BDC Common Stocks Market Recap: Week Ended February 13, 2026

BDC COMMON STOCKS

Week 7

Bewildered

Wall Street finished the trading week on a weaker note as investors digested a fresh batch of economic data, including the latest nonfarm payrolls report and Consumer Price Index release. Market participants also continued to monitor the flow of corporate earnings results.

For the week, the S&P (SP500) lost -1.4%, while the tech-heavy Nasdaq Composite (COMP:IND) dipped -2.1%, and the blue-chip Dow (DJI) fell -1.2%.

seeking alpha- wall street breakfast - february 14, 2026

Back And Forth

The BDC exchange-traded fund with the ticker BIZD - one of our favorite ways to measure the sector’s price performance - moved exactly nowhere this week.

BIZD closed on Friday, February 6, 2026, at $13.42 and ended right back there a week later.

However, in the intervening time, there was much movement - up for two days, with BIZD climbing up to 3.7%, only to slump back Wednesday-Friday.

Investors were reacting to the economic data mentioned above and to the continuing angst about the impact AI will have on…everything.

This week, the baton of panic was passed on to wealth management, logistics, and insurance brokerage companies, amongst others.

Here is a useful precis of the latest angst.

Stable-ish

Yet- as we’ve seen - the BDC sector was relatively calm, measured end to end.

