BDC Common Stocks Market Recap: Week Ended February 20, 2026

BDC COMMON STOCKS

Week 8

Running For The Exits

Wall Street ended the week higher as investors navigated a flurry of economic data points, corporate earnings, and a major legal development in Washington. After bouts of volatility earlier in the week, equities stabilized into Friday’s close, with market participants reassessing growth expectations and policy risk.

For the week, the S&P (SP500) gained +1.1%, while the tech-heavy Nasdaq Composite (COMP:IND) moved up +1.5%, and the blue-chip Dow (DJI) advanced +0.3%.

seeking alpha - wall street breakfast - february 21, 2026

Disjointed

For a few weeks, both the major markets and the BDC sector seemed to be worried about the same risk: the potential disruption that artificial intelligence (AI) might wreak on companies across the economic landscape.

This week, though, the major markets switched focus to the dramatic change in the tariff regime brought on by the Supreme Court.

There was also a slew of economic data, which some read as favorable and some not, but, as shown above, all the key indices were in the black.

Left Behind

However, BDC investors continued to wallow in deep-seated - and sometimes extreme concerns - that AI will shortly destroy a goodly portion of BDC portfolios.

This anxiety sits alongside pretty decent IVQ 2025 results from a third of the public BDC universe in Week 3 of earnings season and no discernible credit impact on anybody’s performance.

Clearly, investors are putting much more emphasis on the jeremiads in the financial press - Bloomberg at the front - rather than the reassuring speeches made by BDC managers on their conference calls.

Down

BIZD - the only exchange-traded fund for the BDC sector and our favorite - if flawed - measuring stick, fell (1.9%).

For reasons we cannot explain, the S&P BDC Index - on a price basis - dropped even more: (2.8%).

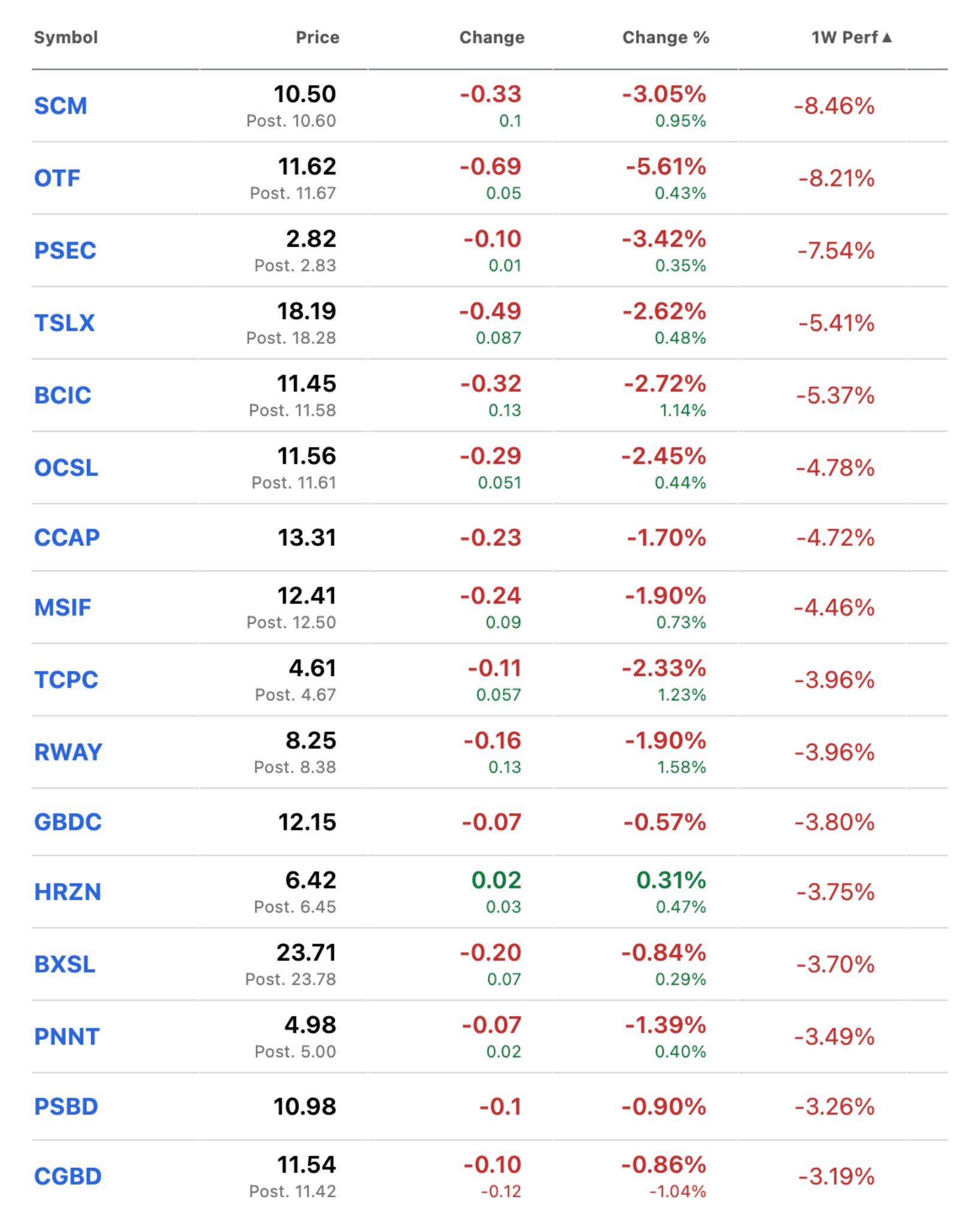

When we look at individual BDC performance, the picture is just as ugly.

