0 million issuer tender offer (the “Tender Offer”). Pursuant to the Tender Offer, on September 11, 2018, we purchased 4,901,961 shares of our common stock at a purchase price of $10.20 per share, for an aggregate cost of approximately $50.0 million, excluding fees and expenses relating to the Tender Offer. The shares of common stock purchased in the Tender Offer represented approximately 8.7% of our issued and outstanding shares at the time of the Tender Offer.

STOCK REPURCHASE PROGRAM

On September 24, 2018, Barings entered into a Rule 10b5-1 Purchase Plan (the “10b5-1 Plan”) that qualified for the safe harbors provided by Rules 10b5-1 and 10b-18 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Pursuant to the 10b5-1 Plan, an independent broker made purchases of shares of our common stock on the open market on behalf of Barings in accordance with purchase guidelines specified in the 10b5-1 Plan. The 10b5-1 Plan was established in accordance with Barings obligation under the Externalization Agreement to enter into a trading plan pursuant to which Barings committed to purchase $50.0 million in value of shares in open market transactions through an independent broker. … As of December 31, 2018, Barings had purchased 4,045,248 shares of our common stock pursuant to the 10b5-1 Plan and owned a total of 12,600,627 shares of our common stock, or 24.6% of the total shares outstanding. On February 11, 2019, Barings fulfilled its obligations under the 10b5-1 Plan to purchase an aggregate amount of $50.0 million in shares of our common stock and the 10b5-1 Plan terminated in accordance with its terms. Upon completion of the 10b5-1 Plan, Barings had purchased 5,084,302 shares of our common stock pursuant to the 10b5-1 Plan and owned a total of 13,639,681 shares of our common stock, or 26.6% of the total shares outstanding.

DIRECTORS/EMPLOYEES

As previously disclosed in our definitive proxy statement relating to the Transactions, filed with the SEC on June 1, 2018, and any supplements thereto, collectively referred to as the 2018 Special Meeting Proxy Statement, all of the existing officers and directors resigned effective as of the closing of the Externalization Transaction. In addition, our Board of Directors (the “Board”) approved the election of, effective from and after the closing of the Externalization Transaction, directors identified by Barings and the appointment of each such director to a director class selected by Barings, as disclosed in the 2018 Special Meeting Proxy Statement. The Board has also appointed new officers of the Company as identified by Barings, effective from and after the closing of the Externalization Transaction. Refer to the 2018 Special Meeting Proxy Statement for more information.

Q: Any employees, directors stay on.

From 2007 through the date of the Externalization Transaction, we were internally managed by our executive officers under the supervision of the Board. During this period, we did not pay management or advisory fees, but instead incurred the operating costs associated with employing executive management and investment and portfolio management professionals. On August 2, 2018, we entered into the Advisory Agreement and became an externally-managed BDC managed by Barings.

Overview of Our Business

Prior to the Transactions, our business was to provide capital to lower middle-market companies located primarily in the United States. We focused on investments in companies with a history of generating revenues and positive cash flows, an established market position and a proven management team with a strong operating discipline. Our target portfolio company had annual revenues between $20.0 million and $300.0 million and annual earnings before interest, taxes, depreciation and amortization, as adjusted (“Adjusted EBITDA”) between $5.0 million and $75.0 million. We invested primarily in senior and subordinated debt securities of privately held companies, generally secured by security interests in portfolio company assets. In addition, we generally invested in one or more equity instruments of the borrower, such as direct preferred or common equity interests. Our investments generally ranged from $5.0 million to $50.0 million per portfolio company. The securities in which we invested would be rated below investment grade if they were rated. Such below investment grade securities are often referred to as “high yield” or “junk.”

Beginning August 2, 2018, Barings shifted our investment focus to invest in syndicated senior secured loans, bonds and other fixed income securities. Over time, Barings expects to transition our portfolio to senior secured private debt investments in performing, well-established middle-market businesses that operate across a wide range of industries. Generally, these securities would also be rated below investment grade if they were rated. Barings’ existing SEC exemptive relief under Sections 17(d) and 57(i) of the 1940 Act and Rule 17d-1 thereunder, granted on October 19, 2017 (the “Exemptive Relief”), permits us and Barings’ affiliated private funds and SEC-registered funds to co-invest in Barings-originated loans, which allows Barings to implement its senior secured private debt investment strategy for us on an accelerated timeline.

Q: Peers

Barings employs fundamental credit analysis, and targets investments in businesses with relatively low levels of cyclicality and operating risk. The holding size of each position will generally be dependent upon a number of factors including total facility size, pricing and structure, and the number of other lenders in the facility. Barings has experienced managing levered vehicles, both public and private, and will seek to enhance our returns through the use of leverage with a prudent approach that prioritizes capital preservation. Barings believes this strategy and approach offers attractive risk/return with lower volatility given the potential for fewer defaults and greater resilience through market cycles. We generate revenues in the form of interest income, primarily from our investments in debt securities, loan origination and other fees and dividend income. Fees generated in connection with our debt investments are recognized over the life of the loan using the effective interest method or, in some cases, recognized as earned. Our syndicated senior secured loans generally bear interest between LIBOR plus 300 basis points and LIBOR plus 400 points. As we transition to senior secured private debt investments, such investments will generally have terms of between five and seven years. Our senior secured private debt investments generally will bear interest between LIBOR plus 450 basis points and LIBOR plus 650 basis points per annum. From time to time, certain of our investments may have a form of interest, referred to as payment-in-kind (“PIK”) interest, that is not paid currently but is instead accrued and added to the loan balance and paid at the end of the term. As of December 31, 2018, we had investments in 139 portfolio companies, with an aggregate cost of approximately $1,173.9 million.

Relationship with Our Adviser, Barings

Our investment adviser, Barings, a wholly-owned subsidiary of Massachusetts Mutual Life Insurance Company (“MassMutual”), is a leading global asset management firm and is registered with the SEC as an investment adviser under the Investment Advisers Act of 1940, as amended (the “Advisers Act”). Barings’ primary investment capabilities include fixed income, private credit, real estate, equity, and alternative investments. Subject to the overall supervision of the Board, Barings’ Global Private Finance Group (“Barings GPFG”) manages our day-to-day operations, and provides investment advisory and management services to us. Barings GPFG is part of a $225 billion Global Fixed Income Platform that invests in liquid, private and structured credit. Barings GPFG manages private funds and separately managed accounts, along with multiple public vehicles.

Small Business Credit Availability Act

On July 24, 2018, our stockholders voted at the 2018 Special Meeting to approve a proposal to authorize us to be subject to a reduced asset coverage ratio of at least 150% under the 1940 Act. As a result of the stockholder approval at the 2018 Special Meeting, effective July 25, 2018, our applicable asset coverage ratio under the 1940 Act has been decreased to 150% from 200%. As a result, we are now permitted under the 1940 Act to incur indebtedness at a level that is more consistent with a portfolio of senior secured debt.