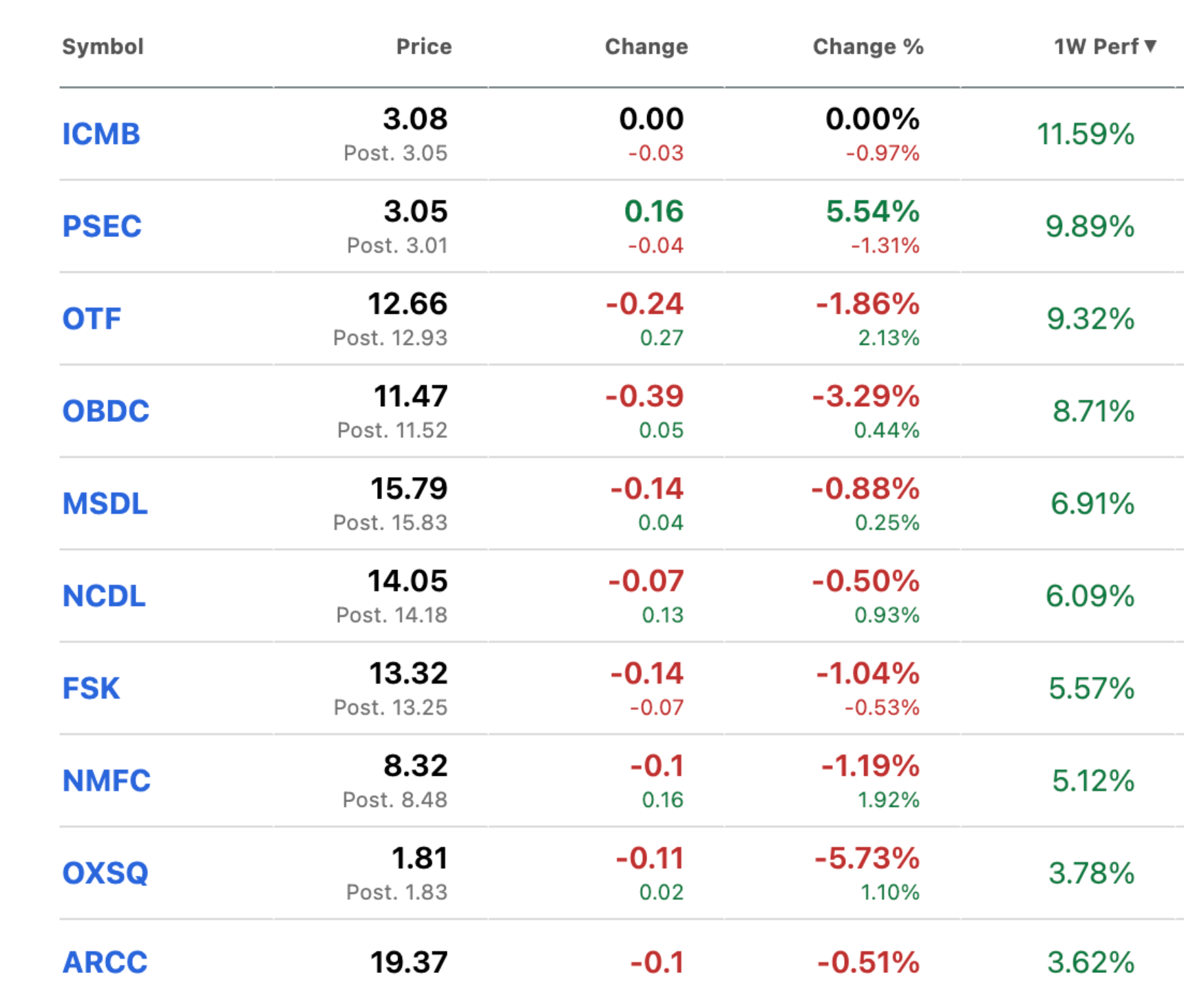

For the first time in 4 weeks, more BDCs increased in price - 30 - than decreased - 16.

We get the impression there was some would-be value buying going on as 10 BDCs increased 3.0% or more in price.

The Last Shall Be First

Setting aside Ares Capital (ARCC), pretty much all the leading price movers this week were BDCs previously beaten up by an unforgiving market that sells first and retraces some of its steps later.

Intriguingly, most of the BDCs on this week’s Winners List have not yet reported their results. The upward price move seems like a positioning strategy, reflecting some optimism - a quality in short supply in the last few weeks.

Spotlight

Prospect Capital (PSEC) did report its latest results, and an increase in its quarterly earnings per share seems to have all that was necessary to ignite investors' animal spirits and push the price up nearly 10%.

The BDC Reporter wrote an article this week about the idiosyncratic BDC’s credit performance in the IVQ 2025 - and in the longer term - which concluded as follows:

To each their own. Clearly, some investors are delighted by the unexpected increase in PSEC’s recurring earnings. (We will point out, though, that the boost has everything to do with a surge in dividend payments from “Controlled Companies” even as interest income continued to decline). Others, though, could be concerned that PSEC’s eroding NAVPS – down (43%) since the IIQ 2022 – could continue, eventually impacting both book value and earnings power.

By the way, the recently inaugurated BDC Performance Table rated PSEC’s IVQ 2025 performance overall a 4 on our 5-point scale, weighed down by the (3.7%) decrease in PSEC’s net asset value per share (NAVPS) in the quarter - the biggest percentage drop amongst the 14 BDCs that have reported IVQ 2025 book value numbers.

If not for the write-up of one of PSEC’s largest “control investments - where the BDC is both lender and owner and not subject to much independent scrutiny as to valuation - the NAVPS loss would have been even higher.

In our rating system, a 2-cent increase in recurring earnings does not make up for the 24 cents per share lost in book value, but we were clearly in the minority, judging by PSEC’s price jag.

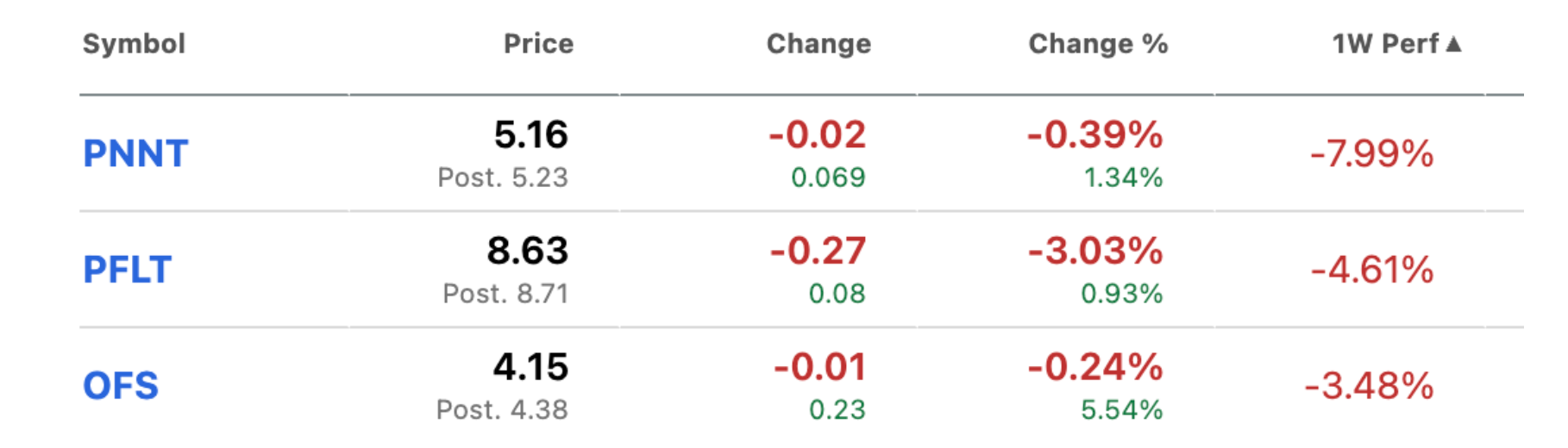

“Losers”