41 of the 46 BDCs we track moved down in price, including 16 by (3.0%) or more.

Here’s the full list, if only to illustrate that BDCs of every ilk are present, including many whose financial performance either in the IVQ 2025 or previously has been first rate:

A third of all BDCs reached new 52-week lows during the week.

A little surprisingly, though, the number of BDCs trading at or above book held firm at 5.

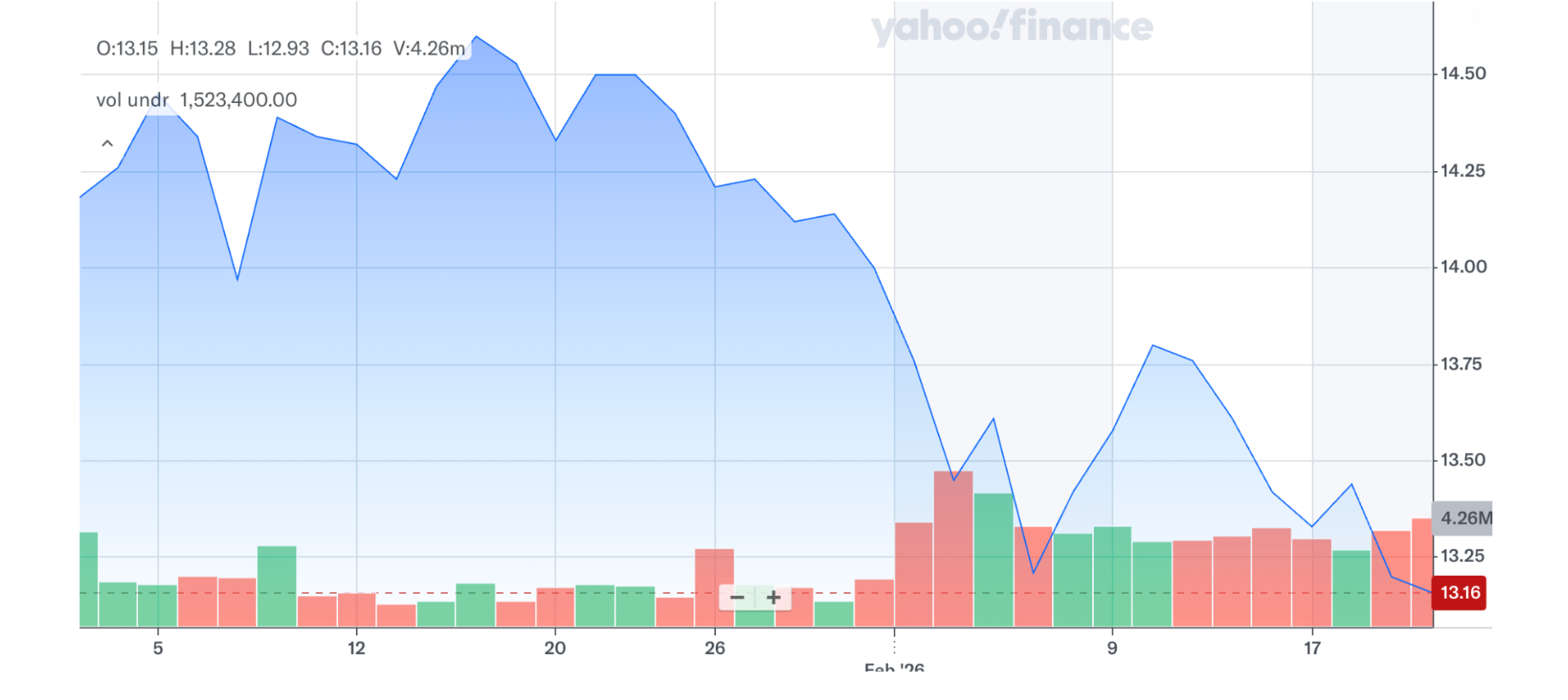

What is most notable - and vividly obvious from this YTD chart of BIZD below - is how trading volumes have amped up in recent weeks, including the 4 trading days that have just concluded.

That’s the rush to the exit doors.

WHERE WE ARE

Very Bad

With only 8 weeks in the rear view mirror, the BDC sector couldn’t have had much of a worse beginning to the year.

BIZD closed on Friday at $13.16, down (7.2%) in 2026.

The S&P BDC Index - which uses a different methodology and includes dividends received in these first two months - is even deeper in the red: (8.4%).

Only 5 BDCs have managed to remain in the black in the past month on a price basis and 7 YTD.