Our Business Strategy

We seek attractive returns by generating current income primarily from directly-originated debt investments in middle-market companies located primarily in the United States. Our strategy includes the following components:

|

•

|

Leveraging Barings GPFG’s Origination and Portfolio Management Resources. Barings GPFG has over 70 investment professionals located in seven different offices in the U.S., Europe, Australia/New Zealand and Asia. These regional investment teams have been working together in their respective regions for a number of years and have extensive experience advising, investing in and lending to companies across changing market cycles. In addition, the individual members of these teams have diverse investment backgrounds, with prior experience at investment banks, commercial banks, and privately and publicly held companies. We believe this diverse experience provides an in-depth understanding of the strategic, financial and operational challenges and opportunities of middle-market companies.

|

|

•

|

Utilizing Long-Standing Relationships to Source Investments. Barings GPFG has worked diligently over decades to build strategic relationships with private equity firms globally. Barings GPFG’s long history of providing consistent, predictable capital to middle-market sponsors, even in periods of market dislocation, has earned Barings and us a reputation as a reliable partner. Barings GPFG also maintains extensive personal relationships with entrepreneurs, financial sponsors, attorneys, accountants, investment bankers, commercial bankers and other non-bank providers of capital who refer prospective portfolio companies to us. These relationships historically have generated significant investment opportunities. We believe that this network of relationships will continue to produce attractive investment opportunities.

|

|

•

|

Focusing on the Middle-Market. We primarily invest in middle-market transactions. These companies tend to be privately owned, often by a private equity sponsor, and are companies that typically generate annual Adjusted EBITDA of $10.0 million to $75.0 million.

|

|

•

|

Providing One-Stop Customized Financing Solutions. Barings GPFG’s ability to commit to and originate larger hold positions (in excess of $200 million) in a given transaction is a differentiator to middle-market private equity sponsors. In today’s market, it has become increasingly important to have the ability to underwrite an entire transaction, providing financial sponsors with certainty of close. Barings GPFG offers a variety of financing structures and has the flexibility to structure investments to meet the needs of our portfolio companies. Currently, we invest primarily in senior secured loans. In addition, in certain limited

|

7

instances, we may invest in equity instruments of our portfolio companies, such as direct preferred or common equity interests.

|

•

|

Applying Consistent Underwriting Policies and Active Portfolio Management. We believe robust due diligence on each investment is paramount due to the lack of an active secondary market. With limited ability to liquidate holdings, private credit investors must take a longer-term, “originate-to-hold” investment approach. Barings GPFG has implemented underwriting policies and procedures that are followed for each potential transaction. This consistent and proven fundamental underwriting process includes a thorough analysis of each potential portfolio company’s competitive position, financial performance, management team operating discipline, growth potential and industry attractiveness, which Barings GPFG believes allows them to better assess the company’s prospects. After closing, Barings GPFG maintains ongoing access to both the sponsor and to portfolio company management in order to closely monitor investments and suggest or require remedial actions as needed to avoid a default.

|

|

•

|

Maintaining Portfolio Diversification. While we focus our investments in middle-market companies, we seek to invest across various industries. Barings GPFG monitors our investment portfolio to ensure we have acceptable industry balance, using industry and market metrics as key indicators. By monitoring our investment portfolio for industry balance, we seek to reduce the effects of economic downturns associated with any particular industry or market sector. Notwithstanding our intent to invest across a variety of industries, we may from time to time hold securities of a single portfolio company that comprise more than 5.0% of our total assets and/or more than 10.0% of the outstanding voting securities of the portfolio company. For that reason, we are classified as a non-diversified management investment company under the 1940 Act.

|

Investments

Debt Investments

The terms of our debt investments are tailored to the facts and circumstances of each transaction and prospective portfolio company, negotiating a structure that seeks to protect lender rights and manage risk while creating incentives for the portfolio company to achieve its business plan. We also seek to limit the downside risks of our investments by negotiating covenants that are designed to protect our investments while affording our portfolio companies as much flexibility in managing their businesses as possible. Such restrictions may include affirmative and negative covenants, default penalties, lien protections, change of control provisions, put rights and a pledge of the operating companies’ stock which provides us with additional exit options in downside scenarios. Other lending protections may include term loan amortization, excess cash flow sweeps (effectively additional term loan amortization), limitations on a company’s ability to make acquisitions, maximums on capital expenditures and limits on allowable dividends and distributions. Further, up-front closing fees of typically 1-3% of the loan amount act effectively as pre-payment protection given the cost to a company to refinance early. Additionally, we typically include call protection provisions effective for the first six to twelve months of an investment to enhance our potential total return.

Prior to the Transactions, we invested in senior and subordinated debt securities of privately-held lower middle-market companies, generally secured by security interests in portfolio company assets. Our senior and subordinated debt investments generally had terms of three to seven years, did not have scheduled amortization and were due at maturity. Our legacy senior secured debt investments generally provided for variable interest at rates ranging from LIBOR plus 550 basis points to LIBOR plus 950 basis points per annum. In addition, our legacy subordinated debt investments generally provided for fixed interest rates between 10.0% and 15.0% per annum. Our subordinated debt investments generally were secured by a second priority security interest in the assets of the borrower and generally included an equity component, such as common stock in the portfolio company. In addition, certain loan investments had PIK interest.

Beginning August 2, 2018, Barings shifted our investment focus to initially invest the proceeds from the Asset Sale Transaction and the stock sale to Barings in syndicated senior secured loans, bonds and other fixed income securities. Over time, Barings expects to transition our portfolio to senior secured private debt investments in performing, well-established middle-market businesses that operate across a wide range of industries. As of December 31, 2018, approximately $845.6 million, or 78.5% of our investment portfolio (excluding our investment in short-term money market funds), was invested in syndicated senior secured loans, and approximately $231.0 million, or 21.5% of our investment portfolio (excluding our investment in short-term money market funds) was invested in senior secured, middle-market, private debt investments. Our syndicated senior secured loans generally bear interest at rates ranging from LIBOR plus 300 basis points to LIBOR plus 400 points per annum. Our senior

8

secured, middle-market, private debt investments generally have terms of between five and seven years, and generally bear interest at rates ranging from LIBOR plus 450 basis points to LIBOR plus 650 basis points per annum. At December 31, 2018, the weighted average yield on our syndicated senior secured loan portfolio was approximately 5.8%, and the weighted average yield on our senior secured, middle-market, private debt portfolio was approximately 7.6%.

Equity Investments

On a limited basis, we may acquire equity interests in portfolio companies. In such cases, we generally seek to structure our equity investments as non-control investments to provide us with minority rights.