Here are the BDCs that performed poorly this week, price-wise:

The two PennantPark BDCs reported results modestly below reasonable expectations, receiving a rating of 3.

Check out the table where we summarize in a paragraph the key metrics achieved.

As to OFS, which has not yet reported: the troubled BDC was - once again - at a new price low this week and has lost two-thirds of its value in recent years.

OFS has fallen nearly (50%) in price in just the last 12 months, the most by any public BDC.

WHERE WE ARE

Painting The Picture

We are 7 weeks into 2026, and we’ve had 3 weeks of BIZD headed up, 3 weeks headed down, and 1 flat week.

At this point, BIZD is off (5.4%) in price terms.

The S&P BDC Index - which uses a different methodology - is (6.1%) down just on price and (5.9%) on a total return basis.

Clearly, it’s too early in the year for the still robust dividends BDCs pay out to affect their return profiles.

Anyway, by any measure, this is NOT a good start to a year that held some promise at the beginning.for the record

Only 11 of 46 BDCs have managed to increase in price this year, and given the headwinds of the last few weeks, that seems something of an achievement.

Only 5 BDCs are trading at or above their NAVPS.

Knocked Off Their Perch

Gone from their traditional presence on this list are luminaries like ARCC, Gladstone Investment (GAIN), and Gladstone Capital (GLAD).

That second Gladstone BDC even managed to reach a new 52-week low this week.

At this point, only 2 BDCs are trading within 10% of their 52 week highs.

On the other hand, 35 BDCs are within 10% of their 52 week lows.

That metric is the worst it’s been all year.

Maybe the most telling stat is that nearly one year after BIZD reached a multi-year high in February 2025, the ETF is down (25%) in price.

By that standard, we are deep into “Bear Territory”.

WHERE WE ARE HEADED

All Bets Off

We could take on the uncertainty about the economy and whether inflation will be X or Y, and whether interest rates will be cut once, twice, or thrice in 2026.

However, now those of us with crystal balls have to contend with this unanswerable concern about what we’ll call for simplicity’s sake “AI risk.”

We’ve begun conducting extensive research into the subject, reviewing every BDC’s portfolio.

Ironically enough, our analysis will be greatly facilitated by the data-crunching ability of AI models themselves.

However, we can already tell that our initial conclusion is likely to be inconclusive and will consist of some variation of “We shall have to wait and see”.

In a year or two, the research is likely to be more useful, but we’re beginning our journey of a thousand miles now.

Familiar Bugbear

Not as new but just as difficult to contend with is whether the Fed gives the Administration what it wants or sticks - at least nominally - to its inflation-fighting guns.

This is a subject that we came back to again and again on these pages in 2025.

Unfortunately, the gap between those in power in Washington, D.C., a still-small group of their acolytes in the financial community, and the majority of Fed members has only grown wider over time.

The BDC earnings landscape at the end of 2026 - and its outlook - will look very different if the Fed Funds rate has been wrestled down to 2.0%-2.5% versus the 3.4% the current dot plot suggests.

We have rarely encountered - outside of a major economic contraction - such a high degree of uncertainty.

Moreover, most of the portents for BDC prices in the months ahead are unfavorable, which is not what we would have said in January.

Maybe the most favorable factor is that BDC prices have already fallen as much as they have.

No downtrend lasts forever.

This one is already 12 months long, but it does not feel like the bottom yet.

We have not had the panic selling and the inevitable headlines from the financial press asking existential questions about the future of leveraged lending that we saw in 2008-2009 and in 2020.

There’s that to look forward to.

Reassuring Last Word

Nonetheless, even with “AI Risk” layered on, we continue - based on our research and long experience in this market - to believe that “this too shall pass” and the phenomenal expansion of Private Credit and of BDCs, both public and private, will continue.