13 BDCs are already (10%) or more down in price, including 1 which just topped (20%).

That’s Blue Owl Technology Finance (OTF), which is the poster child of investor anxiety.

If you look at the BDC Performance Table, you’ll see we gave the ill-fated BDC a Performance Rating of 2 - Performing As Expected - in the IVQ 2025.

OTF received a 1 rating in the IIIQ 2025.

Here’s how our NotebookLM summarized the most recent results:

Summary In the fourth quarter of 2025, OTF experienced continued portfolio expansion, with AUM at fair value growing to $14.29 billion, which helped push its Net Asset Value up by 0.35% to $17.33 per share. Despite the larger portfolio size, lower base rates contributed to yield compression across the portfolio, which slightly depressed total investment income and brought Adjusted Net Investment Income down to $0.30 per share from $0.32 in the prior quarter. Credit quality remained generally stable but exhibited a mild uptick in underperformance, as non-accrual investments rose to 0.2% of fair value across two borrowers, and internal watch-list ratings expanded modestly. Through these shifts, the company sustained its total shareholder payout, maintaining a consistent $0.40 per share dividend.Curated By the BDC Reporter

Clearly, at OTF - and at all the BDCs brought low price-wise of late on AI concerns - the massive credit losses which the market seems to be building into the price are all in the future.

WHERE WE ARE HEADED

Wish We Knew

It’s a cliche, but this is uncharted territory.

For the first time in BDC history, the markets are seriously questioning the financial viability of a fifth or more of investments on the books.

Moreover, this huge question mark has only arisen in the last few weeks and seems impervious to anything the BDC managers have to say.

As a result - as this next lifetime chart of BIZD shows - the sector is at a five-year price low.

If you leave out the short, weird Covid period, BIZD is at an all-time (13-year) nadir:

Will The Fever Break?

We don’t know, but our internal data shows 41 BDCs generating a yield in excess of 10.0% in 2026 - based on the current price and our constantly updated estimate of the likely payout.

Of those, 11 are yielding over 15%.

Decision To Make

Investors up and down BDC-land are going to have to take a deep breath and decide how certain they are that a credit-pocalypse (to coin an unwieldy term) is slouching towards us.

If we get the maximum impact that some are forecasting, today’s prices will seem very generous.

We notice, though, that the broader markets - presumably also in the line of fire - are not as certain that we are about to face a tsunami of failure across thousands of some of the most profitable and successful companies out there.

If we get no material impact - and even after adjusting for lower interest rates - BDC prices may seem like bargains, especially compared with a month ago before this episode began.

We just don’t know which way investors will lean.

OUR OWN VIEW

Just for the record, at this point, we don’t believe there is going to be a credit-pocalypse. We don’t even countenance there being any material pick-up in the level of current credit distress in the BDC sector. Our confidence is based partly on our confidence in the underwriting track records of most of the asset managers running BDCs, as well as their ability to duck and weave appropriately if conditions change. We also don’t “buy” into the narrative going around that AI will spell the end for a wide swathe of existing companies across many sectors. Not so long ago, there was a concern that AI itself might not usher in the Brave New World promised by its proponents, and the hundreds of billions of dollars spent could be largely for naught in terms of real productivity improvements.

Unfortunately, though, some time will need to pass before either the credit-pocalypse will descend upon us, or the all-clear signal will sound. In the intervening period, we will keep an open mind because at worst this could represent the greatest challenge to the BDC sector - and to Private Credit - since its inception, or it could blow like so many other worries that have come before.

Well Said

Regarding that last point, we’ll close by quoting at length what the new CEO of Barings BDC (BBDC) had to say about all this last week on the BDC’s conference call:

The current market tone is reminiscent of a few other periods in recent memory. During 2018, the U.S. initiated a trade war with China, with justified concerns that industrial and manufacturing businesses would experience headwinds, causing bankruptcies across the country. At the onset of the COVID pandemic in 2020, logical arguments were made that healthcare companies would be forever transformed and loans to healthcare issuers would face a reckoning. And in March of 2022, interest rates began a historical rise, ultimately leveling off at more than 500 basis points by mid-2023. The rapid rise in interest rates caused many investors to express concern about indebted companies and the confidence and sustainability of various industries.

Within the context of Barings' managed portfolios, we did not experience a wave of industrial default, healthcare defaults or general industry defaults due to any of these events. What we did witness, however, was that during these periods of rapid industry change, businesses with weak management, poor business models, and questionable value propositions did experience stress. And some companies did fail, but it was not the macroeconomic events that drove losses. It was the fact that macroeconomic events exacerbated weaknesses that already existed.

We believe we stand on the precipice of another period of rapid industry evolution and in this case, within the software ecosystem. Business models will be tested and some may ultimately fade away but well-run businesses managed by smart and capable people are expected to continue exhibiting success.Poorly run businesses will experience the same business cycle that all poorly run businesses ultimately experience. Products will become obsolete, customers will leave and the relevance will be diminished.

CEO Thomas McDonnell- BBDC IVQ 2025 Earnings Conference Call