Investment Criteria

We utilize the following criteria and guidelines in evaluating investment opportunities. However, not all of these criteria and guidelines have been, or will be, met in connection with each of our investments.

|

•

|

Established Companies With Positive Cash Flow. We seek to invest in later-stage or mature companies with a proven history of generating positive cash flows. We typically focus on companies with a history of profitability and trailing twelve-month Adjusted EBITDA ranging from $10.0 million to $75.0 million.

|

|

•

|

Experienced Management Teams. Based on our prior investment experience, we believe that a management team with significant experience with a portfolio company or relevant industry experience is essential to the long-term success of the portfolio company. We believe management teams with these attributes are more likely to manage the companies in a manner that protects our debt investment.

|

|

•

|

Strong Competitive Position. We seek to invest in companies that have developed strong positions within their respective markets, are well positioned to capitalize on growth opportunities and compete in industries with barriers to entry. We also seek to invest in companies that exhibit a competitive advantage, which may help to protect their market position and profitability.

|

|

•

|

Varied Customer and Supplier Bases. We prefer to invest in companies that have varied customer and supplier bases. Companies with varied customer and supplier bases are generally better able to endure economic downturns, industry consolidation and shifting customer preferences.

|

|

•

|

Significant Invested Capital. We believe the existence of significant underlying equity value provides important support to investments. We seek to identify portfolio companies that we believe have well-structured capital beyond the layer of the capital structure in which we invest.

|

Investment Process

Our investment origination and portfolio monitoring activities are performed by Barings GPFG. Barings GPFG has an investment committee that is responsible for all aspects of the investment process. The investment committee is comprised of six members, including our Chief Executive Officer, Eric Lloyd and our President, Ian Fowler. The investment process is designed to maximize risk-adjusted returns, minimize non-performing assets and avoid investment losses. In addition, the investment process is also designed to provide sponsors and prospective portfolio companies with efficient and predictable deal execution.

9

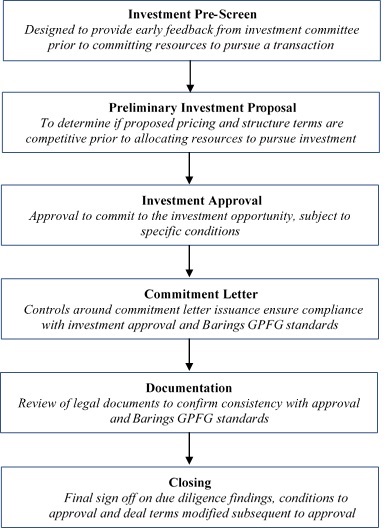

Origination

Our origination process is summarized in the following chart:

Investment Pre-Screen

The investment pre-screen process begins with a review of an offering memorandum or other high-level prospect information by an investment originator. A fundamental bottoms-up credit analysis is prepared and independent third-party research is gathered in addition to the information received from the sponsor. The investment group focuses on a prospective investment’s fundamentals, sponsor/source and proposed investment structure. This review may be followed by a discussion between the investment originator and an investment group head to identify investment opportunities that should be passed on, either because they fall outside of Barings GPFG’s stated investment strategy or offer an unacceptable risk-adjusted return. If the originator and investment group head agree that an investment opportunity is worth pursuing, a credit analyst assists the originator with preparation of a screening memorandum. The screening memorandum is discussed internally with the investment group head and other senior members of the investment group, and in certain instances, the investment group head may elect to

Our portfolio management and investment monitoring processes are overseen by Barings GPFG. Barings GPFG’s portfolio management process is designed to maximize risk-adjusted returns and identify non-performing assets well in advance of potentially adverse events in order to mitigate investment losses. Key aspects of the Barings GPFG investment and portfolio management process include:

|

•

|

Culture of Risk Management. The investment team that approves an investment monitors the investment’s performance through repayment…In addition, we foster continuous interaction between investment teams and the investment committee. This frequent communication encourages the early escalation of issues to members of the investment committee to leverage their experience and expertise well in advance of potentially adverse events.

|

|

•

|

Ongoing Monitoring. Each portfolio company is assigned to an analyst who is responsible for the ongoing monitoring of the investment. Upon receipt of information (financial or otherwise) relating to an investment, a preliminary review is performed by the analyst in order to assess whether the information raises any issues that require urgent attention. Particular consideration is given to information which may impact the value of an asset. In the event that something material is identified, the analyst is responsible for notifying the relevant members of the deal team and investment committee.

|

|

•

|

Quarterly Portfolio Reviews. All investments are reviewed on at least a quarterly basis. The quarterly portfolio reviews provide a forum to evaluate the current status of each asset and identify any recent or long-term performance trends, either positive or negative, that may affect its current valuation.

|

|

•

|

Watchlist Reviews. Certain credits are deemed to be on the “Watchlist” and are reviewed on a more frequent basis. These reviews typically occur monthly but can occur more or less frequently based on situational factors and the availability of updated information from the company. During these reviews, the investment team provides an update on the situation and discusses potential courses of action with the investment committee to ensure any mitigating steps are taken in a timely manner.

|

|

•

|

Sponsor Relationships. We invest primarily in transactions backed by a private equity sponsor and when evaluating investment opportunities, we take into account the strength of the sponsor (e.g., track record,

|

11sector expertise, strategy, governance, follow-on investment capacity, relationship with Barings GPFG). Having a strong relationship and staying in close contact with sponsors and management during not only the underwriting process but also throughout the life of the investment allows us to engage the sponsor and management early to address potential covenant breaks or other issues.

|

•

|

Robust Investment and Portfolio Management System. Barings’ investment and portfolio management system serves as the central repository of data used for investment management, including both company-level metrics (e.g., probability of default, EBITDA, geography) and asset-level metrics (e.g., price, spread/coupon, seniority). Barings GPFG portfolio management has established a required set of data that analysts must update quarterly, or more frequently when appropriate, in order to produce a one-page summary for each company, known as tearsheets, which are used during quarterly portfolio reviews.

|

Prior to the Transactions, our valuation process was led by our executive officers. The valuation process began with a quarterly review of each investment in our investment portfolio by our executive officers and our investment committee. Valuations of each portfolio security were then prepared by our investment professionals, who had direct responsibility for the origination, management and monitoring of each investment. Each investment valuation was subject to (i) a review by the lead investment officer responsible for the portfolio company investment and (ii) a peer review by a second investment officer or executive officer. Generally, any investment that was valued below cost was subjected to review by one of our executive officers. After the peer review was complete, we engaged two independent valuation firms, collectively referred to as the Valuation Firms, to provide third-party reviews of certain investments, as described further below. Finally, the Board had the responsibility for reviewing and approving, in good faith, the fair value of our investments in accordance with the 1940 Act.

The Valuation Firms provided third-party valuation consulting services to us which consisted of certain limited procedures that we identified and requested the Valuation Firms to perform (referred to herein as the “Procedures”). The Procedures were performed with respect to each portfolio company at least once in every calendar year and for new portfolio companies, at least once in the twelve-month period subsequent to the initial investment. In addition, the Procedures were generally performed with respect to a portfolio company when there was a significant change in the fair value of the investment. In certain instances, we determined that it was not cost-effective, and as a result was not in our stockholders’ best interest, to request the Valuation Firms to perform the Procedures on one or more portfolio companies. Such instances included, but were not limited to, situations where the fair value of the investment in the portfolio company was determined to be insignificant relative to the total investment portfolio. Upon completion of the Procedures, the Valuation Firms would reach a conclusion as to whether, with respect to each investment reviewed by each Valuation Firm, the fair value of those investments subjected to the Procedures appeared reasonable.

Investment Valuation Process Subsequent to the Transactions

Barings has established a Pricing Committee that is responsible for the approval, implementation and oversight of the processes and methodologies that relate to the pricing and valuation of assets we hold. Barings uses internal pricing models, in accordance with internal pricing procedures established by the Pricing Committee, to price an asset in the event an acceptable price cannot be obtained from an approved external source.

Barings reviews its valuation methodologies on an ongoing basis and updates are made accordingly to meet changes in the marketplace. Barings has established internal controls to ensure our validation process is operating in an effective manner. Barings (1) maintains valuation and pricing procedures that describe the specific methodology used for valuation and (2) approves and documents exceptions and overrides of valuations. In addition, the Pricing Committee performs an annual review of valuation methodologies.

Our money market fund investments are generally valued using Level 1 inputs and our syndicated senior secured loans are generally valued using Level 2 inputs. Our senior secured private middle-market debt investments will generally be valued using Level 3 inputs.

An independent valuation firm is engaged to perform the Procedures with respect to portfolio investments. The Procedures are generally performed with respect to each portfolio investment each quarter beginning in the quarter after the investment is made. In certain instances, we determine that it is not cost-effective, and as a result is not in our stockholders’ best interest, to request independent valuation firms to perform the Procedures on certain portfolio investments. Such instances include, but are not limited to, situations where the fair value of the investment in the portfolio company is determined to be insignificant relative to the total investment portfolio. Finally, the Board has the responsibility for reviewing and approving, in good faith, the fair value of our investments in accordance with the 1940 Act.

We did not engage any independent valuation firms to perform the Procedures for the third quarter of 2018 as our investment portfolio consisted primarily of newly-originated investments. Beginning in the fourth quarter of 2018, we engaged an independent valuation firm to perform the Procedures noted above with respect to certain of our portfolio investments. For a further discussion of the Procedures both before and after the Transactions, see the section entitled “Critical Accounting Policies and Use of Estimates — Investment Valuation” included in

13

vestment was made or had not fluctuated significantly from management’s expectations as of the date the investment was made, and where there had been no significant fluctuations in the market pricing for such investments, we may have concluded that the Required Rate of Return was equal to the stated rate on the investment and therefore, the debt security was appropriately priced. In instances where we determined that the Required Rate of Return was different from the stated rate on the investment, we discounted the contractual cash flows on the debt instrument using the Required Rate of Return in order to estimate the fair value of the debt security.

Fair value measurements using the Income Approach model can be sensitive to changes in one or more of the inputs. Assuming all other inputs to the Income Approach model remain constant, any increase (decrease) in the Required Rate of Return or Leverage Ratio inputs for a particular debt security would result in a lower (higher) fair value for that security. Assuming all other inputs to the Income Approach model remain constant, any increase (decrease) in the Adjusted EBITDA input for a particular debt security would result in a higher (lower) fair value for that security.

Subsequent to the Transactions, we utilize a similar Income Approach model in valuing our private debt investment portfolio, which consists of middle-market senior secured loans with floating reference rates. As vendor and broker quotes have not historically been consistently relevant and reliable, the fair value is determined using an internal index-based pricing model that takes into account both the movement in the spread of a performing credit index as well as changes in the credit profile of the borrower. The implicit yield for each debt investment is calculated at the date the investment is made. This calculation takes into account the acquisition price (par less any upfront fee) and the relative maturity assumptions of the underlying asset. As of each balance sheet date, the implied yield for each investment is reassessed, taking into account changes in the discount margin of the baseline index,

15

probabilities of default and any changes in the credit profile of the issuer of the security, such as fluctuations in operating levels and leverage. If there is an observable price available on a comparable security/issuer, it is used to calibrate the internal model. The implied yield used within the model is considered a significant unobservable input. As such, these assets are generally classified within Level 3. If the valuation process for a particular debt investment results in a value above par, the value is typically capped at the greater of the principal amount plus any prepayment penalty in effect or 100% of par on the basis that a market participant is likely unwilling to pay a greater amount than that at which the borrower could refinance.

Market Approach

We value our syndicated senior secured loans using values provided by independent pricing services that have been approved by the Barings’ Pricing Committee. The prices received from these pricing service providers are based on yields or prices of securities of comparable quality, type, coupon and maturity and/or indications as to value from dealers and exchanges. We seek to obtain two prices from the pricing services with one price representing the primary source and the other representing an independent control valuation. We evaluate the prices obtained from brokers or pricing vendors based on available market information, including trading activity of the subject or similar securities, or by performing a comparable security analysis to ensure that fair values are reasonably estimated. We also perform back-testing of valuation information obtained from pricing vendors and brokers against actual prices received in transactions. In addition to ongoing monitoring and back-testing, we perform due diligence procedures surrounding pricing vendors to understand their methodology and controls to support their use in the valuation process.

Quarterly Net Asset Value Determination

We determine the net asset value per share of our common stock on at least a quarterly basis, and more frequently if we are required to do so pursuant to an equity offering or pursuant to federal laws and regulations. The net asset value per share is equal to the value of our total assets minus total liabilities and any preferred stock outstanding divided by the total number of shares of common stock outstanding.

Managerial Assistance

As a BDC, we offer, and must provide upon request, managerial assistance to certain of our portfolio companies. This assistance typically involves, among other things, monitoring the operations of our portfolio companies, participating in board and management meetings, consulting with and advising officers of portfolio companies and providing other organizational and financial guidance. Barings provides such services on our behalf to portfolio companies that request this assistance. We may receive fees for these services.

Exit Strategies/Refinancing

While we generally exit most investments through the refinancing or repayment of our debt, we typically assist our portfolio companies in developing and planning exit opportunities, including any sale or merger of our portfolio companies. We may also assist in the structure, timing, execution and transition of these exit strategies.

Competition

We compete for investments with a number of investment funds including public funds, private equity funds, other BDCs, as well as traditional financial services companies such as commercial banks and other sources of financing. Some of these entities have greater financial and managerial resources than we do. In addition, some of our competitors may have higher risk tolerances or different risk assessments, which could allow them to consider more investments and establish more relationships than we do. Furthermore, many of our competitors are not subject to the regulatory restrictions that the 1940 Act imposes on us as a BDC.

We use the expertise of the investment professionals of Barings to assess investment risks and determine appropriate pricing for our investments in portfolio companies. We believe the relationship we have with Barings enables us to learn about, and compete for financing opportunities with companies in middle-market businesses that operate across a wide range of industries. For additional information concerning the competitive risks we face, see “Risk Factors — Risks Relating to Our Business and Structure — We operate in a highly competitive market for investment opportunities, which could reduce returns and result in losses” included in Item 1A of Part I of this Annual Report.

Brokerage Allocation and Other Practices

16

We did not pay any brokerage commissions during the three years ended December 31, 2018 in connection with the acquisition and/or disposal of our investments. We generally acquire and dispose of our investments in privately negotiated transactions; therefore, we infrequently use brokers in the normal course of our business. Barings is primarily responsible for the execution of any publicly traded securities portion of our portfolio transactions and the allocation of brokerage commissions. We do not expect to execute transactions through any particular broker or dealer, but will seek to obtain the best net results for us, taking into account such factors as price (including the applicable brokerage commission or dealer spread), size of order, difficulty of execution, and operational facilities of the firm and the firm’s risk and skill in positioning blocks of securities. While we will generally seek reasonably competitive trade execution costs, we will not necessarily pay the lowest spread or commission available. Subject to applicable legal requirements, if we use a broker, we may select a broker based partly upon brokerage or research services provided to us. In return for such services, we may pay a higher commission than other brokers would charge if we determine in good faith that such commission is reasonable in relation to the services provided.

Dividend Reinvestment Plan

We have adopted a dividend reinvestment plan that provides for reinvestment of our distributions on behalf of our common stockholders, unless a common stockholder elects to receive cash as provided below. As a result, if the Board authorizes, and we declare, a cash dividend, then our common stockholders who have not “opted out” of our dividend reinvestment plan will have their cash dividends automatically reinvested in additional shares of our common stock, rather than receiving the cash dividends.

No action will be required on the part of a registered common stockholder to have his or her cash dividend reinvested in shares of our common stock. A registered common stockholder may elect to receive an entire dividend in cash by notifying Computershare, Inc., the “Plan Administrator” and our transfer agent and registrar, in writing so that such notice is received by the Plan Administrator no later than the record date for dividends to common stockholders. The Plan Administrator will set up an account for shares acquired through the plan for each common stockholder who has not elected to receive dividends in cash and hold such shares in non-certificated form. Upon request by a common stockholder participating in the plan, received in writing not less than 10 days prior to the record date, the Plan Administrator will, instead of crediting shares to the participant’s account, issue a certificate registered in the participant’s name for the number of whole shares of our common stock and a check for any fractional share. Those common stockholders whose shares are held by a broker or other financial intermediary may receive dividends in cash by notifying their broker or other financial intermediary of their election.

We intend to use primarily newly issued shares to implement the plan, so long as our shares are trading at or above net asset value. If our shares are trading below net asset value, we intend to purchase shares in the open market in connection with our implementation of the plan. If we use newly issued shares to implement the plan, the number of shares to be issued to a common stockholder is determined by dividing the total dollar amount of the dividend payable to such common stockholder by the market price per share of our common stock at the close of regular trading on the NYSE on the dividend payment date. Market price per share on that date will be the closing price for such shares on the NYSE or, if no sale is reported for such day, at the average of their reported bid and asked prices. If we purchase shares in the open market to implement the plan, the number of shares to be issued to a common stockholder is determined by dividing the total dollar amount of the dividend payable to such common stockholder by the average price per share for all shares purchased by the Plan Administrator in the open market in connection with the dividend. The number of shares of our common stock to be outstanding after giving effect to payment of the dividend cannot be established until the value per share at which additional shares will be issued has been determined and elections of our common stockholders have been tabulated.

There will be no brokerage charges or other charges to common stockholders who participate in the plan. However, certain brokerage firms may charge brokerage charges or other charges to their customers. We will pay the Plan Administrator’s fees under the plan. If a participant elects by written notice to the Plan Administrator to have the Plan Administrator sell part or all of the shares held by the Plan Administrator in the participant’s account and remit the proceeds to the participant, the Plan Administrator is authorized to deduct a $15.00 transaction fee plus a $0.10 per share brokerage commission from the proceeds.

Common stockholders who receive dividends in the form of stock generally are subject to the same federal, state and local tax consequences as are common stockholders who elect to receive their dividends in cash. A common stockholder’s basis for determining gain or loss upon the sale of stock received in a dividend from us will be equal to the total dollar amount of the dividend payable to the common stockholder. Any stock received in a dividend will have a holding period for tax purposes commencing on the day following the day on which the shares

17

are credited to the U.S. common stockholder’s account. Stock received in a dividend may generate a wash sale if such shareholder sold out stock at a realized loss within 30 days either before or after such dividend.

Participants may terminate their accounts under the plan by notifying the Plan Administrator via its website at www.computershare.com/investor, by filling out the transaction request form located at the bottom of their statement and sending it to the Plan Administrator at Computershare, Inc., P.O. Box 505000, Louisville, Kentucky 40233 or by calling the Plan Administrator at (866) 228-7201.

We may terminate the plan upon notice in writing mailed to each participant at least 30 days prior to any record date for the payment of any dividend by us. All correspondence concerning the plan should be directed to the Plan Administrator by mail at Computershare, Inc., P.O. Box 505000, Louisville, Kentucky 40233.

Employees

The services necessary for our business are provided by individuals who are employees of Barings, pursuant to the terms of our Advisory Agreement and our Administration Agreement. Each of our executive officers is an employee of Barings and our day-to-day investment activities are managed by Barings. In addition, as of December 31, 2018, we employed two administrative professionals.

Management Agreements

On August 2, 2018, we entered into the Advisory Agreement and the Administration Agreement with Barings, an investment adviser registered under the Advisers Act. Our then-current board of directors unanimously approved the Advisory Agreement at an in-person meeting on March 22, 2018. Our stockholders approved the Advisory Agreement at the 2018 Special Meeting.

Advisory Agreement

Pursuant to the Advisory Agreement, Barings manages our day-to-day operations and provides us with investment advisory services. Among other things, Barings (i) determines the composition of our portfolio, the nature and timing of the changes therein and the manner of implementing such changes; (ii) identifies, evaluates and negotiates the structure of our investments; (iii) executes, closes, services and monitors the investments that we make; (iv) determines the securities and other assets that we will purchase, retain or sell; (v) performs due diligence on prospective portfolio companies and (vi) provides us with such other investment advisory, research and related services as we may, from time to time, reasonably require for the investment of our funds.

The Advisory Agreement provides that, absent fraud, willful misfeasance, bad faith or gross negligence in the performance of its duties or by reason of the reckless disregard of its duties and obligations, Barings, and its officers, managers, partners, agents, employees, controlling persons, members and any other person or entity affiliated with Barings (collectively, the “IA Indemnified Parties”), are entitled to indemnification from us for any damages, liabilities, costs, demands, charges, claims and expenses (including reasonable attorneys’ fees and amounts reasonably paid in settlement) incurred by the IA Indemnified Parties in or by reason of any pending, threatened or completed action, suit, investigation or other proceeding (including an action or suit by or in the right of us or our security holders) arising out of any actions or omissions or otherwise based upon the performance of any of Barings’ duties or obligations under the Advisory Agreement or otherwise as our investment adviser.

Barings’ services under the Advisory Agreement are not exclusive, and Barings is generally free to furnish similar services to other entities so long as its performance under the Advisory Agreement is not adversely affected.

Under the Advisory Agreement, we pay Barings (i) a base management fee (the “Base Management Fee”) and (ii) an incentive fee (the “Incentive Fee”) as compensation for the investment advisory and management services it provides us thereunder.

Base Management Fee

The Base Management Fee is calculated based on our gross assets, including assets purchased with borrowed funds or other forms of leverage and excluding cash and cash equivalents, at an annual rate of:

|

•

|

1.0% for the period from August 2, 2018 through December 31, 2018;

|

|

•

|

1.125% for the period commencing on January 1, 2019 through December 31, 2019; and

|

|

•

|

1.375% for all periods thereafter.

|

The Base Management Fee is payable quarterly in arrears on a calendar quarter basis. The Base Management Fee is calculated based on the average value of our gross assets, excluding cash and cash equivalents, at the end of the two most recently completed calendar quarters prior to the quarter for which such fees are being calculated. Base Management Fees for any partial month or quarter are appropriately pro-rated.

Incentive Fee

The Incentive Fee is comprised of two parts: (1) a portion based on our pre-incentive fee net investment income (the “Income-Based Fee”) and (2) a portion based on the net capital gains received on our portfolio of securities on a cumulative basis for each calendar year, net of all realized capital losses and all unrealized capital depreciation for that same calendar year (the “Capital Gains Fee”).

The Income-Based Fee is calculated as follows:

|

(i)

|

For each quarter from and after August 2, 2018 through December 31, 2019 (the “Pre-2020 Period”), the Income-Based Fee is calculated and payable quarterly in arrears based on the Pre-Incentive Fee Net Investment Income for the immediately preceding calendar quarter for which such fees are being calculated. In respect of the Pre-2020 Period, “Pre-Incentive Fee Net Investment Income” means interest income, dividend income and any other income (including any other fees, such as commitment, origination, structuring, diligence, managerial assistance and consulting fees or other fees that we receive from portfolio companies) accrued during the relevant calendar quarter, minus our operating expenses for such quarter (including the Base Management Fee, expenses payable under the Administration Agreement, any interest expense and any dividends paid on any issued and outstanding preferred stock, but excluding the Incentive Fee). Pre-Incentive Fee Net Investment Income includes, in the case of investments with a deferred interest feature (such as original issue discount, debt instruments with payment-in-kind interest and zero coupon securities), accrued income not yet received in cash. Pre-Incentive Fee Net Investment Income does not include any realized capital gains, realized capital losses or unrealized capital appreciation or depreciation.

|

|

(ii)

|

For each quarter beginning on and after January 1, 2020 (the “Post-2019 Period”), the Income-Based Fee will be calculated and payable quarterly in arrears based on the Pre-Incentive Fee Net Investment Income for the immediately preceding calendar quarter and the eleven preceding calendar quarters (or such fewer number of preceding calendar quarters counting each calendar quarter beginning on or after January 1, 2020) (each such period will be referred to as the “Trailing Twelve Quarters”) for which such fees are being calculated and will be payable promptly following the filing of the Company’s financial statements for such quarter. In respect of the Post-2019 Period, “Pre-Incentive Fee Net Investment Income” means interest income, dividend income and any other income (including any other fees, such as commitment, origination, structuring, diligence, managerial assistance and consulting fees or other fees that we receive from portfolio companies) accrued during the relevant Trailing Twelve Quarters, minus our operating expenses for such Trailing Twelve Quarters (including the Base Management Fee, expenses payable under the Administration Agreement, any interest expense and any dividends paid on any issued and outstanding preferred stock, but excluding the Incentive Fee) divided by the number of quarters that comprise the relevant Trailing Twelve Quarters. Pre-Incentive Fee Net Investment Income includes, in the case of investments with a deferred interest feature (such as original issue discount, debt instruments with payment-in-kind interest and zero coupon securities), accrued income not yet received in cash. Pre-Incentive Fee Net Investment Income does not include any realized capital gains, realized capital losses or unrealized capital appreciation or depreciation.

|

|

(iii)

|

Pre-Incentive Fee Net Investment Income, expressed as a rate of return on the value of our net assets (defined as total assets less senior securities constituting indebtedness and preferred stock) at the end of the calendar quarter for which such fees are being calculated, is compared to a “hurdle rate”, expressed as a rate of return on the value of our net assets at the end of the most recently completed calendar quarter, of 2% per quarter (8% annualized). We pay Barings the Income-Based Fee with respect to our Pre-Incentive Fee Net Investment Income in each calendar quarter as follows:

|

|

(1)

|

(a) With respect to the Pre-2020 Period, no Income-Based Fee for any calendar quarter in which our Pre-Incentive Fee Net Investment Income (as defined in paragraph (i) above) does not exceed the hurdle rate;

|

19

(b) With respect to the Post-2019 Period, no Income-Based Fee for any calendar quarter in which our Pre-Incentive Fee Net Investment Income (as defined in paragraph (ii) above) does not exceed the hurdle rate;

|

(2)

|

(a) With respect to the Pre-2020 Period, 100% of our Pre-Incentive Fee Net Investment Income (as defined in paragraph (i) above) for any calendar quarter with respect to that portion of the Pre-Incentive Fee Net Investment Income for such quarter, if any, that exceeds the hurdle rate but is less than 2.5% (10% annualized) (the “Pre-2020 Catch-Up Amount”). The Pre-2020 Catch-Up Amount is intended to provide Barings with an incentive fee of 20% on all of our Pre-Incentive Fee Net Investment Income (as defined in paragraph (i) above) when our Pre-Incentive Fee Net Investment Income (as defined in paragraph (i) above) reaches 2% per quarter (8% annualized);

|

(b) With respect to the Post-2019 Period, 100% of our Pre-Incentive Fee Net Investment Income (as defined in paragraph (ii) above) with respect to that portion of the Pre-Incentive Fee Net Investment Income (as defined in paragraph (ii) above), if any, that exceeds the hurdle rate but is less than 2.5% (10% annualized) (the “Post-2019 Catch-Up Amount”). The Post-2019 Catch-Up Amount is intended to provide Barings with an incentive fee of 20% on all of our Pre-Incentive Fee Net Investment Income (as defined in paragraph (ii) above) when our Pre-Incentive Fee Net Investment Income (as defined in paragraph (ii) above) reaches 2% per quarter (8% annualized);

|

(3)

|

(a) With respect to the Pre-2020 Period, 20% of the amount of our Pre-Incentive Fee Net Investment Income (as defined in paragraph (i) above) for any calendar quarter with respect to that portion of the Pre-Incentive Fee Net Investment Income (as defined in paragraph (i) above) for such quarter, if any, that exceeds the Pre-2020 Catch-Up Amount; and

|

(b) With respect to the Post-2019 Period, 20% of the amount of our Pre-Incentive Fee Net Investment Income (as defined in paragraph (ii) above) for any calendar quarter with respect to that portion of the Pre-Incentive Fee Net Investment Income (as defined in paragraph (ii) above), if any, that exceeds the Post-2019 Catch-Up Amount.

However, with respect to the Post-2019 Period, the Income-Based Fee paid to Barings will not be in excess of the Incentive Fee Cap. With respect to the Post-2019 Period, the “Incentive Fee Cap” for any quarter is an amount equal to (a) 20% of the Cumulative Net Return (as defined below) during the relevant Trailing Twelve Quarters minus (b) the aggregate Income-Based Fee that was paid in respect of the first eleven calendar quarters (or the portion thereof) included in the relevant Trailing Twelve Quarters.

Cumulative Net Return means (x) the aggregate net investment income in respect of the relevant Trailing Twelve Quarters minus (y) any Net Capital Loss (as defined below), if any, in respect of the relevant Trailing Twelve Quarters. If, in any quarter, the Incentive Fee Cap is zero or a negative value, we pay no Income-Based Fee to Barings for such quarter. If, in any quarter, the Incentive Fee Cap for such quarter is a positive value but is less than the Income-Based Fee that is payable to Barings for such quarter (before giving effect to the Incentive Fee Cap) calculated as described above, we pay an Income-Based Fee to Barings equal to the Incentive Fee Cap for such quarter. If, in any quarter, the Incentive Fee Cap for such quarter is equal to or greater than the Income-Based Fee that is payable to Barings for such quarter (before giving effect to the Incentive Fee Cap) calculated as described above, we pay an Income-Based Fee to Barings equal to the Income-Based Fee calculated as described above for such quarter without regard to the Incentive Fee Cap.

Net Capital Loss in respect of a particular period means the difference, if positive, between (i) aggregate capital losses, whether realized or unrealized, in such period and (ii) aggregate capital gains, whether realized or unrealized, in such period.

The Capital Gains Fee will be determined and payable in arrears as of the end of each calendar year (or upon termination of the Advisory Agreement), commencing with the calendar year ending on December 31, 2018, and is calculated at the end of each applicable year by subtracting (1) the sum of our cumulative aggregate realized capital losses and aggregate unrealized capital depreciation from (2) our cumulative aggregate realized capital gains, in each case calculated from August 2, 2018. If such amount is positive at the end of such year, then the Capital Gains Fee payable for such year is equal to 20% of such amount, less the cumulative aggregate amount of Capital Gains Fees paid in all prior years. If such amount is negative, then there is no Capital Gains Fee payable for such year. If the Advisory Agreement is terminated as of a date that is not a calendar year end, the termination date will be treated as though it were a calendar year end for purposes of calculating and paying a Capital Gains Fee.

20

Payment of Company Expenses

Under the Advisory Agreement, all investment professionals of Barings and its staff, when and to the extent engaged in providing services required to be provided by Barings under the Advisory Agreement, and the compensation and routine overhead expenses of such personnel allocable to such services, are provided and paid for by Barings and not by us, except that all costs and expenses of its operations and transactions, including, without limitation, those items listed in the Advisory Agreement, will be borne by us.

Duration and Termination of Advisory Agreement

The Advisory Agreement has an initial term of two years. Thereafter, it will continue to renew automatically for successive annual periods so long as such continuance is specifically approved at least annually by: (i) the vote of the Board, or by the vote of stockholders holding a majority of our outstanding voting securities; and (ii) the vote of a majority of our independent directors, in either case, in accordance with the requirements of the 1940 Act. The Advisory Agreement may be terminated at any time, without the payment of any penalty, upon 60 days’ written notice, by: (a) by vote of a majority of the Board or by vote of a majority of our outstanding voting securities (as defined in the 1940 Act); or (b) Barings. Furthermore, the Advisory Agreement will automatically terminate in the event of its “assignment” (as such term is defined for purposes of Section 15(a)(4) of the 1940 Act).

Administration Agreement

Under the terms of the Administration Agreement, Barings performs (or oversees, or arranges for, the performance of) the administrative services necessary for our operation, including, but not limited to, office facilities, equipment, clerical, bookkeeping and record-keeping services at such office facilities and such other services as Barings, subject to review by the Board, from time to time, determines to be necessary or useful to perform its obligations under the Administration Agreement. Barings also, on our behalf and subject to the Board’s approval, arranges for the services of, and oversees, custodians, depositories, transfer agents, dividend disbursing agents, other stockholder servicing agents, accountants, attorneys, underwriters, brokers and dealers, corporate fiduciaries, insurers, banks and such other persons in any such other capacity deemed to be necessary or desirable.

We are required to reimburse Barings for the costs and expenses incurred and billed to us by Barings in performing its obligations and providing personnel and facilities under the Administration Agreement, or such lesser amount as may be agreed to in writing by us and Barings from time to time. If we and Barings agree to a reimbursement amount for any period which is less than the full amount otherwise permitted under the Administration Agreement, then Barings will not be entitled to recoup any difference thereof in any subsequent period or otherwise. The costs and expenses incurred by Barings on our behalf under the Administration Agreement include, but are not limited to:

|

•

|

the allocable portion of Barings’ rent for our Chief Financial Officer and Chief Compliance Officer and their respective staffs, which is based upon the allocable portion of the usage thereof by such personnel in connection with their performance of administrative services under the Administration Agreement;

|

|

•

|

the allocable portion of the salaries, bonuses, benefits and expenses of our Chief Financial Officer and Chief Compliance Officer and their respective staffs, which is based upon the allocable portion of the time spent by such personnel in connection with performing administrative services for us under the Administration Agreement;

|

|

•

|

the actual cost of goods and services used for us and obtained by Barings from entities not affiliated with us, which is reasonably allocated to us on the basis of assets, revenues, time records or other methods conforming with generally accepted accounting principles;

|

|

•

|

all fees, costs and expenses associated with the engagement of a sub-administrator, if any; and

|

|

•

|

costs associated with (a) the monitoring and preparation of regulatory reporting, including registration statements and amendments thereto, prospectus supplements, and tax reporting, (b) the coordination and oversight of service provider activities and the direct cost of such contractual matters related thereto and (c) the preparation of all financial statements and the coordination and oversight of audits, regulatory inquiries, certifications and sub-certifications.

|

The Administration Agreement has an initial term of two years, and thereafter will continue automatically for successive annual periods so long as such continuance is specifically approved at least annually by the Board,

21

including a majority of the independent directors. The Administration Agreement may be terminated at any time, without the payment of any penalty, by vote of our directors, or by Barings, upon 60 days’ written notice to the other party. The Administration Agreement may not be assigned by a party without the consent of the other party.

Election to be Regulated as a Business Development Company and Regulated Investment Company

Both we and Triangle SBIC individually are closed-end, non-diversified management investment companies that have elected to be treated as BDCs under the 1940 Act. In addition, we have elected to be treated as a RIC under Subchapter M of the Code. Our election to be regulated as a BDC and our election to be treated as a RIC for U.S. federal income tax purposes have a significant impact on our operations. Some of the most important effects on our operations of our election to be regulated as a BDC and our election to be treated as a RIC are outlined below.

|

•

|

We report our investments at market value or fair value with changes in value reported through our consolidated statements of operations.

|

In accordance with the requirements of Article 6 of Regulation S-X, we report all of our investments, including debt investments, at market value or, for investments that do not have a readily available market value, at their “fair value” as determined in good faith by the Board. Changes in these values are reported through our statements of operations under the caption of “net unrealized appreciation (depreciation) of investments.” See “Valuation Process and Determination of Net Asset Value” above.

|

•

|

We intend to distribute substantially all of our income to our stockholders. We generally will be required to pay income taxes only on the portion of our taxable income we do not distribute, actually or constructively, to stockholders.

|

As a RIC, so long as we meet certain minimum distribution, source-of-income and asset diversification requirements, we generally are required to pay U.S. federal income taxes only on the portion of our taxable income and gains we do not distribute (actually or constructively) and certain built-in gains. We intend to distribute to our stockholders substantially all of our income. We may, however, make deemed distributions to our stockholders of any retained net long-term capital gains. If this happens, our stockholders will be treated as if they received an actual distribution of the net capital gains and reinvested the net after-tax proceeds in us. Our stockholders also may be eligible to claim a tax credit (or, in certain circumstances, a tax refund) equal to their allocable share of the corporate-level U.S. federal income tax we pay on the deemed distribution. See “Material U.S. Federal Income Tax Considerations.” We met the minimum distribution requirements for 2016, 2017 and 2018 and continually monitor our distribution requirements with the goal of ensuring compliance with the Code.

In addition, we have one wholly-owned taxable subsidiary, or the Taxable Subsidiary, which holds a portion of one or more of our portfolio investments that are listed on the Consolidated Schedule of Investments. The Taxable Subsidiary is consolidated for financial reporting purposes in accordance with U.S. GAAP, so that our consolidated financial statements reflect our investments in the portfolio companies owned by the Taxable Subsidiary. The purpose of the Taxable Subsidiary is to permit us to hold certain interests in portfolio companies that are organized as partnerships or limited liability companies, or LLCs (or other forms of pass-through entities) and still satisfy the RIC tax requirement that at least 90.0% of our gross income for U.S. federal income tax purposes must consist of qualifying investment income. Absent the Taxable Subsidiary, a proportionate amount of any gross income of a partnership or LLC (or other pass-through entity) portfolio investment would flow through directly to us. To the extent that such income did not consist of investment income, it could jeopardize our ability to qualify as a RIC and therefore cause us to incur significant amounts of corporate-level U.S. federal income taxes. Where interests in partnerships or LLCs (or other pass-through entities) are owned by the Taxable Subsidiary, however, the income from such interests is taxed to the Taxable Subsidiary and does not flow through to us, thereby helping us preserve our RIC status and resultant tax advantages. The Taxable Subsidiary is not consolidated for U.S. federal income tax purposes and may generate income tax expense as a result of its ownership of the portfolio companies. This income tax expense, if any, is reflected in our Statement of Operations.

|

•

|

Our ability to use leverage as a means of financing our portfolio of investments is limited.

|

As a BDC, and as a result of the stockholder vote to approve the proposal to authorize us to be subject to the reduced asset coverage ratio of at least 150% under the 1940 Act, we are required to meet a coverage ratio of total assets to total senior securities of at least 150%. For this purpose, senior securities include all borrowings and any preferred stock we may issue in the future. Additionally, our ability to continue to utilize leverage as a means of financing our portfolio of investments may be limited by this asset coverage test.

22

|

•

|

We are required to comply with the provisions of the 1940 Act applicable to business development companies.

|

As a BDC, we are required to have a majority of directors who are not “interested” persons under the 1940 Act. In addition, we are required to comply with other applicable provisions of the 1940 Act, including those requiring the adoption of a code of ethics, fidelity bonding and investment custody arrangements. See “Regulation of Business Development Companies” below.

Exemptive Relief

As a BDC, we are required to comply with certain regulatory requirements. For example, we generally are not permitted to make loans to companies controlled by Barings or other funds managed by Barings. We are also not permitted to make any co-investments with Barings or its affiliates (including any fund managed by Barings or an investment adviser controlling, controlled by or under common control with Barings) without exemptive relief from the SEC, subject to certain exceptions. The Exemptive Relief that the SEC has granted to Barings permits certain present and future funds, including us, advised by Barings (or an investment adviser controlling, controlled by or under common control with Barings) to co-invest in suitable negotiated investments. Co-investments made under the Exemptive Relief are subject to compliance with the conditions and other requirements contained in the Exemptive Relief, which could limit our ability to participate in a co-investment transaction.

Regulation of Business Development Companies

The following is a general summary of the material regulatory provisions affecting BDCs. It does not purport to be a complete description of all of the laws and regulations affecting BDCs.

Both we and Triangle SBIC individually have elected to be regulated as BDCs under the 1940 Act. The 1940 Act contains prohibitions and restrictions relating to transactions between BDCs and their affiliates, principal underwriters and affiliates of those affiliates or underwriters. The 1940 Act requires that a majority of the directors be persons other than “interested persons,” as that term is defined in the 1940 Act. In addition, the 1940 Act provides that we may not change the nature of our business so as to cease to be, or to withdraw our election as, a BDC unless approved by a majority of our outstanding voting securities.

In addition, the 1940 Act defines “a majority of the outstanding voting securities” as the lesser of (i) 67.0% or more of the voting securities present at a meeting if the holders of more than 50.0% of our outstanding voting securities are present or represented by proxy, or (ii) 50.0% of our voting securities.

Qualifying Assets

Under the 1940 Act, a BDC may not acquire any asset other than assets of the type listed in Section 55(a) of the 1940 Act, which are referred to as qualifying assets, unless, at the time the acquisition is made, qualifying assets represent at least 70.0% of the company’s total assets. The principal categories of qualifying assets relevant to our business are any of the following:

(1) Securities purchased in transactions not involving any public offering from the issuer of such securities, which issuer (subject to certain limited exceptions) is an eligible portfolio company, or from any person who is, or has been during the preceding 13 months, an affiliated person of an eligible portfolio company, or from any other person, subject to such rules as may be prescribed by the SEC. An eligible portfolio company is defined in the 1940 Act and rules adopted pursuant thereto as any issuer which:

(a) is organized under the laws of, and has its principal place of business in, the United States;

(b) is not an investment company (other than an SBIC wholly-owned by the BDC) or a company that would be an investment company but for exclusions under the 1940 Act for certain financial companies such as banks, brokers, commercial finance companies, mortgage companies and insurance companies; and

(c) satisfies any of the following:

(i) does not have any class of securities with respect to which a broker or dealer may extend margin credit;

(ii) is controlled by a BDC or a group of companies including a BDC and the BDC has an affiliated person who is a director of the eligible portfolio company;

23

(iii) is a small and solvent company having total assets of not more than $4.0 million and capital and surplus of not less than $2.0 million;

(iv) does not have any class of securities listed on a national securities exchange; or

(v) has a class of securities listed on a national securities exchange, but has an aggregate market value of outstanding voting and non-voting common equity of less than $250.0 million.

(2) Securities in companies that were eligible portfolio companies when we made our initial investment if certain other requirements are satisfied.

(3) Securities of any eligible portfolio company that we control.

(4) Securities purchased in a private transaction from a U.S. issuer that is not an investment company or from an affiliated person of the issuer, or in transactions incident thereto, if the issuer is in bankruptcy and subject to reorganization or if the issuer, immediately prior to the purchase of its securities, was unable to meet its obligations as they came due without material assistance (other than conventional lending or financing arrangements).

(5) Securities of an eligible portfolio company purchased from any person in a private transaction if there is no ready market for such securities and we already own 60.0% of the outstanding equity of the eligible portfolio company.

(6) Securities received in exchange for or distributed on or with respect to securities described in (1) through (5) above, or pursuant to the exercise of warrants or rights relating to such securities.

(7) Cash, cash equivalents, U.S. government securities or high-quality debt securities maturing in one year or less from the time of investment.

In addition, a BDC must have been organized and have its principal place of business in the United States and must be operated for the purpose of making investments in the types of securities described in (1), (2), (3) or (4) above.

Managerial Assistance to Portfolio Companies